“The US manufacturing sector remains in a demand-driven, supply chain-constrained environment,” Timothy Fiore, chair of ISM’s Manufacturing Business Survey Committee, said in a statement. He added that “sentiment remained strongly optimistic regarding demand, with five positive growth comments for every cautious comment.”

The report also points to lingering capacity constraints related to labor, shipping delays and materials shortages. ISM’s measure of factory employment drifted into contraction territory for the first time since November 2020, and the group’s gauge of delivery performance, despite settling back some, remained elevated.

“Employment levels, driven primarily by turnover and a smaller labor pool, remain the top issue affecting further output growth,” Fiore said.

In a sign that overall labor demand is still robust, a separate report on Wednesday showed job openings in April remained close to a record.

Read more: Job Openings Decline From Record While Remaining Elevated

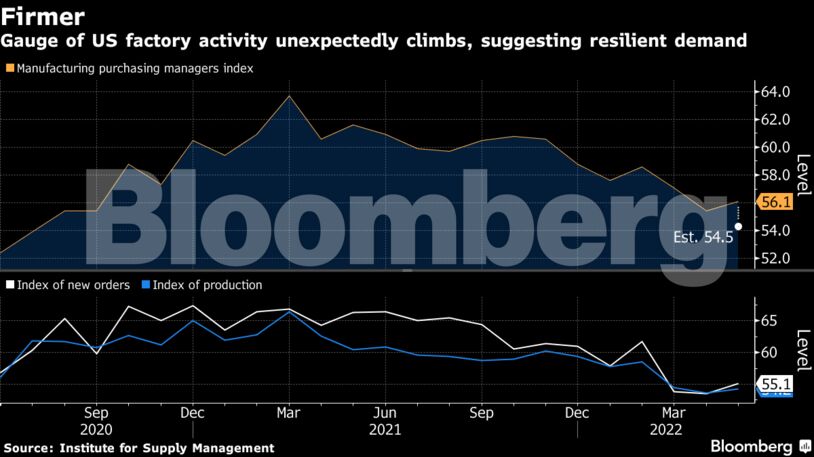

While the ISM index of new orders at factories hit a three-month high, the production gauge was up more modestly. Backlogs also increased.

Average lead times for capital expenditures grew to 178 days, the highest in data back to 1987. Production materials lead times eased to 99 days from a record 100 days a month earlier.

Fifteen manufacturing industries reported overall growth last month, led by apparel, printing and machinery.

The ISM index of factory inventories advanced to the highest since November, as purchasing managers strive to ensure their firms have enough finished product on hand in a still-challenging logistics environment.

Select ISM Industry Comments

“The challenge with semiconductors hasn’t softened; the situation is worsening due to Chinese Covid-19 lockdowns.” – Transportation Equipment

“Input costs, particularly grain, oil, dairy and protein, are rising faster than can be passed along at retail and food service, with no relief in sight.” – Food, Beverages & Tobacco

“Our order books are still strong. Material prices continue to rise, with energy and freight noted as the underlying influences on increased costs.” – Machinery

“While orders remain strong and backlogs exist, there’s a softening in forecasted orders for leading indicator-type customers and business units.” – Chemical Products

“Supply chain issues are causing us to dramatically extend our lead times. Our production lines have (run) low on or out of parts needed to complete rates every week this month.” – Miscellaneous Manufacturing

“Price increases haven’t let up. I thought 2022 was going to be better, but it hasn’t been. Shortages (among other issues) are still disrupting the supply chain.” – Plastics & Rubber

The customer inventories gauge, meanwhile, showed stocks shrank at the fastest rate in three months. That may help explain the pickup in orders to manufacturers as well as ease concerns about the inventory overhang at some retailers.

A measure of prices paid by producers slipped from the prior month but remains historically high. The costs of crude oil and petroleum products continue to climb, while prices of some other commodities such as aluminum and steel have softened.

The ISM results stand in contrast to several regional Federal Reserve bank surveys that showed a clear pullback in factory activity. Gauges of manufacturing in New York state and Texas, along with the Richmond and Philadelphia Fed regions, all declined in May from the prior month.

Comments - Please login in order to comment.