SPONSORED CONTENT

SA remains resilient in its transition towards renewable energy

South Africa’s renewable journey, which began a decade ago through the Renewable Energy Independent Power Producer Procurement (REIPPP) programme, has experienced some stumbling blocks along the way. However, the country is still positioned favourably as one of the global leaders in renewable energy procurement.

This is evident in the more than R200bn private capital that has been invested in the programme thus far, some 20% of which is Foreign Direct Investment. Not a single plant has claimed against the government guarantee in place thus far. It is transparent and efficient, as shown through the number of investors (both local and foreign) that it has attracted since its inception.

Private sector capital is attracted by the stable (non-volatile cash flows) returns over 15-18 year periods that are largely not correlated to the listed markets. This offers an effective hedge against the volatility of the stock market without sacrificing risk-adjusted returns.

These real infrastructure assets also achieve positive broad-based social returns in the communities in which these projects are located while adding affordable and reliable electricity supply to the national grid, of which the SA economy is in dire need. A thriving economy is better for all of us. Finally, this programme has a positive environmental impact as electricity is generated with minimal carbon emissions.

Bid Window 5 of the REIPPP awarded

The latest highlight has come through the recent awarding of Bid Window 5 projects at the lowest weighted average cost of R0.47/KwH of all Bid Windows thus far. The more than 3x oversubscription was also encouraging.

While the Round 4 Bid Window PPA’s signature was long-delayed, the country’s energy blueprint was updated and finally gazetted in October 2019. Shortly after that, the requests for proposal for the 5th Bid Window (2 600 MW, split into 1 600 MW Wind and 1 000 MW Solar PV) was released in May 2021. Submissions were made to the IPP Office in August 2021, and the award announcement was made by 28 October 2021. As reported by the IPP Office, an overwhelming 102 bids (63 Solar PV and 39 Wind) were received, which signifies unwavering appetite for REIPPP.

Further, the IPP Office recently announced the expected timing of the rollout of the following few stages of the IRP2019.

The calendar year 2022 will be very busy as it will see Bids 5,6 and Storage awarded companies pursuing financial close. This generates a significant amount of activity in the local financial markets as each project tries to secure debt and equity funding to be deployed during construction. This is the stage when most institutional players really get involved. The same year will also see the release of RfP’s for Bid Window 7, Gas-to-Power and Coal, the latter of which remains in significant doubt as more financial institutions move away from funding it as a source of generating energy.

The Gas-to-Power bid window will be an interesting one to see unfolding. Firstly, gas is a fossil fuel even though its CO2 emissions are reportedly half of those from coal. Secondly, South Africa doesn’t have a significant supply of its own natural gas. This means it must be imported (at least, in the medium term), which exposes the country to long-term foreign exchange currency fluctuations, making it more expensive over the long term. On the other hand, we can’t be oblivious to the inclement nature of renewable energy while battery storage remains restrictively expensive. It’ll thus be interesting to see how the increasingly and necessarily environmentally active South African funding market and environmental lobby groups approach this rather challenging crossroads.

When the President announced that embedded generation facilities of up to 100MW would be exempt from NERSA’s licensing requirements, the market was pleasantly surprised as this cap was expected to be set at 50MW given the significant push-back by the DMRE Minister prior to this announcement. This set a significant milestone for the South African energy sector as it will unlock a reported 5,000MW of supply over the next five years when the country needs it the most. It will also inevitably alleviate a lot of pressure from Eskom’s shoulders, which has been struggling to reliably supply the country’s economy with energy while switching off some of its coal-fired power plants that have reached the end of their lifespans.

Another significant milestone was the announcement, as part of the increased cap, that generators will be allowed to wheel electricity through the transmission grid and not only the distribution grid, as had been the case previously. Practically, this means that a user can generate up to 100MW of their or their customers’ power needs in one location and have it consumed in a different location without going through NERSA’s lengthy and comprehensive licensing process. This is a significant shot in the arm for companies that can afford to build their power generation as this would reduce their reliance on Eskom and thus load shedding would have a lesser impact on their operations. The South African economy urgently needs a reliable supply of power. It is even better when it is both clean and more affordable.

Further, it is important that some of this additional 5 000MW (excess power) is fed back to the national grid. Although these grid-connected facilities would, unfortunately, need to comply with NERSA’s normal Distribution or Transmission Codes and follow the comprehensive registration process, it is still encouraging that NERSA will now have to complete their evaluation process and registration within 60 days versus the previous 120 days.

Integral to the conversation of Embedded Generation is transmission capacity. It is unlikely that the existing transmission capacity will be able to handle this additional variable load on top of additional REIPPP load as more plants come online. There are already suggestions that the transmission capacity in the Northern Cape, where a lot of the country’s renewable energy power is generated, is under pressure. This is clearly a vital cog in the embedded generation and wider distributed generation equations that requires urgent attention.

Emergency Risk Mitigation Procurement Programme (“RMPP”) held up in court

A low for the country has been the delay in the procurement process of the emergency Risk Mitigation Procurement Programme due to allegations of corruption and fraud. The programme aimed to add 2 000 MW of renewable energy to increase the base load of our power grid to alleviate/reduce the use by Eskom of Open-Cycle Gas Turbines (“OCGT’s”), which are fired through diesel and are thus expensive and highly pollutive.

However, the process was halted when DNG Energy accused Karpowership SA, who were awarded 1 220 MW of the allocated 2 000 MW, of fraud. This consolidated already growing momentum against this bidder as, before these accusations, environmental lobby groups had raised significant concerns about the impact these power ships would have on the environment and marine resources of the three ports in which these ships would be stationed. As a result, the Department of Forestry, Fisheries and the Environment refused to grant this bidder the requisite Environmental Impact and Assessment approvals, a crucial regulatory approval requirement to reach financial close.

In an unexpected procession of events, the National Energy Regulator of South Africa (“NERSA”) granted Karpowership SA energy generation licences amidst all the above.

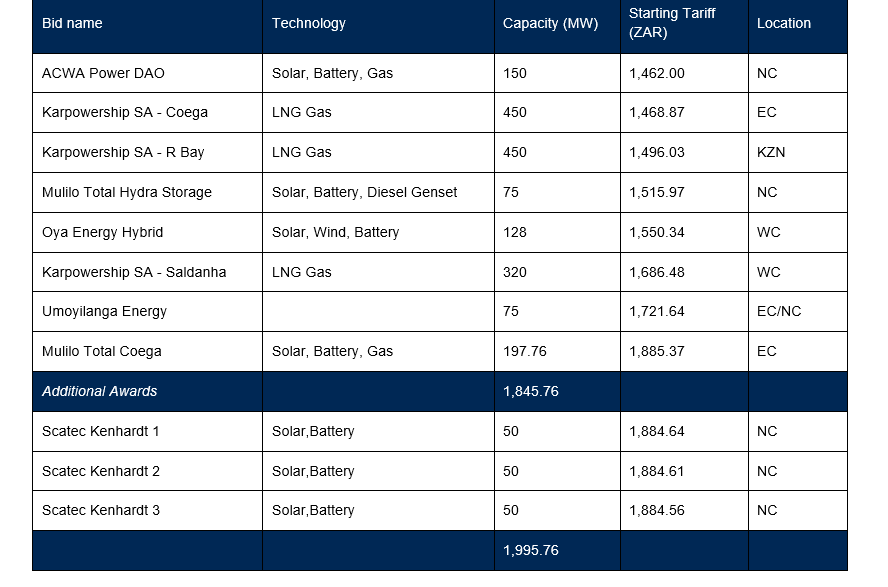

The 11 successful bidders were as follows:

Source: https://www.ipp-rm.co.za/

Source: https://www.ipp-rm.co.za/

As things stand, as the Karpowership SA/DNG Energy matter is in court, the financial close for this procurement programme has been moved out to 31 January 2022 (from 31 July 2021). While this means South Africa will remain exposed to severe load shedding for longer than anticipated, allegations of fraud and corruption must be treated with the seriousness they deserve and be cleared only in a court of law.

While the Independent Power Producers (IPP) Office has responded to these allegations as being “without merit” and “self-serving” and contended that “the applicant’s bid did not meet qualifying criteria”, the latter claim, which was substantiated through the evidence submitted as part of an affidavit by the IPP Office to court, a finding in favour of DNG Energy would cast significant doubt on the credibility of the whole programme.

The business case, from a unit cost point of view for the emergency programme, was evident. The weighted average tariff from the RMIPP was R1 598/MWh, which is 43% below the R2 778/MWh reported by Eskom in their 2021 AFS (OCGT). Additionally, while some of the projects are to incorporate some Liquified Petroleum Gas as a source of their baseload, a significant majority of this power was to be generated from Liquified Natural Gas, Solar PV, Wind and some battery used as storage. As a result, not only was this power expected to be cheaper than OCGT’s, but it was also expected to be less harmful to the environment.

Additionally, this programme was expected to inject more than R45bn private sector investment into the economy, local procurement of which would be 50%. It would also create 3 800 jobs during construction, and another reported 13 800 during the term of the Power Purchase Agreement.

Notwithstanding this setback in the timeline and other delays along the way, the demand seen from the last few Bid Windows of the REIPP and imminent expansion of Regulation 28 to allow pension funds a wider ability to participate in infrastructure debt investments suggest that significant demand for funding the rollout of REIPPP will continue. This will hold South Africa in good stead as it participates in the global transition towards clean energy. DM/BM

Author: Luzuko Nomjana – Portfolio Manager, Prescient Investment Management

Disclaimer

- Prescient Investment Management (Pty) Ltd is an authorised financial services provider (FSP 612).

- The value of investments may go up as well as down, and past performance is not necessarily a guide to future performance.

- Supervised representative.

- There are risks involved in buying or selling a financial product.

- This document is for information purposes only and does not constitute or form part of any offer to issue or sell or any solicitation of any offer to subscribe for or purchase any particular investments. Opinions expressed in this document may be changed without notice at any time after publication. We therefore disclaim any liability for any loss, liability, damage (whether direct or consequential) or expense of any nature whatsoever which may be suffered as a result of or which may be attributable directly or indirectly to the use of or reliance upon the information.

Comments - Please login in order to comment.