The result is a physical market for crude too chaotic even for veteran oil traders who have spent years deftly handling everything from political sanctions to trade wars and attacks on key infrastructure. In the current climate, traders say, even an action as simple as a seller knowing what price to offer their crude at has become confusing.

“Geopolitics are throttling supply chains and keeping markets on edge,” said John Driscoll, a Singapore-based chief strategist at JTD Energy Services Pte. The wild swings in intraday trading ranges, volatility and backwardation are “scary,” he said.

Commodity markets have been in turmoil since the invasion. While sanctions haven’t directly targeted Russian energy exports, trade has seized up amid a reluctance to buy the country’s raw materials. Oil majors, international banks and shipowners are pulling investment and financing, making it tough for refiners and traders to secure credit lines and the vessels needed to continue with their usual purchases of oil grades like Urals, ESPO and Sokol.

Russia accounted for 12% of the world’s total crude exports in 2020 and almost 10% of oil-product shipments. Oil trading giant Trafigura Group tried to sell a cargo of Russia’s flagship Urals grade this week at a record discount to benchmark prices for northwest Europe but found no bidders, highlighting how toxic trade with the country has become.

See also: Chaos in Commodities as Russia’s War on Ukraine Upends Trade

Asian refiners are trying to snap up more Middle Eastern oil, although incremental supplies from the region are very limited, the traders said. More U.S. cargoes are also in their sights, but backwardation, surging transport costs and wild divergences in global benchmarks are making that challenging. Their European counterparts are looking to buy more North Sea crude, which may price Chinese and South Korean refiners out of that market, the traders said.

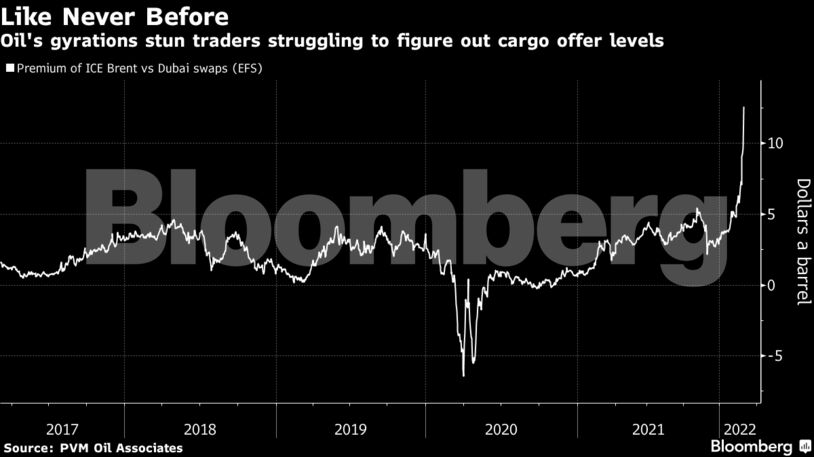

Physical differentials are surging with traders finding it hard to keep up. U.S. WTI Midland crude delivered to Asia was notionally pegged at a staggering premium of more than $15 a barrel over the Dubai benchmark price this week. That’s in part due to gyrations in the relative price of benchmarks such as Brent, West Texas Intermediate and Dubai, with the premium of Brent futures to Dubai swaps at almost $13 a barrel on Wednesday, the widest in data going back to 2006.

For sellers with oil not implicated by sanctions, the wide geographic differentials, expensive shipping rates and record premiums for prompt delivery are making it difficult to know at what level to price their offers, traders said.

In fuel markets, the invasion of Ukraine has caused steep backwardations, a market structure where prompt supplies are more expensive than later-dated cargoes. Buyers are struggling to find replacements for Russian diesel, as well as heavy naphtha, mainly used by the petrochemicals industry, and vacuum gasoil, a feedstock for gasoline production.

Russian exports of these products typically flow to buyers across Asia, Europe and the U.S. There’s no immediate answer to the question of where alternatives will be found as fuel stockpiles have been rapidly shrinking over the last few months, the traders said.

Comments - Please login in order to comment.