OP-ED

Policy implications for SA: Upward phase of the super-cycle still intact

Ever since the swift and pronounced global economic recovery from the pandemic, the likelihood of a commodity price super-cycle has been trending in economic circles.

Much of the debate has been rather confusing, especially with regard to the absence of academic rigour and supporting data. A super-cycle in commodity prices does not equate to rising prices alone, but consists of an upswing and a downswing phase, with a peak year representing the turning point.

Formally, a super-cycle is defined as long-term price movements for a wide range of commodities that are above the trend. According to the authoritative research and econometric modelling by Erten & Ocampo (2012), the full cycles of upswings and downswings last between 20 and 70 years.

It is not surprising, therefore, that the theory of commodity price super-cycles has met with some scepticism amongst leading economists, including Nobel laureate Gary Becker, who stated in 1988: “If long cycles of the Kondratieff or Kuznets type exist, we will need another 200 years of data to determine whether they do exist or are just a statistical figment of an overactive imagination.”

Relevance to commodity exporters

Studying the nature of super-cycles in commodity prices nevertheless remains relevant to policymakers in developing countries that are highly dependent on commodity exports as a source of foreign exchange and economic value added.

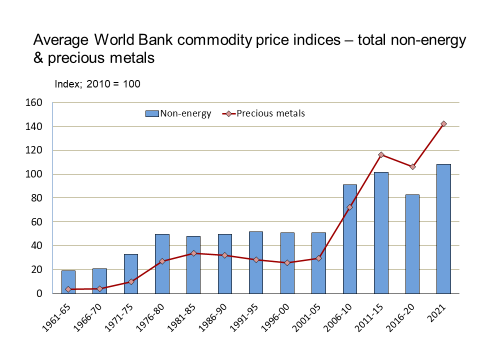

Erten & Ocampo’s research has only identified four super-cycles since the end of the 19th century, with the latest one still in progress (at the time of publication of their study in 2012). History will prove them correct in predicting the ongoing nature of the 4th post-19th century super-cycle, but they did not foresee the eclipse of their peak year conclusion, namely 2010.

The World Bank’s non-energy commodity price index continued increasing up to 2011, which would have been very close to the mark, but after declining by almost 34% over the next five years, it started to pick up again, remaining stable until 2020, but still 30% below the record high of 2011. Then the global economic recovery gained momentum and commodity prices leapt to new record levels.

Whether or not the current commodity super-cycle remains in its new-found upward phase has important policy implications for South Africa, especially against the background of several years of lethargic growth, continued socio-political unrest and the dire need for reducing unemployment. The latter is a direct outflow of State Capture and widespread corruption and incompetence in the public sector at large – a legacy of the governance decay engineered by former president Jacob Zuma and his cohorts.

A significant increase in capital formation is a prerequisite for an acceleration of economic growth, and the current boom in metal and mineral prices, especially precious metals, could pave the way for substantial new investment in mining. It may even allow the mining sector to relive its past glory as a major contributor to employment and value added in the South African economy.

Conditions for an upward phase

However, decisions on capital investment are taken with due consideration not only of current commodity prices, but also expected future price trends. Furthermore, capital formation in mining can take between 10 and 20 years before starting to generate revenues. It is illuminating, therefore, to delve into the circumstances that have to be present for an upswing phase of the super-cycle to occur or to continue.

Empirical research has identified the presence of a surge in demand for a variety of raw materials during the industrialisation (and inevitable urbanisation) of a major economy or group of economies. This occurred in the early 20th century in the United States and in Europe and Japan during the post-World War 2 period.

The current super-cycle is largely being driven by the rapid and sustained expansion of the Chinese economy, which is likely to be augmented by the inevitable further development and growth of the economy of India (the world’s second-most populous country)

The current upward phase in commodity prices may face the odd lapse but is fuelled by a number of impressive drivers, including:

- Resurgent economies, but with large differences in key measures of fundamental economic stability, especially in the area of public finance. This uneven pattern of geographical recovery implies a steady but erratic process of recovery from an unprecedented low base.

- As pent-up demand is coming to the fore, supply-chain disruptions caused by lockdown regulations are likely to continue for several years, especially in developing countries, where deficiencies in logistical capacity have been exacerbated by fiscal constraints

- Supply-side constraints can operate in tandem with demand-side factors in prolonging commodity price upswings, especially when there is insufficient investment in new capacity in commodity-exporting countries – leading to increasing costs

- With the United States now having rejoined the global drive towards a green economy, the demand for certain metals and minerals will experience the type of high and structural increases that have accompanied previous super-cycles. This effect will be enhanced by the growing importance of environmental, social, and governance (ESG) criteria that socially conscious investors use to screen potential investments in companies. According to the most recent report from the Forum for Sustainable and Responsible Investment, assets held by investors that were chosen according to ESG criteria jumped from $8.1-trillion in 2018 to $11.6-trillion in 2020 – an increase of 43% in the space of only two years.

Record trade surplus

The strong upward phase in commodity prices represents the main reason for South Africa’s trade surplus notching up new records on a regular basis. The cumulative trade surplus for the first five months of 2021 amounted to more than R161-billion, which goes a long way to explaining the rebound of the rand exchange rate since the Covid-induced low of April 2020.

Hopefully, the commodity price upswing will last long enough for South Africa to retain capital market stability. This will aid the quest for reining in rising public debt and allow fiscal resources to be spent more productively, especially on the expansion of infrastructure. DM/BM

Comments - Please login in order to comment.