Traders on the floor of the New York Stock Exchange. (Photo: Michael Nagle/Bloomberg)

Traders on the floor of the New York Stock Exchange. (Photo: Michael Nagle/Bloomberg) “The dovish commentary from Powell supports the narrative that inflation is trending lower, and the Fed would soon be cutting rates, underpinning ‘SMID-cap’ (small-mid) stocks,” said Craig Johnson at Piper Sandler. “The market broadening into ‘SMID-caps’ indicates a positive outlook for the remainder of the year.”

Monday’s action reprised a recent trend in which capitalization-weighted indexes underperformed the average stock, a consequence of weakness in the megacaps that dominate them. With firms such as Apple Inc. and Nvidia. each making up over 6.5% of the S&P 500, losses are hard to offset even when most of the index’s members are up.

Strong flows from corporate buybacks, systematic funds and retail investors are expected to push stocks higher in the coming weeks, according to Goldman Sachs Group Inc.’s Scott Rubner.

He estimates there will be $17 billion of “unemotional demand between robots and corporates every day this week.” Rubner also sees a so-called “green sweep” for commodity trading advisers, or CTAs, over the coming week, which means those funds will likely be buying stocks however the market trades.

The S&P 500 hovered near 5,620, with most of its major groups rising. Trading volume was 25% below the average of the past month. The Russell 2000 of smaller firms added 0.3%. The tech-heavy Nasdaq 100 fell 1%. A Bloomberg gauge of the “Magnificent Seven” megacaps sank 1.2%.

Treasury 10-year yields rose one basis point to 3.81%. Oil advanced after an Israeli strike on Hezbollah targets in southern Lebanon raised tensions in the Middle East and Libya’s eastern government said it will halt exports.

The market has been on a healthier track over the past few weeks, moving away from the overly strong reliance on a few big tech names that we saw in the first seven months this year, according to Mark Hackett at Nationwide. With that said, we are currently in what can best be described as a “market pause,” he noted.

“September is historically the worst month on the calendar, so investors should expect some volatility, especially if key indicators like the PCE inflation data, Nvidia earnings, or upcoming payroll disappoint. However, even with potential headwinds, it’s fair to expect a bounce back for the fourth quarter, particularly an election year, as we see the Fed begin to cut rates and share buybacks continue.”

To Chris Larkin at E*Trade from Morgan Stanley, in order to push to fresh highs this week, stocks may need to avoid any major surprises from earnings — especially Nvidia — “which has been driving a good deal of the sentiment in the tech sector.”

Expectations heading into the giant chipmaker’s earnings on Wednesday are high, with analysts anticipating another strong consensus beat that could prompt the chipmaker to raise its profit guidance. Trading in the options market suggest investors see potential for a 9% move in either direction on the day following the report, Citigroup Inc.’s Vishal Vivek said last week.

Its report this week will wrap up results for the “Magnificent Seven,” which in combination are on track to post 34% year-over-year growth in earnings for the second quarter — compared to 6% for the rest of the S&P 500, according to Jason Pride and Michael Reynolds at Glenmede.

This comes after a nearly year-long period in which the cohort of megacaps posted earnings growth of more than 40% — while the rest of the index saw outright declines.

“The back half of this year is likely to be the beginning of a process that gives way to broader fundamental improvement,” they said. “Broader earnings growth participation should favor small caps and investment processes that avoid the pitfalls of market concentration.”

“At current valuations, stocks are expensive and any further upside will depend on improving earnings,” said Richard Saperstein at Treasury Partners. “Abundant liquidity coupled with declining inflation and an accommodative central bank will provide the backdrop for higher stock prices.”

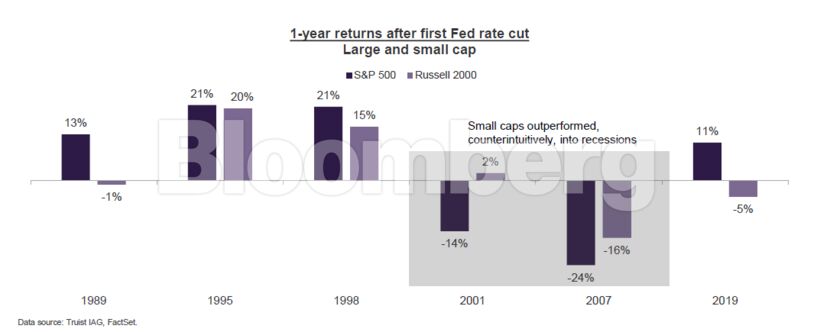

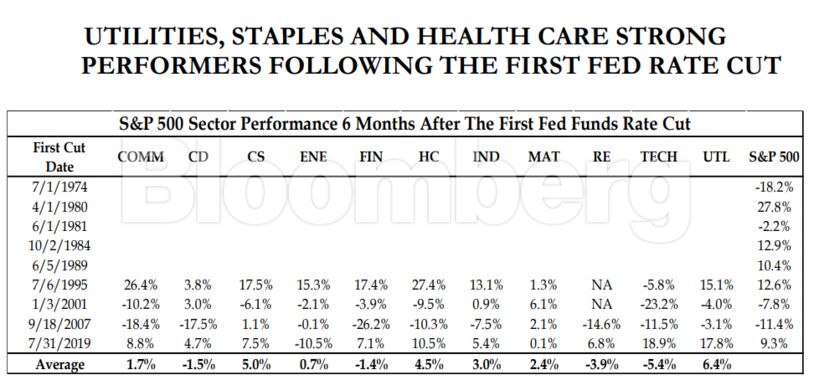

S&P 500 returns following the initial Fed rate cut tend to be positive — unless the economy falls into recession, according to Keith Lerner at Truist Advisory Services, who also notes that’s not his base-case scenario.

“Small caps are likely to do better in the near term, but longer term we still prefer large caps,” Lerner said. “Small caps are a greater beneficiary of lower short-term rates, and valuations are cheap. However, historical trends after first Fed rate cut are mixed, earnings trends are still weak, and a cooling economy is historically a headwind for the asset class.”

While it’s hard to stand in front of a market trending higher that is about to get rate cuts, we continue to think equities will show some consolidation around the area of prior highs, said Jonathan Krinsky at BTIG.

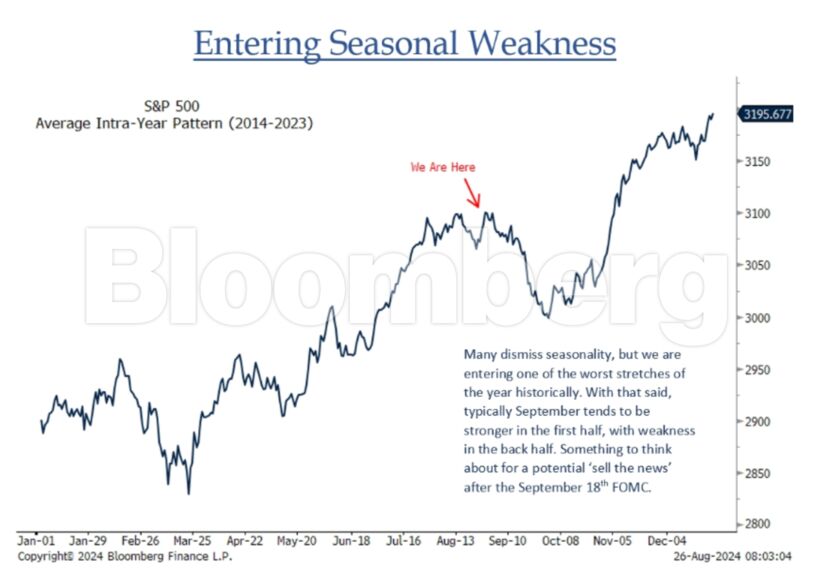

“No rush to push all your chips in right here, especially as we enter one of the worst seasonal stretches of the year,” Krinsky noted. “Small caps remain above their key breakout level, but we are more interested in the potential turn in the relative trend. Rate cuts should help this trade, assuming the eco data holds up.”

US inflation figures in the coming week will reinforce that long-awaited interest-rate cuts are coming soon, while a reading on consumer spending is seen indicating that the central bank has been successful at keeping the expansion intact.

Economists see the personal consumption expenditures price index excluding food and energy — the Fed’s preferred measure of underlying inflation — rising 0.2% in July for a second month. That would pull the three-month annualized rate of so-called core inflation down to 2.1%, a smidgen above the central bank’s 2% goal.

Corporate Highlights:

- Elliott Investment Management has increased its equity stake in Southwest Airlines Co. to 9.7%, nearing the amount needed to call a special shareholder meeting at which the activist hopes to replace most of the carrier’s board.

- Apple Inc. has sent out invitations for a product launch event at its headquarters on Sept. 9, when it’s likely to announce details of the iPhone 16 and other new devices.

- McKesson Corp. agreed to buy a controlling stake in an arm of Florida Cancer Specialists & Research Institute, a privately held operator of clinics.

- PDD Holdings Inc.’s shares tumbled after Temu’s owner warned that revenue growth will inevitably dwindle, highlighting the challenges of sustaining its pace of expansion against aggressive rivals like ByteDance Ltd.

Key events this week:

- China industrial profits, Tuesday

- Germany GDP, Tuesday

- US Conference Board consumer confidence, Tuesday

- Nvidia earnings, Wednesday

- Fed’s Raphael Bostic and Christopher Waller speak, Wednesday

- Eurozone consumer confidence, Thurrsday

- US GDP, initial jobless claims, Thursday

- Fed’s Raphael Bostic speaks, Thursday

- Japan unemployment, Tokyo CPI, industrial production, retail sales, Friday

- Eurozone CPI, unemployment, Friday

- US personal income, spending, PCE; consumer sentiment, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 fell 0.3% as of 12:26 p.m. New York time

- The Nasdaq 100 fell 1%

- The Dow Jones Industrial Average rose 0.2%

- The MSCI World Index fell 0.2%

- Bloomberg Magnificent 7 Total Return Index fell 1.2%

- The Russell 2000 Index rose 0.3%

Currencies

- The Bloomberg Dollar Spot Index rose 0.3%

- The euro fell 0.2% to $1.1166

- The British pound fell 0.2% to $1.3193

- The Japanese yen was little changed at 144.50 per dollar

Cryptocurrencies

- Bitcoin fell 0.9% to $63,635.71

- Ether fell 1.8% to $2,722.7

Bonds

- The yield on 10-year Treasuries advanced one basis point to 3.81%

- Germany’s 10-year yield advanced two basis points to 2.25%

- Britain’s 10-year yield declined five basis points to 3.91%

Commodities

- West Texas Intermediate crude rose 2.9% to $76.98 a barrel

- Spot gold was little changed