Market vendors in the Randburg Central Business District of Johannesburg, South Africa, on Monday, Sept. 4, 2023. South Africas National Treasury warned other government departments that it is confronting significant budgetary challenges and spending needs to be reined in if it is to meet its debt-stabilization targets.

Market vendors in the Randburg Central Business District of Johannesburg, South Africa, on Monday, Sept. 4, 2023. South Africas National Treasury warned other government departments that it is confronting significant budgetary challenges and spending needs to be reined in if it is to meet its debt-stabilization targets. A new government, formed by the African National Congress with business-friendly parties after it lost its outright majority in May 29 elections, has committed to accelerating reforms to boost economic growth. A top priority is fixing its ports and rail networks.

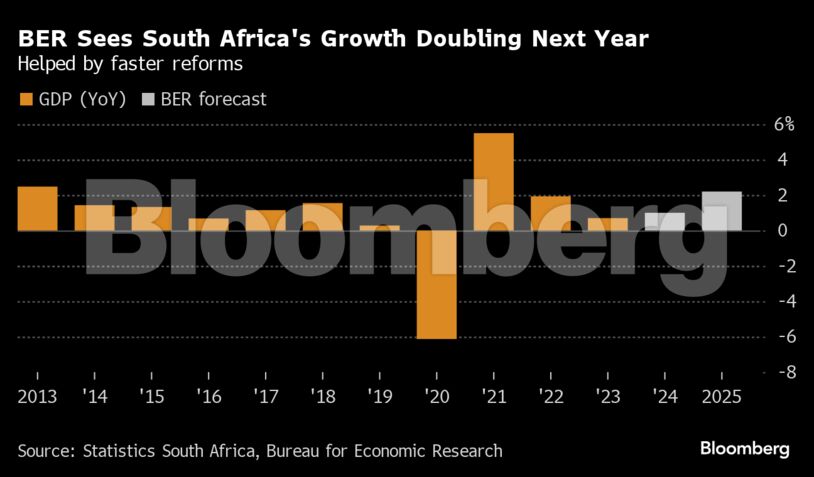

“Logistics disruptions should be less constraining,” Shannon Bold, senior economist for macroeconomic modeling and forecasting at the BER said in a presentation, noting that a return in consumer and business sentiment is expected.

The new government’s commitment to mobilize investments and speed up reforms with the aid of Operation Vulindlela, a 2020 initiative between the Presidency and National Treasury, bodes well for growth, the BER said.

The agency’s work has helped generate investment potential of 500 billion rand.

BER said lower inflation, a stronger currency and interest rate cuts should also help lift growth. While South Africa’s inflation rate remains above the midpoint of the central bank’s 3% to 6% target band, where it prefers to anchor expectations, the bank now sees it moderating to 4.3% in the last quarter of 2024.

That could prompt policymakers to lower borrowing costs, potentially as soon as September, provided price pressures soften as expected.