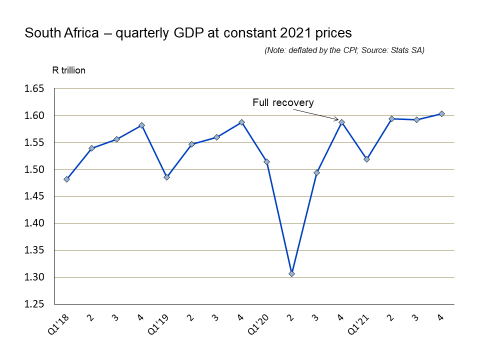

With talks to end the conflict in Ukraine underway, it is useful to revisit the latest national accounts data in more detail. Thanks to the predictable surge in mining activity (boosted by high commodity prices), and the resurgence of the trade and hospitality sectors, nominal GDP increased by 12% to a level of close to R6.2-trillion.

Deflated by the average consumer price index (CPI) for 2021, this translates into a real growth rate of 7.4%. Unfortunately, Stats SA uses a rather complicated set of formulas to remove the effect of inflation from the nominal data, which yielded a lower real growth rate of 4.9%.

There is also a huge question mark over the calculation of value added by the agriculture sector. According to data from the producer organisations representing the largest contributors to agriculture output, 2021 was a record year for most product groups, but Stats SA data shows a decline in the sector’s value added of 11% (in nominal terms).

The record export performance of the agriculture sector during 2021 serves as further confirmation of a likely grave error in Stats SA’s estimation of the sector’s contribution to GDP in 2021.

Under the conservative assumption of a 10% nominal increase in agriculture value added in 2021, South Africa’s real GDP growth rate for last year stands at an impressive 8% (deflated by the CPI).

An encouraging feature of the GDP data for 2021 is the recovery of net capital formation, which recorded a very healthy nominal growth rate of almost 14%, boosted by a predictable recovery of inventories. During 2020, when the pandemic set in, inventories declined by a record R53.6-billion.

In 2021, this component of capital formation remained in negative territory, but at a figure of minus R9-billion, it represents a turnaround of more than R44-billion.

Further recovery during 2022 is bound to occur, which should provide growth momentum for new investment in productive assets (including infrastructure). In 2021, both the private sector and public corporations managed to increase their expenditure on new economic capital in real terms.

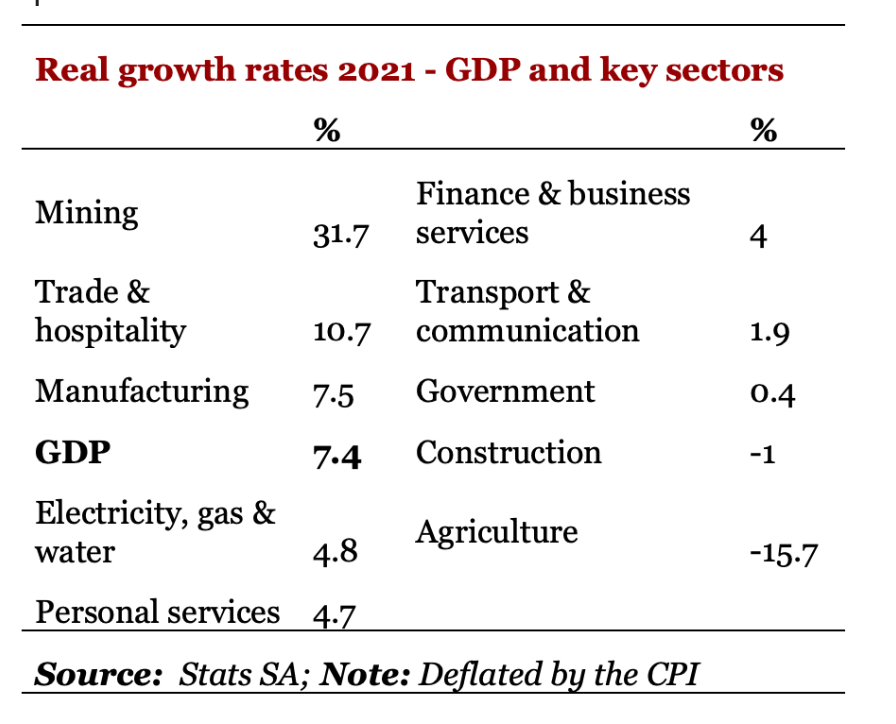

The real growth rates for the country’s GDP and key sectors in 2021 are listed in the table below (deflated by the CPI):

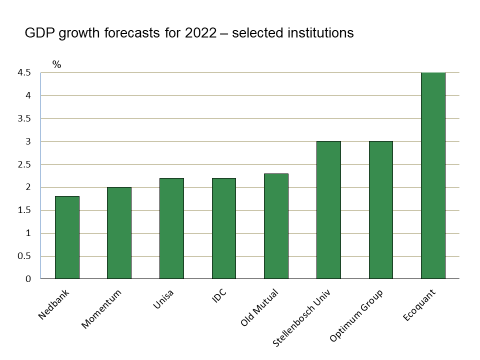

Attention now turns to prospects for another solid economic performance in 2022, with wide-ranging opinions amongst different forecasting agencies and institutions. According to the IMF, South Africa should record real GDP growth of just less than 2%. National Treasury is more upbeat, pitching at 2.1%.

When considering the strong likelihood of a full recovery of the hospitality industry, an impressive pipeline of infrastructure projects, government’s new initiatives to cooperate with the private sector in the area of deregulation and the imminent second phase of inventory recovery, these forecasts seem ultraconservative.

A number of reputable institutions do expect significantly higher growth this year, as illustrated by the graph above. Hopefully, National Treasury will eventually prove to have erred on the side of caution (just like last year!) BM/DM

[hearken id="daily-maverick/9284"]