First published in the Daily Maverick 168 weekly newspaper.

Answer: There are a few options open to you:

Increase your drawdown rate

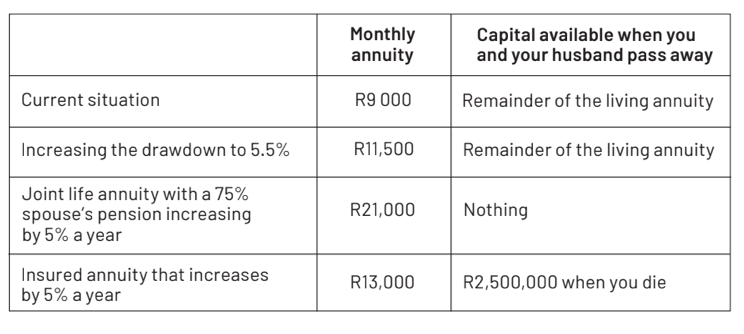

As a 75-year-old, you can increase your living annuity drawdown rate to 5.5%. This means that you could draw a pension of R11,500. As long as you are careful in your fund selection and regularly review the fund performance and drawdown rate, you should not run out of money. The additional R2,500 a month could provide the necessary buffer to ensure that you do not have to use your emergency fund for living.

Convert to a life annuity

You are allowed to convert a living annuity into a life annuity, but can’t convert a life annuity into a living annuity.

The income that you get from a life annuity increases as you get older so I often recommend that my newly retired clients take out a living annuity and then convert it to a life annuity when they get older.

Married pensioners should consider taking out a joint life annuity that decreases by 25% on the first death. Many living costs are fixed, so if one partner dies, the overall cost of living does not halve. A 25% reduction would be more appropriate.

In your instance, if you took out a joint life annuity with a 25% reduction on the first death, your R2.5-million would get you around R21,000 a month, increasing by 5% a year for the rest of your lives.

When the first person dies, the annuity would decrease by 25%.

That is more than you need so I would recommend that you use the additional money to bolster your emergency fund.

Although your annuity increase of 5% is on the upper end of the government’s targeted inflation rate of 3% to 6%, the inflation rate for pensioners is often higher than the official rate.

The biggest items in a pensioner’s budget are medical costs and electricity and these items have been increasing by way more than the official inflation rate.

I recommend that pensioners have additional savings or retirement annuities that they can access in years to come when the higher cost of living starts to take its toll.

Insured annuity

As you are under 80, an additional option that is open to you is an insured annuity.

The monthly income here is usually higher than that of a living annuity, but not quite as high as you would get with a regular life annuity. Should you need to leave a capital sum, however, then this is an option to consider.

Many retired people make the mistake of placing too much focus on leaving an inheritance with their pension savings and not enough on ensuring that they have a decent income. Your retirement savings should first and foremost provide you with a pension and, if anything is left over once you die, then that should be considered a bonus. Your children can inherit your home and other possessions.

There may, however, be instances where inheriting a capital sum is needed.

Your children may be struggling financially and clearing their bonds may be just the fillip they need.

This is where this product comes into its own. You take a single life annuity in your name and, when you die, the amount you invested is paid out to your spouse or heirs.

If you chose this option, you would receive a monthly annuity of R13,000, increasing by 5% a year. When you die, R2.5-million would be paid out.

If your husband is still alive, he can use this to provide a pension for himself or it could be inherited by your children.

As you can see, there are a number of options open to you and each has its pros and cons.

A financial planner can help you make the right call for your specific circumstances. DM168

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for R25 at Pick n Pay, Exclusive Books and airport bookstores. For your nearest stockist, please click here.

Comments

Scroll down to load comments...