Answer: There are three key decisions that you will need to make here:

- How much are you going to draw out of your investment to live on each year?

- What portfolios should you use?

- Do you invest all your money in South Africa?

Drawdowns

One big challenge you have is that you do not know how long you will be drawing an income for. You don’t want to run out of money, so you need to budget on drawing an income for the next 35 years (until you turn 100). I have several clients who are close to 100.

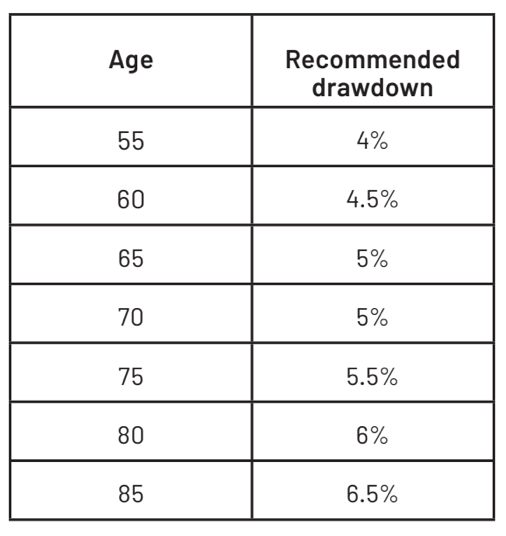

The drawdowns you make from your investment must be sufficient for you to live on but not so high that you eat into your capital. There have been guidelines published by the Financial Sector Conduct Authority that give the level of drawdown you should ideally use so that you do not run out of money. These are given below:

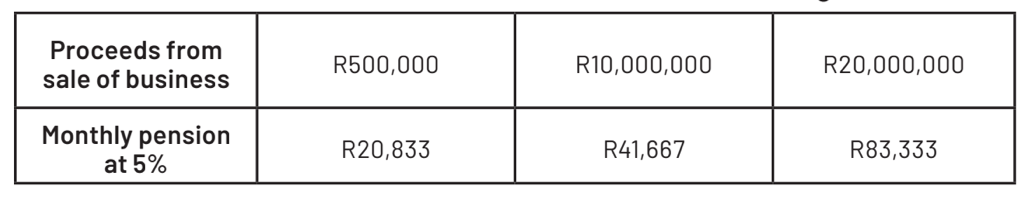

As a 65-year-old, you can draw down 5% of your investment each year. To give you an idea of how much you’ll receive each month, look at this table:

Portfolio choice

This is where a lot of people make mistakes. They put all their money into a conservative portfolio so that they do not lose money; after all, they no longer have a job and will not be earning money in the usual way. This can result in them running out of money in the years that follow. Remember, your money needs to last you for 35 years.

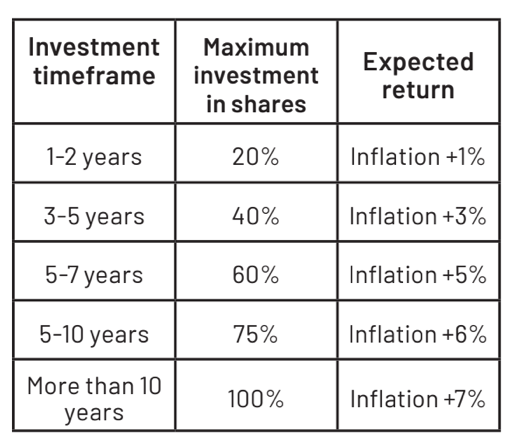

You need to make your investment work for you. As you have a 35-year investment horizon, you need to have a mix of investment types. The table below shows some of the factors I consider when putting an investment portfolio together for a client:

I like to use my three-potjie approach where I have:

- At least two years’ worth of income in a one-to-two-year portfolio;

- An amount in a portfolio with a medium-term timeframe; and

- An amount in a portfolio with a long-term timeframe.

The actual percentage that I would decide to use would be based on your specific circumstances.

These would need to be reviewed regularly and adjusted where needed.

Local or offshore

I believe in diversifying one’s investments. Having all your investments in one country is an unnecessary risk. I have seen it in action with a number of my clients where a fall in the South African markets has been compensated for by a rise in the overseas markets and vice versa.

The specialists recommend having between 40% and 60% of your assets offshore. I would therefore recommend that you consider investing some of your assets offshore. I would keep the short-term investments in South Africa, as our returns are better and the mechanics of paying the income would be simpler.

You mentioned that you wish to leave an inheritance to your children. Most of my clients have at least one child living overseas. By having some of your investments based offshore, you can make inheriting money a lot simpler for them. You can do this by putting your money into a structure where you make your children the beneficiaries of ownership should you and your spouse pass away. They would inherit within weeks rather than the years it takes to finalise an estate with children living overseas.

To summarise, you should not draw down more than 5% of your investment in any year. You need to keep at least two years’ worth of money in a conservative fund. You need to spread the rest of your money into growth assets, with at least half being offshore. For the offshore money, you should use a structure that will make any inheritance easier and cheaper. I would recommend that you chat to a financial adviser who can determine the correct mix of portfolios for you. DM168

Kenny Meiring MBA CFP is an independent financial adviser. You can contact him at Financialwellnesscoach.co.za. Please send your questions to kenny@financialwellnesscoach.co.za.

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for R25 at Pick n Pay, Exclusive Books and airport bookstores. For your nearest stockist, please click here.

Comments

Scroll down to load comments...