From left: Krugerrands. (Photo: Gallo Images / Maryann Rivers-Moore) | South African banknotes. (Photo: Simon Dawson / Bloomberg via Getty Images) | A SARS office in Johannesburg. (Photo: Gallo Images / Luba Lesolle) | A foundry worker pours molten gold into a mould. (Photo: Andrey Rudakov / Bloomberg via Getty Images)

From left: Krugerrands. (Photo: Gallo Images / Maryann Rivers-Moore) | South African banknotes. (Photo: Simon Dawson / Bloomberg via Getty Images) | A SARS office in Johannesburg. (Photo: Gallo Images / Luba Lesolle) | A foundry worker pours molten gold into a mould. (Photo: Andrey Rudakov / Bloomberg via Getty Images) The South African Revenue Service (SARS) has conducted a wide-ranging confidential investigation into the second-hand gold industry and found what appears to be a staggering, multibillion-rand tax fraud scheme.

The scheme is immense in scale, with just two companies claiming R24.4-billion between 2012 and March 2020 in allegedly fraudulent VAT refunds, according to an affidavit filed by SARS in the Johannesburg High Court.

The two companies appear to have scored illegitimate VAT refunds of over R8-billion in 2019 alone – roughly half a percent of SARS’ entire tax collection for the year.

In that year, the scheme allegedly involved amounts of gold equal to an astonishing 70% of all gold legally mined in South Africa in 2019 – again only counting the activities of these two players.

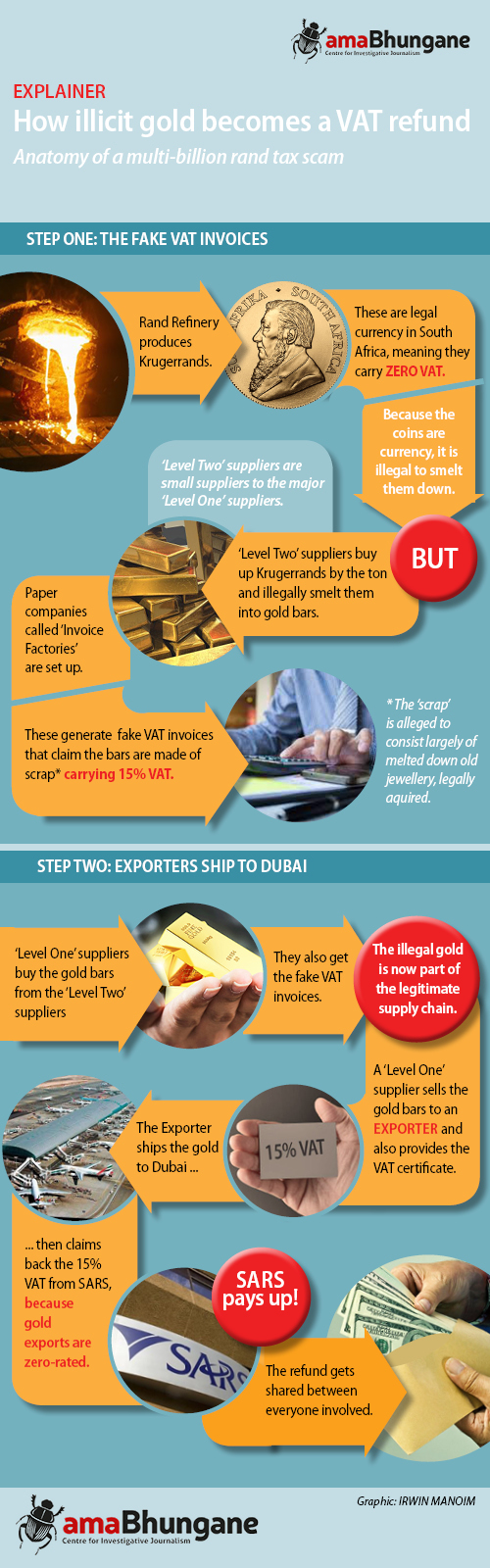

The scheme laid out by SARS is simple in principle. Gold exports are zero-rated for VAT. Buying gold scrap locally, however, carries the standard 15% VAT.

If you can find a way to buy large amounts of gold for export, without paying the obligatory VAT, you can claim 15% of the value of the gold as a refund from SARS on tax you never actually paid.

Key to the scheme is introducing untaxed gold into the supply chain and faking VAT payments for this gold.

SARS fingers Rappa

One of the two companies cited is Rappa Resources, a Germiston-based gold trader currently locked in a court battle with the taxman.

Rappa went to court after SARS withheld VAT refunds totalling R1.8-billion purportedly owed to the company for February to June 2020.

The case has forced SARS to reveal details about its closely guarded investigation.

The revenue service has subsequently raised a gargantuan assessment of R7-billion against Rappa for its allegedly illegitimate VAT claims between January 2019 and March 2020, another illustration of the scale of its seemingly tainted gold export business.

Rappa has in turn launched a second case against the revenue service, challenging this assessment.

In interim skirmishes, SARS has suffered some setbacks, including a stern rebuke for its apparent tactic of indefinitely withholding billions in refunds while it is still completing an investigation into Rappa.

Judge Seena Yacoob slammed the revenue service and noted that it would make the Tax Administration Act “inherently unfair towards the taxpayer” if SARS didn’t change tack.

SARS also challenged Rappa’s decision to bypass the specialised tax court and go directly to the Johannesburg High Court. The court ruled against SARS but allowed an appeal to the Supreme Court, which will have to be decided before the main case goes ahead.

Nevertheless, the court papers for the two high court cases, which exceed 3,000 pages, provide an eye-watering glimpse into an alleged criminal underworld operating in the shadow of South Africa’s formal gold industry.

SARS’ actions against Rappa follow an extensive inquiry into gold trading launched by the revenue service in March 2019 when Rappa was summoned as a witness, court papers show.

The first suspect was a competitor, Aesha Refineries, and a coterie of big second-hand gold dealers suspected of dealing in “illicit” metal. These dealers are suppliers to Rappa. At least two of these dealers were targeted in search and seizure operations in 2019, according to the court papers.

Dozens of tiny suppliers of allegedly illicit gold to these dealers are also under the microscope.

AmaBhungane has also learned that some of them are subject to a criminal investigation by the Directorate for Priority Crime Investigation (DPCI). This includes Rappa and 64 other companies, according to an affidavit by Lt-Col Mark de Bruin of the DPCI dated 30 June 2020, which supported subpoenas for information from banks.

The alleged scheme

The SARS investigation centres on the modus operandi of companies in the second-hand gold sector.

The tax authority accuses major players of introducing smuggled or illegally mined gold and illegally smelted Krugerrands (which attract no VAT) into the “legal” gold supply chain.

They do this, SARS claims, by fraudulently presenting the gold as second-hand (such as from purchased jewellery) and thereby enabling fraudulent VAT refunds to be claimed.

According to an affidavit by Gerald Motadi, a senior manager at SARS, there is a general pattern: “In the majority of cases, [they are] generating fictitious tax invoices that falsely represent that the taxpayer purchased second-hand gold jewellery from a VAT vendor, thereby claiming input tax based on purported standard-rated goods.”

To do this, according to Motadi, the fraudsters would often use “invoice factories” – companies set up to generate fake invoices for the gold dealers.

Alternatively, the gold traders generate the fake invoices themselves. In instances uncovered by SARS, the gold was ostensibly bought from “businesses” registered in random people’s houses. It is unclear whether these individuals always knew what was going on.

From there the gold is sold “up” a supply chain and ultimately exported, at which point the fraudulent VAT refund is claimed. According to SARS, the proceeds of the fraud are shared along the supply chain.

SARS alleges Rappa is one of the exporters that knowingly sits at the apex of these illicit gold supply chains and profits from them, although the company vehemently denies this.

Rappa buys gold ostensibly derived from “scrap” and old jewellery and exports it to clients “based in Europe or Dubai”, according to its court papers.

Rappa’s version of its business model is simply that it collects a minor margin of around 3% on the buying and exporting of gold and that its position is VAT neutral in that it claims to pay out the same amount of VAT it then claims from SARS.

“There is no factual basis to suggest that Rappa is involved in any criminal conspiracy to fraudulently claim VAT refunds. SARS has deliberately attempted to derail and delay court hearings by instituting dilatory procedural obstacles and SARS is guilty of unlawful and improper conduct,” Rappa said in a letter in response to questions from amaBhungane.

Aesha, the original subject of the SARS inquiry, is another exporter and the two allegedly share many gold suppliers. It has subsequently ceased operations.

According to Motadi: “The exporter will typically acquire gold-bearing bars, which it exports at a zero-rate, from its suppliers (“level 1 suppliers”). The suppliers to the level 1 suppliers are level 2 suppliers. The suppliers to the level 2 suppliers are level 3 suppliers, and so forth.

“The purpose of these levels is to disguise the source of the gold and to create distance between the source and the end supplier/exporter… The end supplier in the supply chain is the exporter of the gold.”

The supply chains are seemingly impossible to pin down.

“SARS observed that as soon as suppliers were assessed, they would disappear and new suppliers would enter the market. This later morphed further in that new suppliers would fit in vertically below direct suppliers to Rappa Resources, i.e. a multi-layered supply chain.”

While the so-called level 2 and 3 suppliers are ephemeral, there are several major level 1 suppliers from whom Rappa and Aesha have sourced material for years. These companies were also targets in SARS’s inquiry.

A significant finding in SARS’ investigation is that these companies handle amounts of gold that cannot be explained away as scrap jewellery.

The real Kruger millions

The scheme requires gold – lots of it. Between 2012 and mid-2020, Rappa and another unnamed company (possibly Aesha) exported 286 tons of the precious metal.

According to SARS, the sources include gold illegally mined by “zama zamas” and gold smuggled from Zimbabwe, Dubai and elsewhere.

A major source has been Krugerrands, SARS asserts. The iconic gold coins are easy to procure and are classified as currency, so they carry no VAT. It is, however, a crime to smelt them down.

Statistics provided by SARS in its court documents demonstrate how the coins almost certainly sit at the core of the multibillion-rand scam.

In 2019, Rappa and the unnamed exporting refinery’s export sales reached a peak of 83 tons. That is the equivalent of 70% of the total gold production of all South African gold mines that year. These exports were worth about R53.7-billion.

Most importantly, the VAT that was allegedly fraudulently claimed amounted to a whopping R8.16-billion.

These exports grew at a heady pace from 2014 onwards. The growth almost perfectly correlated with total national sales of Krugerrands by Rand Refinery, which is the sole supplier of bullion Krugerrands to primary distributors both locally and internationally.

To be more specific, between 2014 and 2019, the annual exports of Rappa and the one other exporter grew by 89%, while the annual supply of Krugerrands grew by 93%.

SARS argues that the “scrap” being exported is to a very large extent illegally smelted Krugerrands.

This begs the question why Rand Refinery never flagged the sudden massive increase in demand for its signature product – a product produced on behalf of the Reserve Bank – and whether it conducts proper due diligence on buyers.

The private refinery is jointly owned by major gold mining companies, but the Krugerrands are produced by a joint venture with the SA Mint (a subsidiary of the reserve bank), called Prestige Bullion.

Rand Refinery told amaBhungane that it is “always concerned about any illicit activities, but are cognisant that there are many reasons for high demand and that the demand cannot be isolated to illicit activities alone.

“We, however, continue to act with due care and diligence on behalf of our stakeholders and the industry as a whole and remain highly vigilant about sudden changes in market demand… we are not aware that any of the dealers who purchase directly from Rand Refinery… participated in illicit activities”.

Tricks of the trade

The bulk of the SARS investigation deals with the nebulous network of gold suppliers who allegedly supply Rappa and other gold exporters.

A 250-page letter of findings that SARS sent to Rappa on 11 December 2020 provides an overview of this network. According to the letter, Rappa bought gold worth R52-billion from 27 different direct suppliers in the period SARS was auditing – January 2019 to June 2020.

SARS identified the top 10 “level 1” direct suppliers and enumerated the astonishing methods virtually all of them allegedly used to introduce smelted Krugerrands and other illicit gold into the supply chain.

These methods include the creation of whole clusters of fake “level 2” companies that then “sell” supposed scrap to the level 1 supplier, which then sells to Rappa.

The SARS investigation found that one of these level 1 suppliers allegedly got its gold from eight smaller suppliers but, according to the revenue service, there is a veritable mountain of red flags around the legitimacy of these companies:

“Certain of the directors of the 8 (eight) level 2 suppliers denied any knowledge of the business, the business operations and their involvement therein,” SARS found.

The same directors “indicated to SARS that the company(s) were dormant, never traded and was to be deregistered”, said SARS.

However, these suppliers used the same bank accounts and provided SARS with the same address when they registered as VAT vendors, the revenue service claimed. Their addresses “were either residential address[es], could not be located by means of verification by SARS and/or were not valid addresses and/or premises which are utilised for business purposes”.

They were also paid for their “scrap” gold “by means of a third-party bank account and/or were remunerated in cash for their alleged taxable supplies”, and gave SARS “fictitious bank statements and invalid bank account particulars in order to register as a VAT vendor”.

A number of the companies accused by SARS of generating fake invoices and knowingly buying illicit gold nonetheless operate behind the cover of the London-based Responsible Jewellery Council.

It is a global certification organisation which, according to its online vision statement, wants to create “a responsible world-wide supply chain that promotes trust in the global jewellery and watch industry”.

The council did not respond to questions about the quality of its assurances by the time of publication.

Coining it

SARS’ R7-billion claim against Rappa stems from its findings involving three major suppliers: Northern Spark Refinery, JR Technical Services and Geba Precious Metals. These findings were set out in a “finalisation of audit letter” dated 29 March 2021.

The case of Northern Spark is particularly revealing of how the alleged illegal channelling of Krugerrands into the VAT fraud was massified.

According to SARS, Northern Spark was by far Rappa’s top supplier in the assessment period, selling Rappa R18-billion worth of gold. Underneath this “level 1” supplier there were supposedly a total of 48 “level 2” suppliers.

In April 2019, Northern Spark was raided by SARS. It has subsequently had its books extensively scrutinised, its suppliers investigated, and has been subjected to Section 47 tax enquiries, among other things.

The findings by Johan Klingenberg, an auditor at SARS’ Illicit Economy Unit, were included in the court papers. The first finding is that the company sold gold almost exclusively to Rappa.

Second, its supposed payments to its 48 level 2 suppliers were largely fictitious and, where suppliers were paid, they were not scrap suppliers, but companies whose “only trading activity is dealing in Krugerrand Gold Coins”.

“Documentary evidence was also obtained from a reputable third party that billions of rands of gold coins were physically delivered to Northern Spark’s business premises,” said Klingenberg.

“Certain of the ‘suppliers’ of Northern Spark, who were interviewed during the Section 47 interviews, indicated that they were not even aware of Northern Spark and that Northern Spark used the names of their entities. They also did not recognised (sic) the tax invoices issued in their entities names.”

Northern Spark allegedly instructed dealers in Krugerrands to open special bank accounts to receive payments, and at other times paid them through intermediary companies, the coin dealers testified.

“I was unable to obtain any evidence of second-hand gold jewellery purchased by Northern Spark during my investigation thus far,” said Klingenberg.

“The only commodity that therefore could have been sold to Rappa is in fact Krugerrand gold coins or gold-bearing bars consisting of smelted Krugerrands.”

The upshot is that SARS is disallowing the R2.4-billion input tax claimed by Rappa in relation to gold bought from Northern Spark.

Conviction

Northern Spark is of interest to authorities for another reason.

One of its founding directors, Andries Greyvenstein, was last year convicted for “illegal dealing and illegal possession of unwrought precious metals”, according to a media statement by the Hawks.

He and three other men “were arrested in Primrose during a clandestine operation after they were linked to several incidents of illegal procurement of unwrought gold”, read the media statement.

Greyvenstein is also a director of Gold Kid Trading, another significant supplier of gold to Rappa in previous years not covered by the SARS assessment.

Northern Spark’s attorneys told amaBhungane that it will not respond to questions because it has not seen SARS’ allegations independently.

The company’s lawyers told amaBhungane, “Kindly be advised that our clients are not in a position to respond to the various enquiries being made by yourself in the email under reply due to the fact that they are not in receipt of any of the documentation (Court papers) that relate to SARS and Rappa.

“Further there are allegations that are being made that are incorrect. We therefore need to ascertain if these incorrect allegations are contained in the said Court Papers.”

JR Technical

JR Technical, the second major supplier to Rappa targeted by SARS, allegedly faked supplies from individuals.

According to the finalisation of audit letter from March last year: “Members of the public, who according to the records of the level 2 supplier had supplied second-hand gold jewellery, denied having sold second-hand gold jewellery.”

JR Technical appears to have created a massively convoluted supply chain to throw off authorities.

According to SARS, some of the level 2 suppliers were fictitious and their “business addresses either could not be verified or were found to be the residential address of third parties”.

“Certain of these level 2 and 3 suppliers interchangeably supplied to each other in order to create confusion and to disguise the illicit nature of the transactions between the various levels of supply.

“Certain of the level 2 suppliers fraudulently made use of the VAT registration numbers of other suppliers in the supply chain.”

JR Technical did not respond to amaBhungane’s request for comment.

Geba

The third level 1 supplier SARS scrutinised for its assessment, Geba, is also accused of buying Krugerrands and smelting them.

SARS’ affidavits also reveal details of its investigation into Geba’s supply to Aesha, Rappa’s competitor. SARS’ Illicit Economy Unit (IEU) raided Geba’s offices in 2019.

“The SARS IEU auditors evaluated the data seized. They established that since April 2018, Unlock Capital (Pty) Ltd, seemingly sold vast quantities of Krugerrands to Geba.”

“The data seized from Geba proved that Geba issued recipient-generated tax invoices for Unlock Capital. These recipient-generated tax invoices reflected a taxable supply from Unlock Capital to Geba at a standard rate.

“The purpose of these fraudulent recipient-generated tax invoices is to disguise the fact that Krugerrands are introduced into the supply chain and to convert a zero-rated supply into a standard rated one,” according to SARS’ affidavit.

“In as far as your request for a response to questions and observations is concerned, our clients respectfully cannot adhere to the request, as the information relate to subject matter which is currently a dispute between Geba and SARS and as such remains subjudice and our clients have no comment in respect thereof at this stage.

“Geba and its directors deny any complicity in or knowledge of any illegal activity in the industry,” the company told us in response to questions.

SARS does not imply Unlock Capital is in on the scam.

The court documents show that SARS has made similar findings about Aesha as those made with regards to Rappa. There has, however, not been a court process to make more details public.

SARS is fastidious about taxpayer secrecy and the revenue service appears to have been even more concerned with witness protection in this investigation.

According to its court papers: “Witnesses in the tax inquiry testified that the secondary gold industry is a dangerous industry. Certain of the witnesses were scared and sought specific assurances that their evidence would not be disclosed.”

Rappa responds

Rappa has mounted a vociferous defence in court, arguing that SARS is targeting it in a scheme to make up for missing tax revenue targets and making serious allegations based on a flawed investigation that has not produced direct evidence.

“SARS is guilty of a material misdirection of law at the very least. More likely, however, this demonstrates the ulterior purpose, bad faith and irrationality in the raising of the Assessments. SARS has gone against Rappa because it perceives it to have deep pockets and because it has fabricated a basis to try and withhold refunds lawfully due to Rappa,” the company’s chief executive, Gary Bickerton, said in an affidavit.

According to Rappa, “most of the allegations and so-called findings… are based in their entirety on nothing more than unfounded conjecture, innuendo and suspicion and, in any event, are unclear and vague”.

The company has countered SARS’ assertion that the volume of gold it was buying was far too large to be ascribed to legitimate sources, by passing the buck to its suppliers.

“I specifically stated that I understood that the gold supplied to Rappa by its suppliers was a combination of second-hand jewellery and small-scale mining gold. This would then account for the massive numbers,” said Bickerton.

According to him, SARS has concocted an “after-the-fact and otherwise indefensible theory of justification that it is somehow constitutionally obliged to withhold VAT refunds where it believes a taxpayer such as Rappa ‘may possibly’ be implicated in what ‘might possibly’ amount to a scheme between myriad suppliers wholly unconnected with the taxpayer at issue”.

Rappa itself paid the so-called level 1 suppliers VAT and then legitimately claimed it back, he argued.

Treasury fights back

In October last year, National Treasury proposed new regulations to the VAT Act to try to quash what appears to be a vast gold VAT scam industry. The changes were to be implemented on 1 January.

The new mechanism being introduced is called a domestic reverse charge and is “aimed at removing the opportunity for fraudulent vendors to re-characterise gold and goods containing gold, make minimal VAT payments to SARS and extracting (sic) large amounts of VAT refunds from the fiscus”, according to the memorandum announcing the proposal.

The idea is to make the buyer of the gold liable for the VAT declarations of the seller, rather than the other way around. SARS hopes this would stamp out the invoice “factories”.

SARS did not respond to questions from amaBhungane. DM

The statement of the Responsible Jewellery Council can be found here.

The AmaBhungane Centre for Investigative Journalism is an independent non-profit organisation. We co-publish our investigations, which are free to access, to news sites like News24. For more, visit us on www.amaB.org

Comments

Scroll down to load comments...