The offices of Standard & Poor's in New York, New York.(Photo: EPA / JUSTIN LANE)

The offices of Standard & Poor's in New York, New York.(Photo: EPA / JUSTIN LANE) Remember the old adage: If the US sneezes, the rest of us catch a cold. Well, as we head into September, the US stock market is looking in fine form, notching up several eye-watering milestones over the past month.

Last week the US Federal Reserve set the stage for the S&P 500 to achieve another record high – its 50th all-time high in 2021 and putting it 20% ahead for the year to date. In August, stock markets in the UK and Europe also rallied a couple of percentage points, with the FTSE 100 Index up 1.7% for the month and the Euro Stoxx 50 2.5% higher.

It’s only China that looks anaemic after the government’s shock regulatory stance, putting the brakes on big tech and online education players’ share prices – and business futures. For the year, the CSI 300 Index is off almost 8%, but it did manage to eke out a 0.4% gain for the month.

In South Africa, the JSE All Share Index felt the fallout from China – declining 2.8% for the month – given the significant weight Naspers and Prosus hold in the index and the significant share price declines incurred by Tencent. Over 12 months, however, the local stock exchange is still 25% higher, and there is optimism in the domestic investment community that the JSE still has further to go.

But, with various risks bubbling under globally and the bull market now in its 13th year, the debate rages on about how long equity market investors’ good fortunes can last. This year, there has been a good reason for the rally in equity markets. UBS AG analyst Mark Haefele points out that S&P 50 earnings results have been much better than expected for the fifth quarter in a row, and are now 30% higher than pre-pandemic levels.

The latest second-quarter earnings season was particularly strong, with more than 85% of US companies beating earnings and sales estimates. Haefele points out that aggregate corporate profits are up nearly 90% on a year ago, which was higher than his original estimate of 80% corporate profit growth and “much stronger than the typical recovery from a recession”. Also, S&P 500 profit margins are at a multidecade high of almost 14%.

Against this backdrop, he is confident that the S&P 500 Index could reach 5,000 by the end of the year – 500 points and just over 10% from 4,500.

“Going forward, we believe cost pressures for businesses should subside as supply begins to catch up,” says Haefele. “Finally, consumers’ balance sheets are at their strongest in decades due to the significant build-up in household savings over the past year, while on the production side, retailers will continue to restock to keep up with demand.”

Events that could undermine this optimistic outlook would be the Covid-19 situation getting even worse – with the third wave protracted or a fourth wave threatening – a sharp rally in US Treasuries which have held at yields of below 1.4% throughout August, and a sharp deterioration in the economic environment, which is already looking vulnerable.

We’re nowhere near out of the woods yet regarding Covid-19. Daily deaths in the US have now exceeded 1,000 a day for the first time since March, and infections have consistently increased for nine weeks. South Africa is still battling to come out of the other side of its third wave, and this week’s news that local scientists had potentially found another Covid-19 variant is a keen reminder that we need to expect the unexpected.

The messaging coming out of the Jackson Hole symposium was also significant for bond investors. Federal Reserve chair Jerome Powell did an excellent job of convincing financial markets that, although tapering was likely to happen this year and not early next year, it would be done gradually and cautiously. He emphasised that the preconditions for a rate hike would also be stringent.

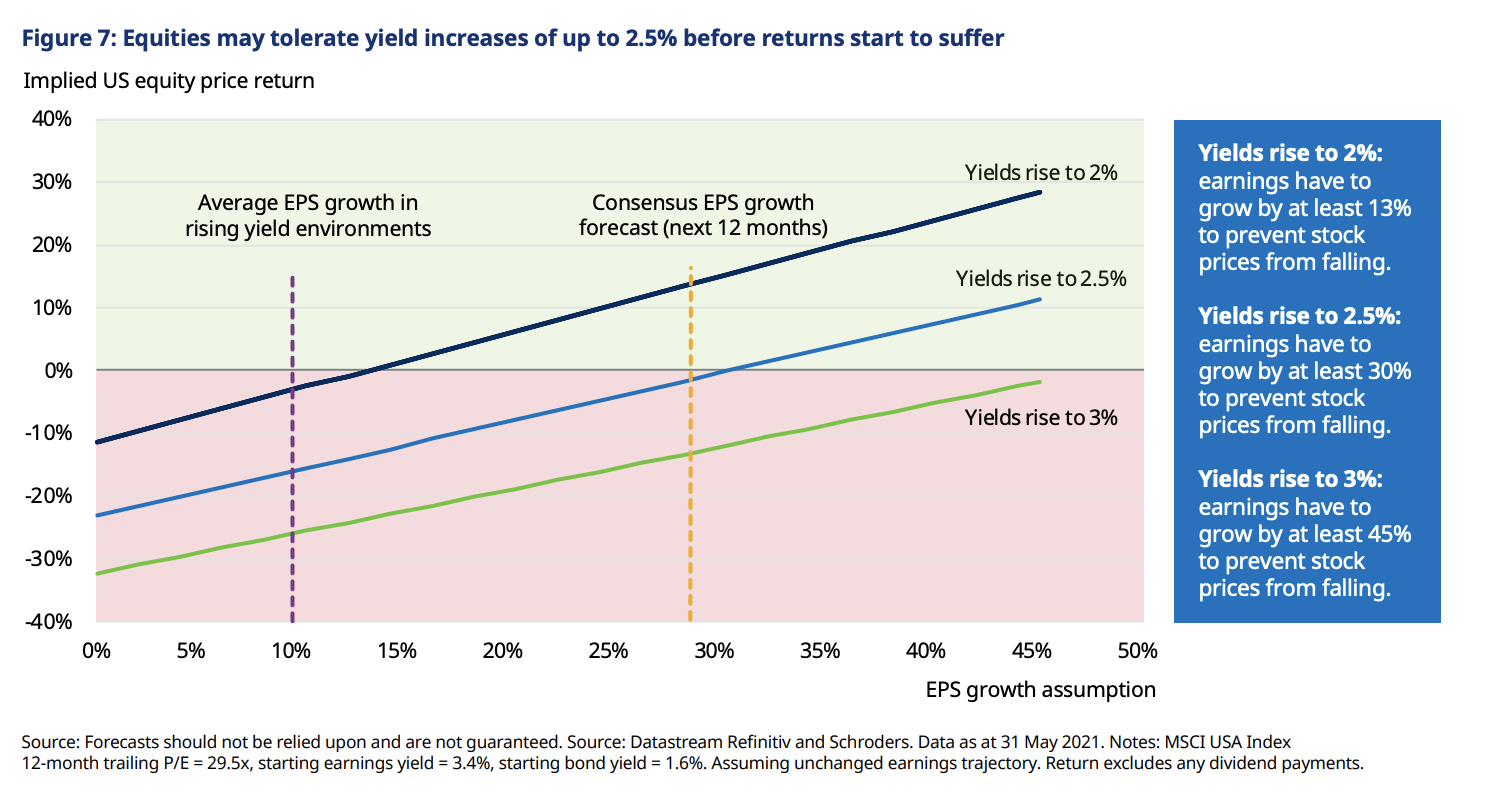

Thus, current conditions suggest that the US 10-year Treasury yield, a benchmark for interest rates globally, is unlikely to move sharply higher off its recent lows. This year, Schroders did some interesting analysis on the likely impact of a change in bond yields on the equity market. Though a few months ago, it still provides a good perspective on what investors can expect should circumstances change as we navigate a potentially precarious period during September, when more evidence of the Delta variant’s impact on the global economy will become available.

Schroders Strategist Sean Markowicz’s conclusion, based on his analysis of previous periods during which interest rates increased, is that rising bond yields alone are necessarily bad for equity returns – as long as yield increases are gradual and don't exceed 2.5% and the increase is roughly proportional to earnings growth.

“Most of the time, markets can absorb the impact because earnings growth is strong enough and/or valuations expand. None of this is particularly surprising as rising rate cycles often coincide with improving growth prospects and inflation, which are supportive for stock prices,” said Markowicz.

The graph below highlights three scenarios in which US 10-year Treasury yields rise to 2%, 2.5% and 3%, and the earnings growth that would be required to prevent stock prices from falling.

For now, Goldman Sachs and JP Morgan, two of the biggest US bond market participants, no longer anticipate yields increasing to 2% by the end of the year, and have decreased their projected year-end 10-year yield to 1.6% and 1.75%, respectively, so that may give the equity market a reprieve.

A more severe global economic slowdown would also pose a threat to buoyant equity markets. Citigroup’s Economic Surprise Index continues to surprise on the downside. The latest PMIs are rolling over, with China’s services sector falling below 50, which means it is contracting, yet equity investors have taken this in their stride. But it does make stock markets vulnerable to any further bad news.

Citigroup believes that “a return to the usual trend” could see a 10% to 15% selloff in the S&P 500, or the index moving sideways for the next six months.

When looking at the performance of equities since their sharpest and shortest bear market selloff in history in March last year at the onset of the pandemic, it’s hard to believe that Covid-19 has had any impact on company earnings or share prices.

Hopefully, this is not a case of “if it sounds too good to be true, it probably is” – another investment adage that has stood the test of time, for good reason. BM/DM