Business Maverick

Bank of Russia rode rouble rally when war left few other options

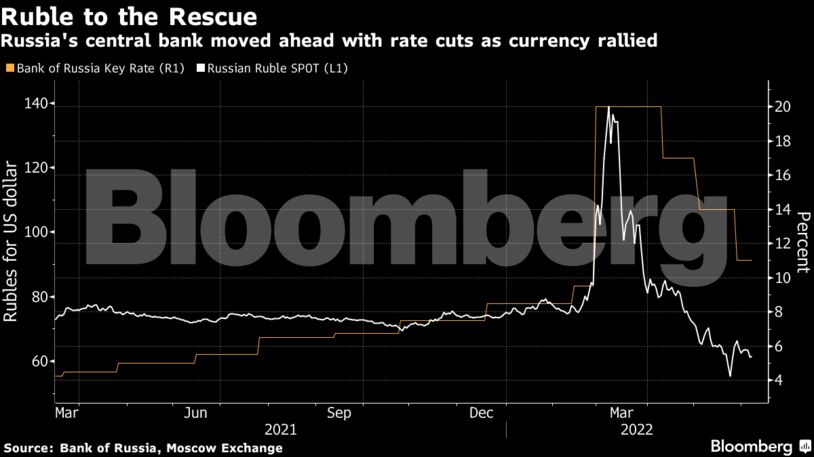

Some economists say the country's central bank could lower the benchmark below its pre-war level of 9.5% on Friday. It would be the fourth straight cut, a series that started as the rouble wiped out the losses incurred after Russia's invasion of Ukraine began.

Instead of acting faster to dismantle restrictions on the cross-border flow of money, the choice three months ago was to hold out as long as possible even at the cost to the budget, the people said. Only once a stronger rouble made enough of a dent on inflation would the central bank move aggressively to lower interest rates from the highest in almost two decades, they said, requesting anonymity to speak openly about the deliberations.

The culmination of what insiders describe as Nabiullina’s tactical manoeuvre may come on Friday, when some economists think the central bank could lower the benchmark below its pre-war level of 9.5%. It would be the fourth straight cut, a series that started as the rouble wiped out the losses incurred after the invasion began.

“The strategy is clear, first let the rouble strengthen to fight inflation,” said Oleg Vyugin, a former top central bank and Finance Ministry official. “But there is one catch: this tactics makes sense if imports recover and then bring at least a relative balance to trade. But imports aren’t recovering yet. And that’s a problem.”

The central bank didn’t respond to a request for comment.

Turnaround Job

Just days before the start of her third term later this month, Nabiullina might feel vindicated because inflation has cooled off so much that Russia saw rare weekly declines in consumer prices.

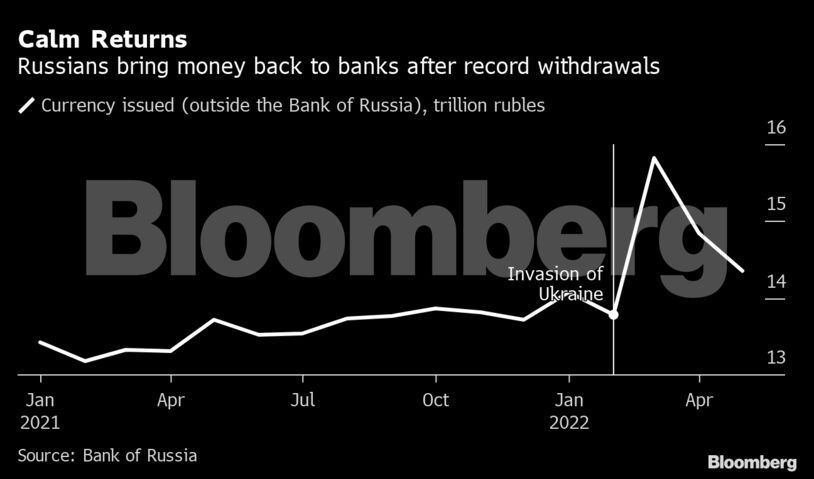

The broader outlook is also turning more favorable, with some forecasters seeing a far more shallow recession this year than anticipated earlier. Higher rates have prompted more Russians to return money to banks after record withdrawals starting in February.

But the central bank’s anti-crisis arsenal is less well suited for the risks ahead, from economic regression under sanctions to the threat of shortages as supplies of imported goods run dry. And with about half of Russia’s international reserves frozen by sanctions, policy makers are still unable to intervene in the market.

This week’s rate decision will go a long way toward showing just how much longer the central bank wants to rely on a strong rouble as a policy anchor, especially if it decides to complement monetary stimulus with an additional relaxation of capital controls.

Although the Bank of Russia gradually began to roll back its financial defenses from April, some of the harshest measures remain, including a ban on sales of Russian securities by foreign investors.

Most analysts surveyed by Bloomberg predict a rate cut of one percentage point on Friday to 10%. Inflation slowed more than forecast in May, reaching an annual 17.1%.

JPMorgan Chase & Co.’s economists expect the rouble’s performance will largely dictate the pace and extent of the easing cycle. Rates may even need to go below a level deemed neutral – 6% to 8% – to revive consumer spending and balance out surging exports, they said.

Otherwise the rouble will remain at the mercy of the current account.

“To reduce the current-account surplus notably – via higher imports – a significant policy easing to heat up domestic demand might be needed,” JPMorgan economists including Yarkin Cebeci said in a report. “The Finance Ministry is doing its part via a large fiscal stimulus, but a stronger monetary impulse may also be needed.” BM

Comments - Please login in order to comment.