Question: There is a lot of talk about the benefits of converting a retirement annuity into a living annuity as soon as one turns 55. Is this advisable?

Answer: As with most financial planning questions, the answers depend very much on personal circumstances, so I cannot give any categoric answers. I will, however, run through some of the pros and cons of doing this.

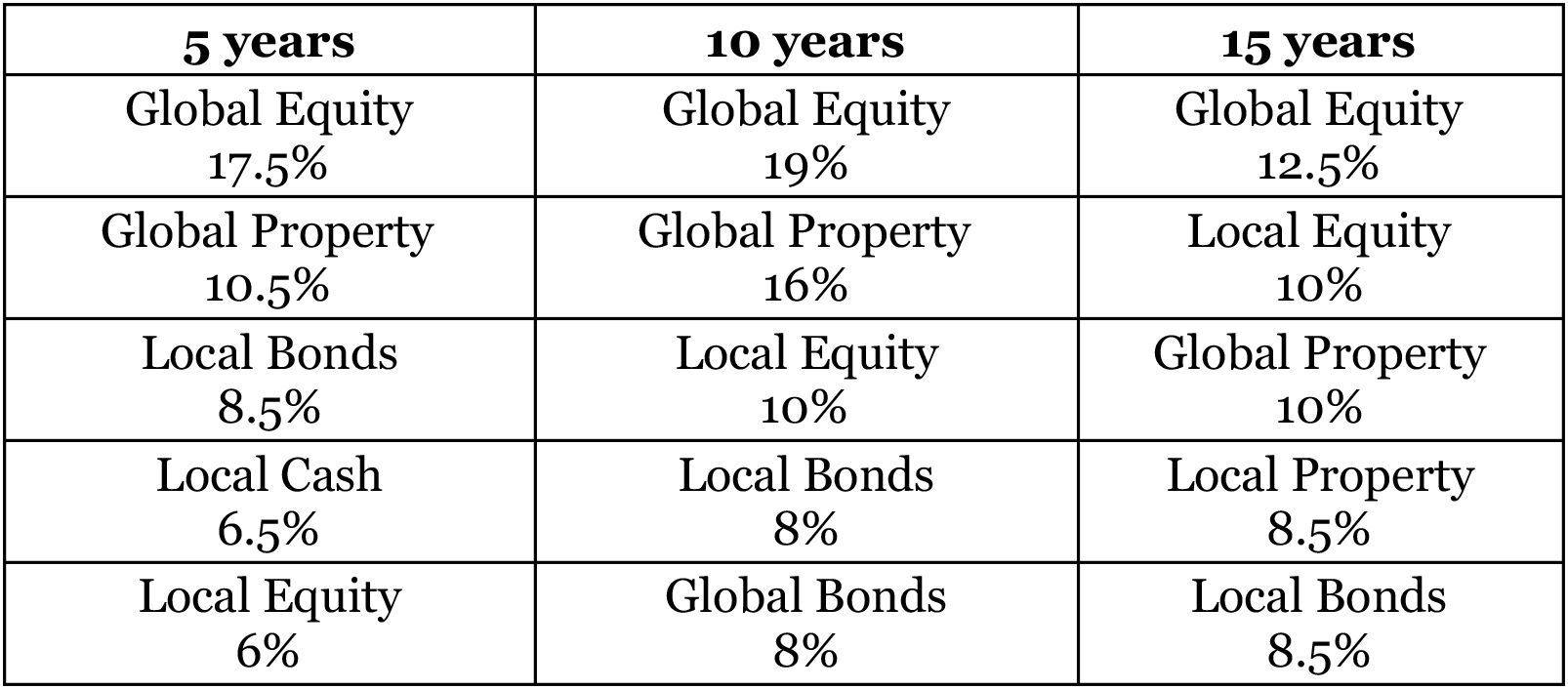

Investment portfolios

With a retirement annuity, your investments must conform with regulation 28, which places certain restrictions on where you can invest your money. For example, you are only allowed to invest 25% of your assets outside of Africa and are potentially missing out on the great performance of global equities.

If you look at the table below, which gives the rounded performance of the various asset classes over the past five, 10 and 15 years, you will see that global equity, when converted to rands, has consistently been the best performer.

Over the past five years, global equity returned 17.5% compared with the 6% from local equity. This is why many are looking at moving their investments into a space like living annuities where regulation 28 does not apply.

Be careful of just assuming that offshore always produces better results than local investments. I have some clients who obtained in excess of 30% growth on their regulation 28 compliant portfolios over the past year.

Avoid this mistake

A living annuity requires you to take a minimum of a 2.5% drawdown. What often happens is this 2.5% becomes part of your normal family budget and “disappears”. Had you left it in the retirement annuity it would have continued to grow.

A solution that I often suggest for my clients is that they take the 2.5% drawdown annually and, at the same time, take out a retirement annuity where there is an annual premium that matches the drawdown. This will ensure the money does not get used for groceries and continues to be used for retirement savings. The retirement contributions are tax-deductible so you will be left in a cost-neutral situation.

What to do with lump sums

You are allowed to take a lump sum of one-third of the value of your retirement annuity investment. The first R500,000 of this amount will be tax-free. This is an attractive benefit and you do not want to lose it.

The allowance applies to the total of all your retirement savings, so there will be times when it makes sense not to take a lump sum from a particular investment and rather have it applied to another one.

Now, should you take this lump sum when you convert to a living annuity? The answer really depends on what retirement savings you have. If you are part of a company pension fund you may not be able to retire into a living annuity when you turn 55, so it may be better to use that as the source of your lump sum.

If you withdraw the R500,000, you may invest it wherever you like. The growth will be subject to capital gains tax. However, if the money was invested in a living annuity, there would be no capital gains tax payable.

If you invest the income from your living annuity into another retirement annuity until you eventually retire, you may make a withdrawal from that retirement annuity and take advantage of the tax-free benefits.

Inheriting

When it comes to inheriting from a living annuity, the process is quick. The beneficiaries could get the lump sum value of the living annuity or receive the ongoing payment stream. I have a couple of clients who receive a living annuity as part of an inheritance. The additional monthly income makes a significant difference in their lives — it is the gift that keeps on giving.

Inheriting from a retirement annuity is not as simple. As a retirement annuity is a retirement fund, the trustees of the fund must make a decision regarding the distribution of the benefits. This is usually in line with your beneficiary nomination, but the trustees do need to approve it, so there will be delays.

There are benefits to converting a retirement annuity to a living annuity but you need to do it properly and ensure that you will be better off when you retire. DM168

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for R25 at Pick n Pay, Exclusive Books and airport bookstores. For your nearest stockist, please click here.

Comments

Scroll down to load comments...