A customer signs for a purchase with a Barclaycard MasterCard chip credit card at a Wal-Mart Stores Inc. location in Burbank, California, U.S., on Tuesday, 22 Nov. 22, 2016. Consumer hardline retailers are hopeful Black Friday will provide a strong start to the holiday shopping season, but any lift may come at the expense of margins, as the landscape has become increasingly promotional. Photographer: Patrick T. Fallon/Bloomberg

A customer signs for a purchase with a Barclaycard MasterCard chip credit card at a Wal-Mart Stores Inc. location in Burbank, California, U.S., on Tuesday, 22 Nov. 22, 2016. Consumer hardline retailers are hopeful Black Friday will provide a strong start to the holiday shopping season, but any lift may come at the expense of margins, as the landscape has become increasingly promotional. Photographer: Patrick T. Fallon/Bloomberg “Despite the many headwinds American consumers have faced over the last year — higher interest rates, post-pandemic inflationary pressures, and the recent banking failures — there is little evidence of widespread financial distress for consumers,” the economists wrote in the post.

Credit card holders have, in aggregate, $3.6 trillion in additional credit availability.

Total US household debt rose by 0.1% to a record $17.06 trillion last quarter, according to the New York Fed, whose data go back to 2003.

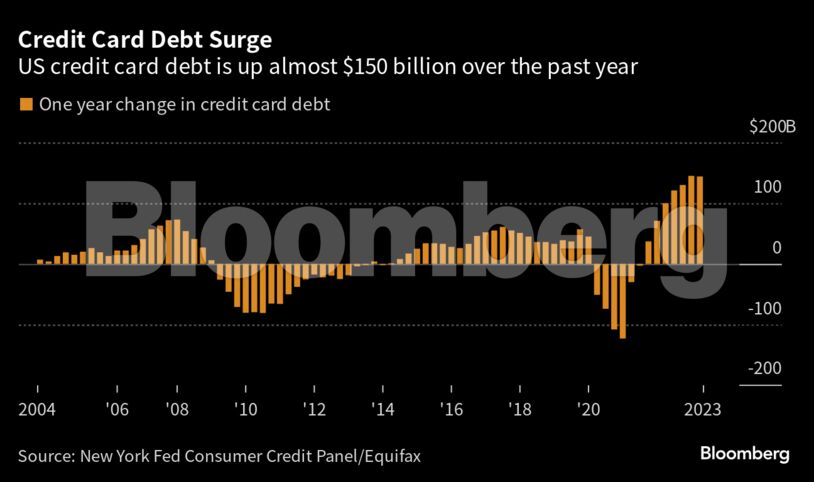

A separate report from the US Federal Reserve indicated that the interest-rate for credit cards reached a record high of 22.2% in May. More than 70 million new credit card accounts have been opened since the start of pandemic.

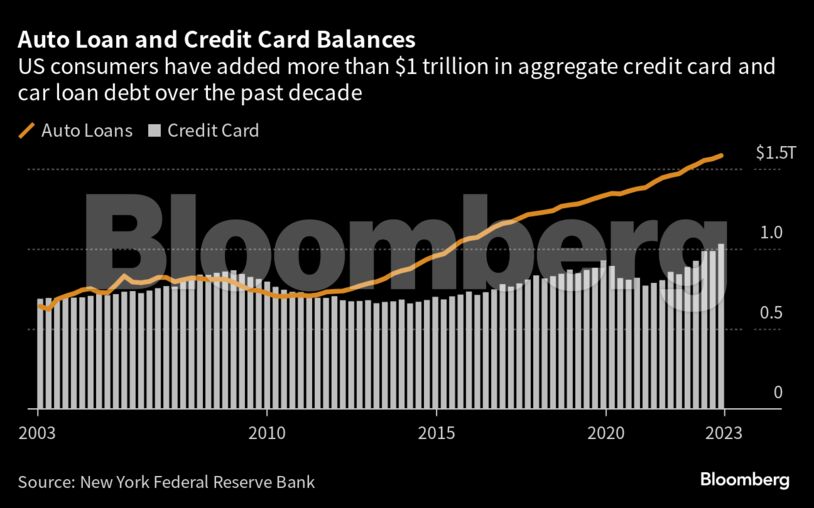

Auto-loan balances rose by $20 billion to $1.58 trillion, and exceeded student debt for the first time since 2009, the New York fed report shows. The volume of newly originated auto loans, which includes leases, was $179 billion.

Student-loan balances fell by $35 billion and stood at $1.57 trillion. Federal student loan payments remain suspended until October.

More than 70% of household debt is made up of mortgage balances. They were largely unchanged last quarter, at $12 trillion. Slow mortgage origination growth due to a sharp uptick in interest rates have kept depressed home-purchase applications.