First published in the Daily Maverick 168 weekly newspaper.

Answer: Well done on doing a cash flow projection and picking up that you stand a good chance of running out of money. Many spot this when it is too late.

You are entering the danger zone as your drawdown percentage is greater than the returns you are getting and the costs of running the annuity.

You have a couple of options open to you:

- Reduce your drawdown;

- Choose a more aggressive portfolio for your living annuity; or

- Take out a life annuity.

Reducing your drawdown

If the pension you are taking cannot be sustained over the long term by your capital, you may have to make some uncomfortable lifestyle changes.

You may need to move to a smaller home, downgrade your medical aid, or look for where you can cut your budget.

These are not easy things to do but if you need to make a change, it is often better to recognise the reality while there is still room for manoeuvre than to be forced to make a drastic change later.

Portfolio choice

The challenge that many people face when it comes to choosing the right investment portfolio for a living annuity is to get one that provides you with the right level of growth over the longer term but also does not endanger the capital.

If you want good returns, you need to put some of your capital at risk but, if you are a pensioner, it can be catastrophic if the markets go down.

We have come off a couple of years where the investment growth has been flat, which has resulted in many people drawing down more than what the portfolio has returned. This means they are starting to use up some of their capital, which can be dangerous.

There are some clever portfolios constructed for living annuities that provide high returns at a low risk. This is done through the smart use of financial instruments such as hedges and guaranteed funds. This may be an easy way out of your current situation, so chat to someone who is familiar with these products.

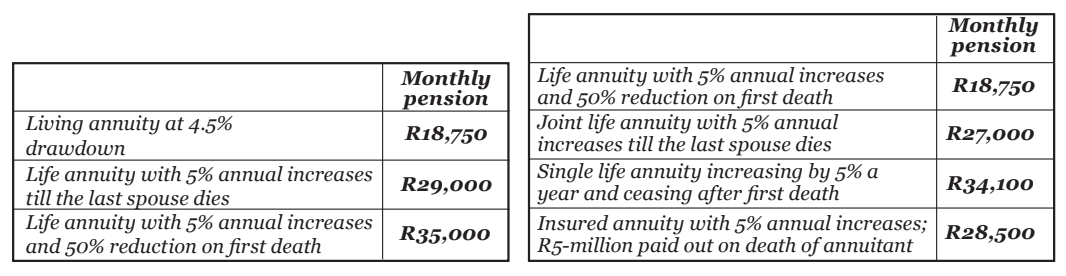

Life annuities

A life annuity will give you a higher income for the rest of your life than a living annuity. As your wife has no retirement savings, you need to go for a joint life annuity.

Your R5-million can fund a monthly pension of R29,000 that increases by 5% a year for the rest of your and your wife’s lives.

Age plays an important role in your initial annuity. Given that your wife is seven years younger than you, you may want to consider having the pension reduce when the first spouse dies.

If it reduces by 25%, the starting pension would be R32,000 and, if it reduces by 50%, then the starting pension will be R35,000.

As you can see, there are several options open to you because you have identified the problem early. I often come across problems when the room for manoeuvre is limited because it was identified too late.

Insider tip

If you have a living annuity, you need to take your income reviews seriously.

- Look at what the investment returns have been on your portfolio and project them forward.

- Subtract the annual costs of the investment.

- Look at your annuity income and see what percentage of the capital it will be in each year over the next 10 years.

If this is more than 7%, then you need to be careful and get the opinion of a professional.

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for R25 at Pick n Pay, Exclusive Books and airport bookstores. For your nearest stockist, please click here.