Shipping containers on the dockside at the Port of Felixstowe Ltd. in Felixstowe, U.K., on Friday, Oct. 15, 2021. Handling more than a third of the U.K.s ocean freight, Felixstowe is battling a collision of incoming full containers and outgoing empties. Photographer: Chris Ratcliffe/Bloomberg

Shipping containers on the dockside at the Port of Felixstowe Ltd. in Felixstowe, U.K., on Friday, Oct. 15, 2021. Handling more than a third of the U.K.s ocean freight, Felixstowe is battling a collision of incoming full containers and outgoing empties. Photographer: Chris Ratcliffe/Bloomberg Their dilemma is that it’s hard to tell just how much of the inflation is being driven by a resurgence of demand as lockdowns end, and how much by supply strains caused by log-jammed ports and shortages of materials and workers.Raising interest rates now would temper the demand that lifted the world out of last year’s recession, but do little to ease the supply bottlenecks. If shortages then ease as trade returns to normal, policy could end up too tight and throttle the recovery.

But if the central banks hold back and the supply squeeze endures, that could entrench expectations of higher inflation –- prompting consumers and companies to push wages and prices up. In that scenario, central banks may later be forced to hit the brakes even harder.

“Trying to work out the difference between demand and supply-side drivers right now is incredibly difficult,” Stephen King, senior economic adviser to HSBC Holdings Plc, told Bloomberg Television. “Most central banks would probably admit at least in private that inflation is far higher than they had initially expected. You can see why some of them are biting their nails and becoming ever more nervous.”

‘Have to Act’

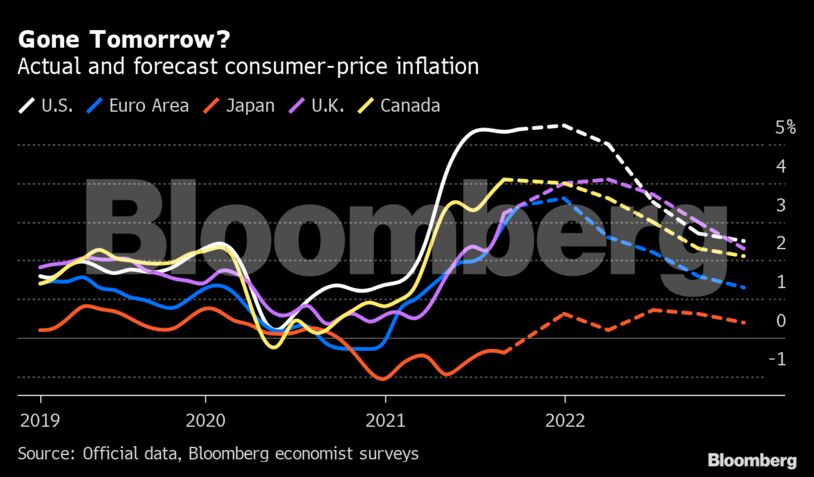

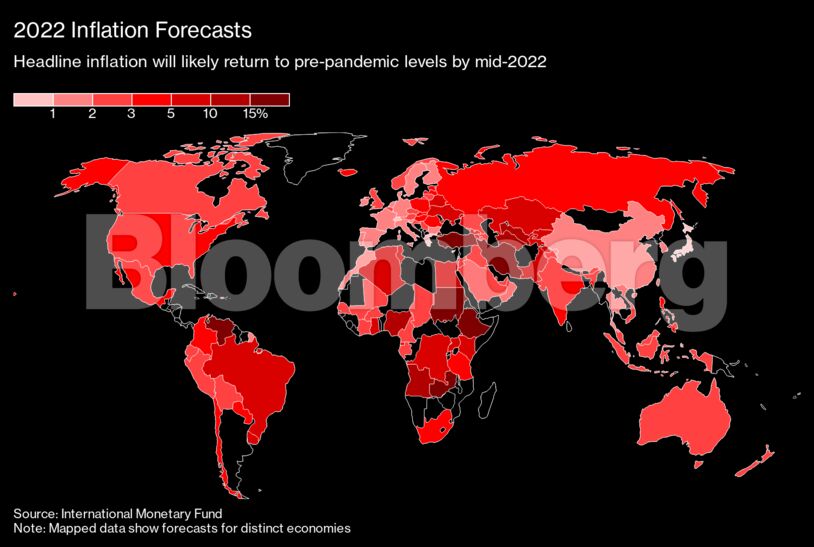

Worldwide, consumer prices have risen more than 4% over the past twelve months, with inflation outside of food and energy at its highest in the past decade, according to JPMorgan Chase & Co.

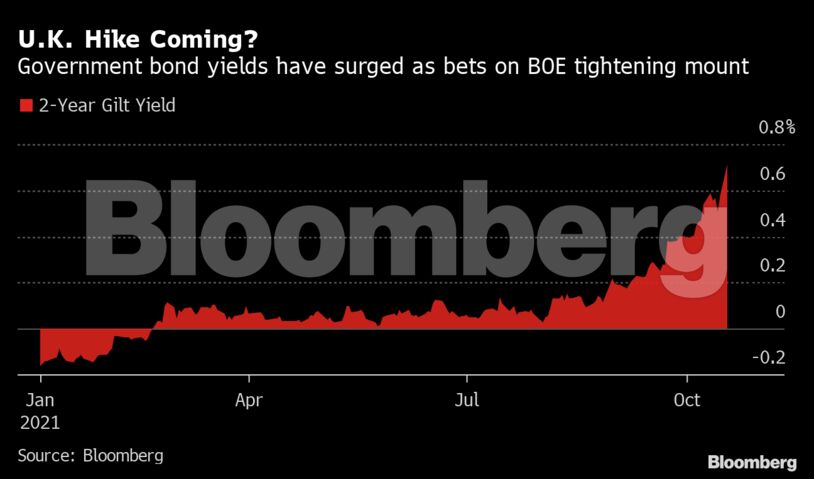

In the U.K., where inflation is on course to run at twice the Bank of England’s target this year, Governor Andrew Bailey warned on Sunday that the central bank will “have to act” -- even though he’s repeatedly highlighted the limits to what central banks can do.

Traders are betting the Bank of England will raise its key rate to 0.5% by the end of this year. That would place it alongside Norway and New Zealand among the small number of developed-economy central banks to have boosted borrowing costs during the pandemic.

The Federal Reserve isn’t about to join that club anytime soon, but it is poised to give the go-ahead next month to taper its $120-billion-per month asset purchase program. While Chair Jerome Powell has sought to delink that move from any hike in interest rates, other policy makers have pressed for an early end to the bond purchases so the Fed has leeway to boost rates if needed in the back half of next year.

‘Prick the Bubble’

The Fed is broadly sticking to its view that transitory factors are largely to blame for elevated inflation. But policy makers at the September meeting saw risks decidedly tilted to the upside. Investors are now pricing in two quarter-point rate increases next year.

Greg Peters, head of PGIM Fixed Income’s multi-sector and strategy, questioned how much the Fed could do to counter a rise in inflation stemming from a pandemic-driven disruption of supply chains.

“I’m not convinced that the Fed has any control around these issues,” he said in an Oct. 15 interview on Bloomberg Television. “Pundits are talking about the Fed needs to prick the bubble, they need to raise rates. To do what, exactly? To fix the supply-chain issues? Do you really want to crush the labor market?”

The European Central Bank seems set on continuing to support the recovery -– influenced in part by its own history of over-reacting to signs of inflation: The ECB raised rates in 2008 and 2011 before having to turn tail as the economy slowed. President Christine Lagarde said on Saturday that the current spike in inflation is unlikely to last.

That view is shared by others: People’s Bank of China Governor Yi Gang said on Sunday that producer-price inflation, which hit a quarter-century high last month, will start to wane at the end of this year. The International Monetary Fund said last week that inflation pressures will mostly unwind in advanced economies next year.

‘Buy Time’

Business leaders, though, are warning of longer-lasting price pressures.

On Monday, Royal Philips NV lowered its growth and earnings guidance after the shortage of semiconductors weighed on sales. Chief Executive Officer Frans van Houten expects staffing costs to remain high even as materials inflation subsides.

If the combination of strong demand and disrupted deliveries continues, it raises the risk that central banks will be forced into “an abrupt shift in policy sometime later,” said Neil Dutta, head of economics at Renaissance Macro Research.

One way for monetary policy makers to thread the needle would be by using hawkish rhetoric -– to keep a lid on inflation expectations -- while holding back on the actual interest-rate increases that would slow the recovery, according to John Briggs, global head of desk strategy at Natwest Markets.

It’s a strategy “to buy time to get to the other side,” he wrote, “and hope that the current supply-induced surges in both goods and energy prices eases by the time we see early 2022.”

Comments

Scroll down to load comments...