(Illustration: iStock)

(Illustration: iStock) The average monthly contribution to belong to a medical scheme is R2,104, according to the Council for Medical Schemes. However, medical scheme membership does not mean that your medical costs will necessarily be covered in full if you are admitted to hospital. And that’s where gap cover comes in – to cover the co-payment.

“The reality is that medical scheme cover can cost 20% or more of monthly disposable household income. If you consider the hyper-inflationary growth in healthcare costs, the annual medical scheme increases of 8% to 10%, and the fact that salary increases have declined to lows of 3% to 4% annually, if at all, it is clear that medical schemes costs are eating into a much greater share of monthly household income than ever before,” says Martin Rimmer, CEO of Sirago Underwriting Managers.

Gap cover is a form of short-term insurance that shields you and your family from unexpected shortfalls on medical expenses for in-hospital procedures and specific out-patient procedures, helping to avert potential financial catastrophe after a major medical event.

Jill Larkan, head of healthcare at GTC Consulting, says gap cover is often misunderstood. “You must have medical scheme membership because gap cover is complementary to it and does not replace a medical scheme. It’s not intended to cover specialist costs unless that specialist is treating you in hospital and there must be a partial payment from your medical aid,” she explains.

Gap insurance covers the difference that arises from the rate that specialists charge for in-hospital procedures – which are often as high as 300% to 500% higher than the rate paid by your medical scheme. For example, if your medical scheme option only pays out at 100% of tariff, you will then be liable to pay the shortfall of the other 200% to 400% charged by your healthcare provider as an “out of pocket” expense.

Out-of-pocket expenditure for hospital services increased at an annual rate of 14.9% between 2013 and 2019, according to a study by the Board of Healthcare Funders’ Southern African Health Journal. Rimmer explains that shortfalls occur in several ways, including:

Out-of-pocket expenditure for hospital services increased at an annual rate of 14.9% between 2013 and 2019, according to a study by the Board of Healthcare Funders’ Southern African Health Journal. Rimmer explains that shortfalls occur in several ways, including:

- Surgeons, anaesthetists and other specialists charge more than the contracted/agreed rate with your medical scheme for certain in-hospital procedures;

- Your medical scheme applies co-payments or deductibles on certain in-hospital admissions and/or procedures; and

- Certain in-hospital items and appliances have annual sub-limits, for example, the internal prosthetic devices used in a joint replacement procedure.

To keep up with inflation, medical scheme contributions go up each year whereas benefits tend to increase at a lower rate. Inflation (CPI) is about 5.5% and medical inflation would be estimated to be 7.5% to 8%.

Bianca Viljoen, marketing director at Agility Health, says tariff increases higher than inflation are largely driven by ageing and an increasing burden of disease as well as supply-side use increases such as new technology and drugs. Last year was the first year in more than a decade in which average medical scheme contribution increases at 2.9% were below inflation. This was largely the result of guidance from the Council for Medical Schemes and efforts by medical schemes to provide members with financial relief during Covid-19.

Lee Callakoppen, the principal officer of Bonitas Medical Fund, says hospital admissions are one of the biggest cost drivers for private medical schemes and concerns about increased usage and higher tariffs are widely expected to lead to more co-payments for medical scheme members.

South Africans who usually negotiate costs for services such as plumbing and repair work are yet to wake up to the fact that medical specialist costs are not regulated or set in stone.

Rimmer says you should always negotiate the pricing of any planned surgery with healthcare providers before and ask for a formal quote. “That way there are no surprises or unexpected costs creeping in after the fact that you would find difficult to dispute, unless there were specific complications during the procedure. Finally, be wary of doctors asking you upfront whether you have gap cover or not – overbilling based on a client’s insurance portfolio is a growing unethical practice by some unscrupulous medical specialists looking to capitalise on the patient’s insurance cover by overcharging, knowing that the patient has the insurance to cover the inflated price,” he warns.

When choosing gap cover, Michael Emery, marketing executive at Ambledown Financial Services, suggests you speak to a financial adviser. “Don’t always go for the product with the most benefits. The right level of cover should minimise shortfalls with gap cover of up to 600% less the medical scheme reimbursement rate. It should assure members of the latest, correct overall limitation as stipulated by the regulator.”

At the upper end, gap cover options could help you to pay medical hospital admission co-payments, and may even offer cancer cover and dread disease benefits.

Emery emphasises that your gap cover provider should be easily accessible to you. This translates to a service provider that has easy registration processes; can settle claims using online or mobile technologies; and has a track record of paying claims quickly. “Ideally, you should be able to register or submit a claim quickly and easily via your mobile phone and have access to 24/7 ambulance medical assistance. A Covid-19 self-assessment screening and support line would also be helpful,” he says.

If you have gap cover, the onus is on you to submit claims to your provider. Your provider also does not have to be the same company that administers your medical scheme. For example, belonging to Discovery Medical Scheme does not mean you have to take out gap cover with Discovery. You could use a different gap cover provider.

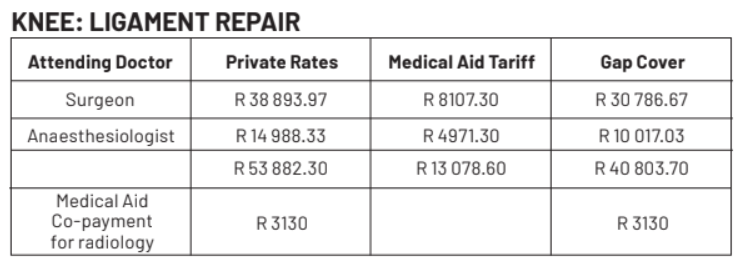

Ambledown Financial Services provided the following examples of costs for two procedures – removal of tonsils and repair of a knee ligament – to illustrate how gap cover could be used. DM168

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for R25 at Pick n Pay, Exclusive Books and airport bookstores. For your nearest stockist, please click here.