Traders work on the floor of the New York Stock Exchange on 20 March 2020. (Photo: EPA-EFE / JUSTIN LANE)

Traders work on the floor of the New York Stock Exchange on 20 March 2020. (Photo: EPA-EFE / JUSTIN LANE) With just six weeks to go before the end of the year, 2022 is within sight and the fortunes of the US stock market are again the subject of much debate after gaining 25% so far this year, doubling since 2019 and trebling since 1996.

These are big numbers and so it’s no wonder that investment managers are again contemplating what comes next – ruminations that have been spurred on by the US Federal Reserve’s decision to wind down asset purchases completely over the next six or so months, all going well.

Subsiding money market liquidity and, eventually, rising interest rates will likely weigh on equities if it undermines corporate profitability, thereby eroding the biggest contributing factor that has underpinned the marathon run up in US equities over the last decade and a half, and through the Covid-19 pandemic.

But if there’s one thing the last couple of years has shown us, it’s to expect the unexpected. Few would have thought that the US stock market would have been able to continue its now 14-year bull market during an unprecedented health crisis that has changed the world as we know it.

The question, however, is whether 2022 will see the bull market enter its 15th year, or whether the investor appetite will shift to other geographies, like Europe and Japan – where equities offer much better value and central banks are not so set on taking away the punchbowl for the foreseeable future – or emerging markets ex-China. Or will it be thematic investing or careful stock picking that will be winning the day for investors this time next year.

The US’s ongoing ascendancy has prompted repeated warnings that the cyclical upswing is near its end. Robeco, in its Expected Returns 2022-2026 update, says current valuations of risk assets “appear out of synch with the business cycle, and are more akin to where they should be late in the cycle”.

It sees these “torrid valuations”, especially for US equities, as suggestive of below-average returns and advises investors “to keep an eye on downside risk at a time when many investors have a fear-of-missing-out, buy-the-dip mentality”.

Morgan Stanley is another investment house that is not excited about the US equity market from a top-down point of view next year. “With financial conditions now tightening and earnings growth slowing,” it says, “the 12-month risk/reward for the broad indices looks unattractive at current prices.” It is putting its bets on stock-picking, which it sees as having the potential to deliver strong performance in an environment of continued strong nominal GDP growth.

So far, the surprisingly vigorous global economic recovery has enabled corporates to continue delighting investors with their quarterly earnings outperformances this year and, though the momentum of the global economy is waning, earnings are still expected to exceed expectations in a positive quarter for equities.

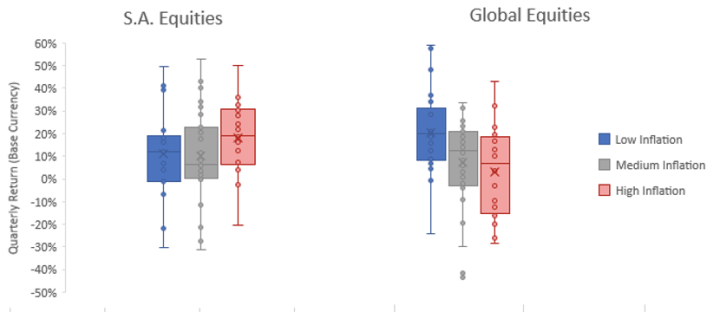

However, should inflation prove to be more entrenched than the developed market central banks believe it will be, US equities would face a significant headwind, with other countries, like South Africa, potentially benefiting instead.

Research conducted by Prescient Investment Management CIO Bastian Teichgraeber shows that high inflation in the US has historically been “generally good for SA equities, which act as a form of inflation hedge, and periods of heightened inflation after a crisis (especially with unprecedented stimulus) can be followed by low inflation due to a higher base effect in prices and the faucet of free money being turned off”.

He says that would result in a local equity market that offered pockets of value in a risk-on global environment, providing offshore investors looking for growth exposure to hedge inflation risk with an attractive opportunity.

As the graph below shows, SA equity returns have been higher than during medium and lower inflation periods, while global equities have delivered better returns in low inflation cycles.

Investec Asset Management global head of multi-asset growth, Phillip Saunders, and portfolio manager Iain Cunningham are managing potential cyclical shifts by focusing on five overarching structural themes it expects to drive financial markets. These are demographics, debt, technological disruption, China’s rise and climate change.

Whether its lower-than-expected growth, higher-than-expected inflation or any of these important structural themes, it’s important to bear in mind that the financial markets do move in cycles and, although those cyclical waves may last far longer than expected, they do shift at some point.

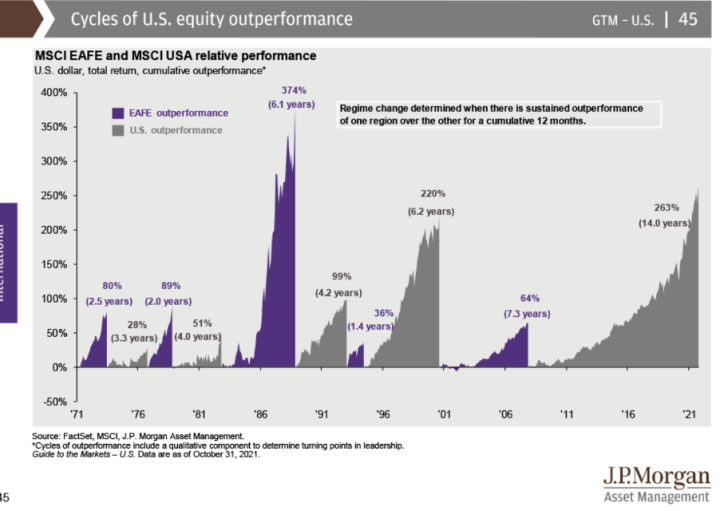

The JP Morgan graph below highlights how substantially the US has outperformed the other developed market equity markets, as encapsulated in the Europe, Australasia and Middle East grouping, EAFE. While the current cycle is by far the steepest and the longest period of outperformance for the US since 1996, it is unlikely to continue indefinitely.

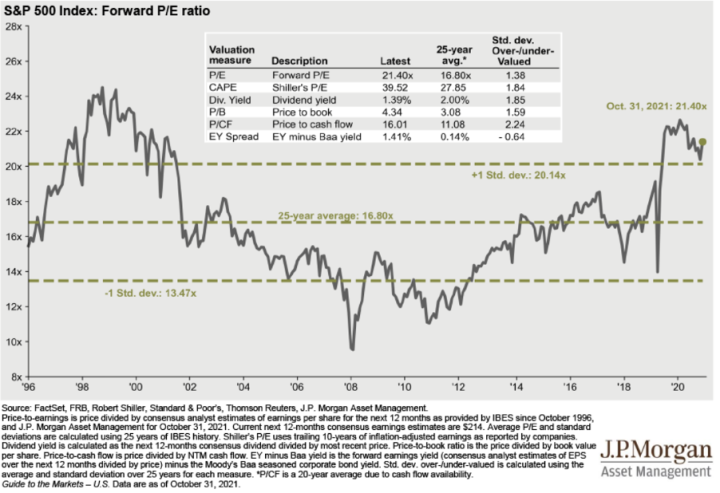

The US’s 263% outperformance of the EAFE equity universe has left it trading at hefty market valuations, with the S&P 500 price: earnings ratio 21.4 times compared with a 25-year average of 16.8 times. Across a range of other absolute measures, US equities look around 2% overvalued.

JP Morgan Asset Management points out that a relative perspective is a more useful gauge of whether the US equity market has outpriced itself or not – and if you measure the S&P 500 earnings yield relative to the Baa yield, the broad-based index looks cheap relative to fixed income assets.

However, the asset manager says the stars do seem to be aligned for international equities to take over because they offer cheaper equity valuations, cheaper currencies and the cyclical and structural themes could help boost their long-term returns.

This year has been an eventful one, but, unless it’s just me, it has also passed by far more quickly than 2020’s painfully slow coming-to-terms with a whole new world that is still in the making.

2022 will be here before we know it, with all its peculiarities and underlying seismic shifts, and the best that investors can do is focus on differentiating between the two if they want to make it through Covid Year Three ahead of the game. BM/DM

Comments

Scroll down to load comments...