Federal Reserve Board Chairman Jerome Powell. (Photo: EPA-EFE / Drew Angerer / POOL)

Federal Reserve Board Chairman Jerome Powell. (Photo: EPA-EFE / Drew Angerer / POOL)

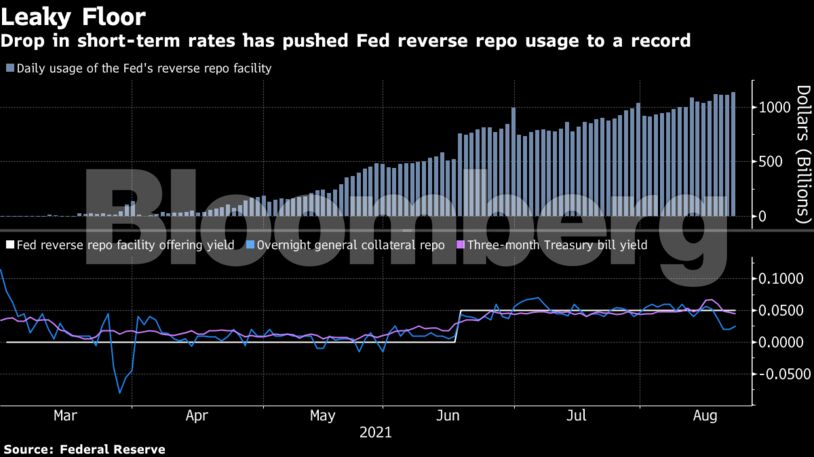

Demand for the so-called RRP facility has surged as a flood of dollars threatens to overwhelm funding markets. That’s in part a result of the central bank’s long-standing asset purchases and drawdowns of the Treasury’s cash account, which is pushing reserves into the system. As a result, liquidity has been swelling, especially as the Treasury cuts supply to create more borrowing room under the debt ceiling.

The pressure pushing down overnight rates toward zero is proving a major headache for money-market funds. It hampers their ability to invest profitably, and can lead to further disruptions as they begin to waive fees to avoid passing on negative rates to shareholders. A number of firms including Vanguard Group shut down prime money-market funds last year after struggling to cover operating costs in the low-interest-rate environment.

Not Panacea

“The Fed’s technical adjustment earlier this year is not a panacea for the money markets,” JPMorgan Securities strategists Teresa Ho and Alex Roever wrote in a note. “Supply and demand technicals remain an overarching driver of rates, and with the supply and demand gap now having grown to $1.35 trillion, it’s not surprising that the Fed’s ON RRP is providing only a soft floor for money market rates.”

The strategists predict the distortion will linger even after the Fed begins reducing asset purchases from the current level of $120 billion per month. Even if the central bank were to complete tapering by August 2022, as JPMorgan expects, there may still be an additional $850 billion to $1 trillion of additional liquidity injected into the financial system.

While Treasury bill supply is expected to rebound once the debt-ceiling limit is resolved, it’s still unclear when that will happen. Bills maturing at the end of October and through November are yielding more than the securities surrounding those dates.

--With assistance from Stephen Spratt.