First published in the Daily Maverick 168 weekly newspaper.

Answer: Your question is certainly relevant. I love to give talks to groups on how to manage their finances better. This issue of teaching our children and grandchildren good financial habits comes up regularly.

There are three principles that are central to your financial wellness.

Principle 1 – You will earn a finite amount of money in your life. What you spend it on depends on the choices you make when you first start earning.

You can spend your lifetime earnings on the repayment of debt or on having great experiences. Sadly, most people end up spending too much of their lifetime earnings on debt repayments. Easy access to credit has led to this situation.

Do you really need those clothes so badly that you must open up a store credit account? Can you drive your car for a couple more years while you save up for a replacement? Should you really be taking money out of your home loan to pay for that holiday?

If you are able to delay gratification and save up for an item rather than buy it on credit, it will make a huge difference to your overall financial wellness.

Principle 2 – Invest a portion of your earnings immediately.

When I was growing up, one of the building societies (remember them?) had an advert for a special savings account that offered a higher interest rate. The advert resonated with me – it said: “Spend 90% of your money with a clear conscience”.

I took this to heart and saved 10% of all I earned. When I started work, I was able to buy an Opel Kadett for cash while many of my friends had car loans.

This is a great principle to teach children. Save 10% of your birthday money, save 10% of your pocket money and, when you get a job, immediately save 10% of your salary.

It is important that you put the 10% into the investment immediately. Do not wait till the end of the month to see if there is anything left over that you can save. Trust me, that money will disappear.

Principle 3 – Poor people work for money; rich people get money to work for them.

A key element to becoming wealthy is to harness the power of compound interest. With compound interest, you get interest on your interest. The longer you invest, the more your money grows.

It therefore makes sense to start investing as soon as possible.

The earlier you start, the more the compound interest will add to your wealth.

This is best illustrated by way of an example. Consider a set of triplets – Larry, Moe and Curly (and their sister, Susan, who we’ll get to later):

Larry invests R10,000 a year for 40 years. Total investment is R400,000.

Moe invests R15,000 a year for 30 years. Total investment is R450,000.

Curly invests R20,000 a year for 25 years. Total investment is R500,000.

Now, if each investment gave a return of 5% a year, see the first table below for the amounts each triplet would have.

As you can see, even though Larry invested less money than his brothers, his savings are significantly higher. More than two-thirds of his final investment value consists of investment returns. This shows the value of investing for a long period.

His brother Curly, who invested more money for half the period, received much less in terms of investment returns – R502,000 compared with R868,000.

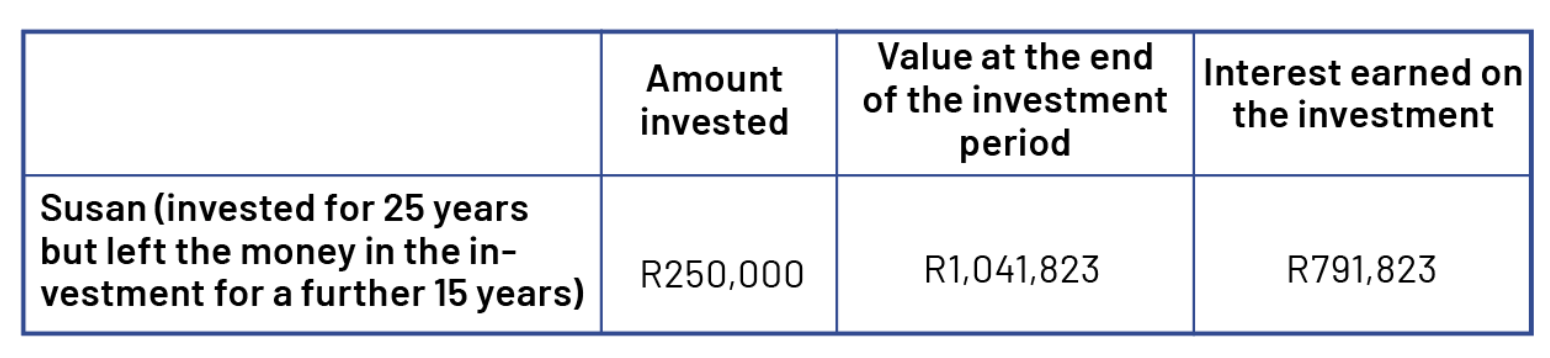

Now consider Susan, who invested for 25 years but, unlike her brother Curly, started investing at the same time as Larry but stopped making deposits after 25 years and left the money in the investment for a further 15 years. See the second table below for the outcome.

As you can see, even though she invested half of what Curly did, her investment was worth more than her brother’s. This highlights the value of compound interest (and why you should never cash in your pension benefit when changing jobs). DM168

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for R25 at Pick n Pay, Exclusive Books and airport bookstores. For your nearest stockist, please click here.

Comments

Scroll down to load comments...