Shigeru Ishiba, Japan's prime minister and president of the Liberal Democratic Party (LDP), prepares to place a paper rose on an LDP candidate's name, to indicate a victory in the lower house election, with Yoshihide Suga, Japan's former prime minister and vice president of the Liberal Democratic Party (LDP), at the party's headquarters in Tokyo, Japan, on Sunday, Oct. 27, 2024. Japans Liberal Democratic Party is set to lose its majority in Sundays election, according to a forecast from public broadcaster NHK, leaving in the balance whether the ruling coalition will hold on to power.

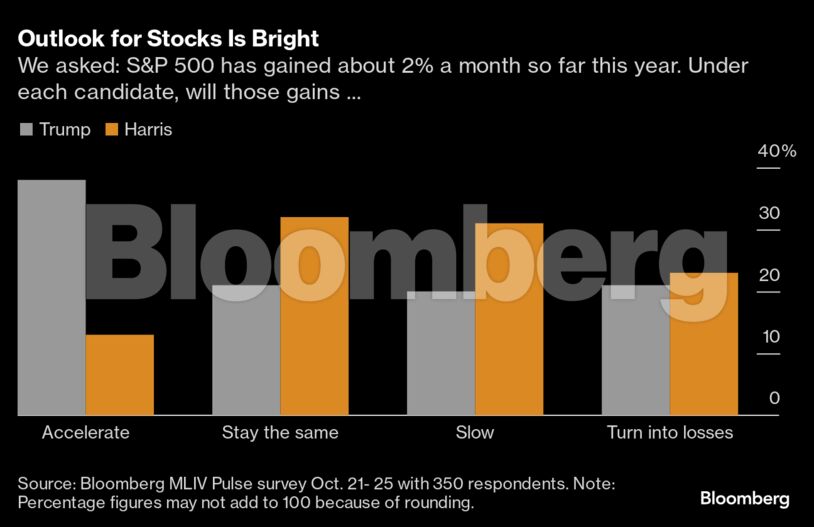

Shigeru Ishiba, Japan's prime minister and president of the Liberal Democratic Party (LDP), prepares to place a paper rose on an LDP candidate's name, to indicate a victory in the lower house election, with Yoshihide Suga, Japan's former prime minister and vice president of the Liberal Democratic Party (LDP), at the party's headquarters in Tokyo, Japan, on Sunday, Oct. 27, 2024. Japans Liberal Democratic Party is set to lose its majority in Sundays election, according to a forecast from public broadcaster NHK, leaving in the balance whether the ruling coalition will hold on to power. A victory for Trump would be more beneficial for stocks and Bitcoin relative to his Democratic opponent, while a Kamala Harris presidency would bring slightly more relief to housing costs, according to a Bloomberg Markets Live Pulse survey. Some 38% of the 350 respondents see equities accelerating a year from now under the Republican candidate, versus 13% under the Democrat.

“Markets have been extremely active over the past month as traders have juiced up the already ebullient scenario baked into equity valuations, adding improved odds of a Republican sweep to the list of goodies discounted,” said Lisa Shalett at Morgan Stanley Wealth Management.

A week before Fed gathers to reflect on the appropriate tempo of rates cuts, data is set to show underlying resilience in the US economy and a temporary hiccup in jobs growth. Investors are also awaiting results from firms accounting for nearly 42% of the S&P 500’s market capitalization, including several big techs like as Apple Inc., Microsoft Corp. and Meta Platforms Inc.

“This week’s megacap tech earnings and jobs data will provide plenty of potential fuel for near-term market momentum, but it remains to be seen whether investors will want to sit on their hands until after next week’s election, especially given the volatility around the past two,” said Chris Larkin at E*Trade from Morgan Stanley.

The S&P 500 rose 0.3%. The Nasdaq 100 added 0.2%. The Dow Jones Industrial Average gained 0.6%. The Russell 2000 of small caps climbed 1.5%.

Treasury 10-year yields rose five basis points to 4.29%. The yen dropped as much as 1% before paring losses as investors mulled the implications of the Liberal Democratic Party and its coalition partner losing their majority.

With the US election in sight, many investors continue to second-guess whether their portfolios are well-positioned for whatever lies ahead.

To Saira Malik at Nuveen, it is critical to remain focused on long-term investment goals and attentive to the broader economic backdrop and company fundamentals, as election-driven volatility has historically been short-lived.

“With that in mind, corporate earnings, inflation and the direction of interest rates should continue to be the structural drivers of financial markets,” she said. “This was evident in the recent backup in US Treasury yields after they bottomed in mid-September following the Federal Reserve’srate cut. Since then, the uptick in yields, paired with underlying fundamentals, may have created another attractive entry point for one of our favored fixed-income sectors.”

Although the polls are extremely tight, and it’s anyone’s race to win, the stock and bond markets have shown recent momentum that appears to favor a result that puts former President Trump back in the White House, according to Anthony Saglimbene at Ameriprise.

“Government bond yields have risen, the US dollar has strengthened, and areas of the stock market that would benefit from less regulation and lower taxes have ground higher,” he said. “Some of this is related to a strong economy and growing profits, while some of this momentum may be attributed to investors increasingly discounting a Trump victory.”

Off to the races or sell the news?

“In our view, the market can perform well through year-end whether Vice President Harris or former President Trump wins in November,” he said. “We believe fundamental conditions in the US are solid, seasonality factors/historical trends are favorable for stocks, and known election results, which let investors finally move on from the election, could see major equity averages press higher into the end of the year.”

Key events this week:

- US job openings, Conference Board consumer confidence, Tuesday

- Alphabet earnings, Tuesday

- Eurozone consumer confidence, GDP, Wednesday

- US GDP, ADP employment, pending home sales, Wednesday

- Meta Platforms, Microsoft earnings, Wednesday

- US Treasury Department holds quarterly refunding announcement of bond-auction plans, Wednesday

- China Manufacturing and non-manufacturing PMI, Thursday

- Bank of Japan rate decision, Thursday

- Eurozone CPI, unemployment, Thursday

- US personal income, spending and PCE inflation data, initial jobless claims, Thursday

- Amazon, Apple earnings, Thursday

- China Caixin manufacturing PMI, Friday

- US employment, ISM manufacturing, Friday

This is a modal window.

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.3% as of 11:59 a.m. New York time

- The Nasdaq 100 rose 0.2%

- The Dow Jones Industrial Average rose 0.6%

- The Stoxx Europe 600 rose 0.4%

- The MSCI World Index rose 0.3%

- Bloomberg Magnificent 7 Total Return Index rose 0.3%

- The Russell 2000 Index rose 1.5%

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro rose 0.2% to $1.0819

- The British pound rose 0.1% to $1.2981

- The Japanese yen fell 0.6% to 153.22 per dollar

Cryptocurrencies

- Bitcoin rose 1.1% to $68,423.85

- Ether rose 0.4% to $2,498.2

Bonds

- The yield on 10-year Treasuries advanced five basis points to 4.29%

- Germany’s 10-year yield was little changed at 2.29%

- Britain’s 10-year yield advanced two basis points to 4.25%

Commodities

- West Texas Intermediate crude fell 5.3% to $67.94 a barrel

- Spot gold fell 0.2% to $2,741.04 an ounce