(Photo: Adobe Stock)

(Photo: Adobe Stock) In recent months, currency volatility and higher interest rates (or the threat of tighter monetary policy) have invariably been associated with bouts of risk-off sentiment (which, oddly, means investors are reducing their risk exposure) among global fund managers.

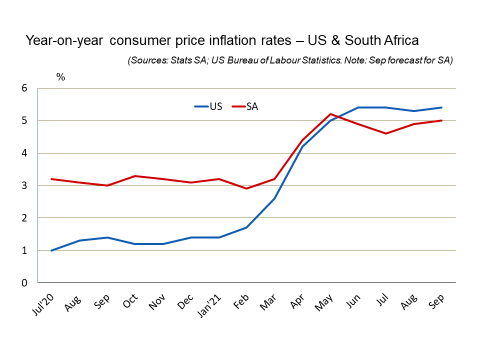

Higher inflation has been the root cause of more attractive bond yields, albeit only marginal in most of Europe, and the rise in the oil price suggests that price instability is becoming a key economic policy concern.

Ever since the economic malaise caused by the phenomenon of stagflation during the early 1970s, substantial scholarly research has been conducted on the relationship between inflation and GDP growth. Although consensus seems to exist over the negative correlation between high inflation and economic growth (with varying time lags), no clarity exists on what constitutes “high” inflation.

In a post-industrial economy, driven mainly by the services sectors and state-of-the-art technological innovation, an inflation rate of above 3% could be regarded as excessive, but in an emerging market that is still battling to establish a critical mass of infrastructure and integrated private sector supply chains, an inflation rate of between 5% and 7% could be regarded as a “threshold” rate.

The latter term has been the subject of research by Mishchenko (et.al), published in Banks and Bank Systems, vol.13. In attempting to find a compromise for monetary policy, specifically inflation targeting, the team of researchers from the Ukraine and the Russian Federation analysed the relationship between inflation and GDP growth, utilising IMF data on 158 countries.

Deflation is worse than inflation

Key to this ground-breaking research was the determination of the threshold of inflation (defined as the excess of which has a negative impact on economic growth). It was established that for the period 2010-2017, 6% inflation was the global threshold (or marginal) value of the inflation rate, beyond which the economic growth rate declined or slowed down.

Importantly for policymakers, the results also indicated that deflation constrains economic growth substantially less than high inflation.

A more recent article by Greg Petro, a contributor to Forbes, sheds some pragmatic light on the issue of inflation, by pointing out the negative effects on the retail sector (until recently) of a decade-long period of constrained price flexibility.

Higher inflation in the US is occurring at a time when the world’s largest economy is growing at a rapid pace, possibly even outpacing its biggest rival, China, during the second half of the year. Consumers in the US are also flush with cash and employers are hiring people at a rate of knots.

Although not all of these trends are present in South Africa, the country shares the universal post-pandemic phenomenon of pent-up demand, which will start to breathe new life into those industries that suffered the most from lockdown regulations, particularly hospitality and tourism.

Furthermore, the pandemic has thinned out the competition in the retail sector, which is the pulse of the global economy. According to a report by the United Nations Conference on Trade and Development, published in May, global e-commerce sales alone amounted to $26.7-trillion in 2019, representing more than 30% of global GDP.

Catalyst for spending sooner

Depending on the extent, duration and nature of the current upward trend for price levels, it should not constitute any serious threat to the post-pandemic economic recovery. Rising prices often serve to catalyse consumers into spending sooner rather than anticipating that goods will become cheaper.

Little doubt exists over the short- to medium-term nature of the current upward trend in price levels, as these have been mainly caused by supply-chain disruptions flowing from the uneven global pattern of lockdown restrictions. Progress with mass vaccinations and the general trend for an easing of restrictions will eventually also lead to an easing of constraints on manufacturing industries and international shipping.

Financial stocks usually count as a group that benefits from inflation, once it leads to a higher interest rate environment. The same holds for energy stocks, when higher inflation is caused, in part, by higher oil and gas prices.

For now, the message to central banks in emerging markets should be clear – do not overreact by raising interest rates when demand is still in the process of recovering. DM/BM

Dr Roelof Botha is Economic Adviser to the Optimum Investment Group.