An aerial view of China Evergrande Group's Riverside Palace development under construction in Taicang, Jiangsu province, China, on Friday, 24 September 2021. (Photo: Qilai Shen/Bloomberg)

An aerial view of China Evergrande Group's Riverside Palace development under construction in Taicang, Jiangsu province, China, on Friday, 24 September 2021. (Photo: Qilai Shen/Bloomberg)

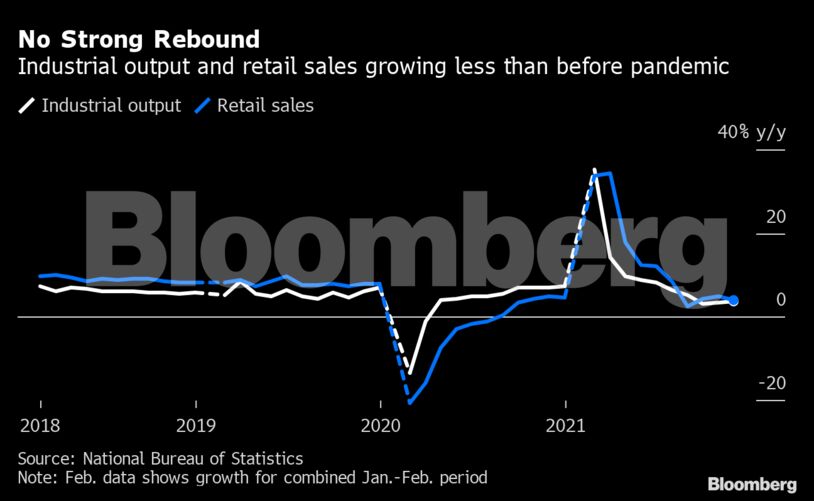

Industrial output rose 3.8% from a year earlier, quickening from 3.5% in October and above the 3.7% projected by economists. Retail sales growth weakened to 3.9%, missing economists’ forecasts of a 4.7% gain. Sales in the restaurant and catering sector dropped 2.7%, as people stayed home amid renewed virus outbreaks.

Read More: China Home Market Slump Deepens as Prices Fall for Third Month

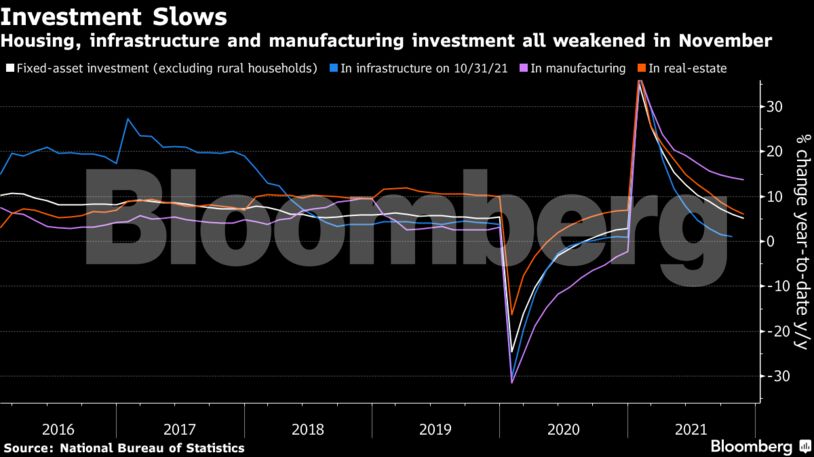

The data highlights the downward pressure on the economy from the real-estate sector and the scale of the challenge facing the Chinese government in stabilizing the world’s second-largest economy. While Beijing is expected to make more credit available and signaled some easing of controls on the property market to support “stability,” officials last week maintained the basic stance that “houses are for living in, not speculation.”

The economy’s slowdown has prompted Beijing to shift its focus to stabilizing growth, with the central bank easing monetary policy and the Communist Party ordering more fiscal spending in 2022.

Earlier on Wednesday the central bank kept the interest rate for one-year loans to banks unchanged and only rolled over about half of the maturing debts, withdrawing liquidity from the economy. However, a recently announced cut to the reserve requirement ratio for banks takes effect from Wednesday, which will increase the amount of money financial institutions have on hand to lend.

“The international environment is increasingly complex and grim and there are still many constraints on the domestic economic recovery,” the National Bureau of Statistics said in a statement. We must “combine the cross-cyclical and counter-cyclical macro policy adjustments so as to stabilize the overall macro economy.”

Infrastructure investment, another weak link in China’s slow recovery this year, rose at a slower pace of 0.5%. Local governments have stepped up efforts to borrow money and start new projects and Beijing has allowed authorities to start selling next year’s bonds from Jan. 1 to speed up spending.

What Bloomberg Economics Says...

China’s November activity data suggest the economy is still under strain, though the production side appears to be stabilizing. The pressure on the demand side was clear, with growth in both fixed asset investment and retail sales extending slowdowns. We expect fiscal and monetary policies to become more supportive in the months ahead.

David Qu and Eric Zhu

For the full report, click here

Consumption weakened despite support from still strong sales around the “Singles Day” shopping festival, which didn’t help offset the impact of the outbreaks of Covid-19 on consumption of services, restaurant and catering sales, and purchases at physical shops.

The surveyed jobless rate inched up to 5% while the average number of hours worked per week fell to 47.8 from the record 48.6 in October. The unemployment rate of those aged 16-24 rose slightly to 14.3% from 14.2%.

“Domestic consumption remains weak with retail sales disappointing,” said Raymond Yeung, chief economist for Greater China at Australia & New Zealand Banking Group Ltd. “The incremental increase in the jobless rate is concerning. The authorities should pledge more support and offer a stronger signal to the market.”

Comments

Scroll down to load comments...