Answer: I cannot give you a categorical answer on any of these issues, as I do not know enough about your personal situation. What I can do is flag some of the issues you should consider when discussing the options with a professional.

Selling some of the properties

When you invest, you need to be careful about exposing your investments to only one asset class. We often find that certain sectors of the market have cycles, where they move up for a while and then they go down. If all your wealth is concentrated in only one sector, you are exposing your finances to this concentration risk.

Property is also a high-involvement investment. If you do not employ the services of a property management company to manage these properties, it can become quite a hassle as you get older. Your desire and inclination to manage the ongoing repairs of these properties often reduces as you get older.

A downside of living off rental income is that you are dependent on the ability of those who are renting from you to pay the rent. During the lockdown, I helped many retired people recalibrate their finances as their rental income became erratic. (This may not be an issue, as you have a substantial preservation fund that can pay you an income.)

Setting up a trust

One of the advantages of a trust is that you peg the value of the asset in your estate to the value at the time of the transfer to the trust. This is why I often consider the use of trusts for my clients who want to build up a portfolio of investment properties.

You have a substantial portfolio that has grown over the years. Moving the properties into a trust will trigger a capital gains tax (CGT) event. Given the number of properties you have, this can be quite significant, so give some thought to the cash flow implications of this action.

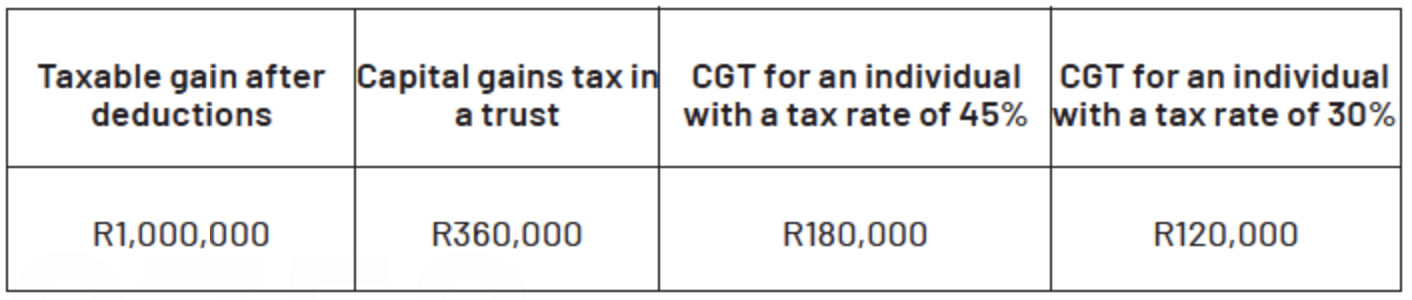

If you sell an asset out of a trust, the CGT would be a lot higher than if you sold it in your individual capacity. For example:

The question you need to ask is what appetite the next generation has to manage the property portfolio when you and your husband are no longer around. If they intend disposing of most of the properties, they will end up paying CGT at a much higher rate, which is not desirable.

If you are thinking of selling some properties, sell them before you move the properties into a trust.

You must make sure that you manage the trust properly and distribute any income if the tax rate of the recipients is less than 45%, as the tax rate in a trust is 45%.

Having said that, trusts are often an overlooked way to ensure the smooth transfer of assets when someone dies.

Preservation fund

As you have enough money to live on from your property portfolio, I would recommend that you consider delaying the spending of any of your retirement savings. My reasoning here is that your retirement savings do not form part of your estate, so there will be an immediate 20% saving in estate duty should you die.

Take a close look at the portfolios that your preservation fund is invested in. As you are unlikely to need to access it any anytime soon, you can afford to be a bit more aggressive in your choice of portfolio.

In some of my earlier columns I spoke about the importance of matching your equity exposure to the timeframe of your investment.

If your financial adviser was not aware of your substantial property portfolio, they may have put you in a portfolio that is too conservative. This could result in an opportunity cost.

There are many factors to consider and you do need to get a professional in to help you make the right decisions. DM168

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for R25 at Pick n Pay, Exclusive Books and airport bookstores. For your nearest stockist, please click here.

Comments

Scroll down to load comments...