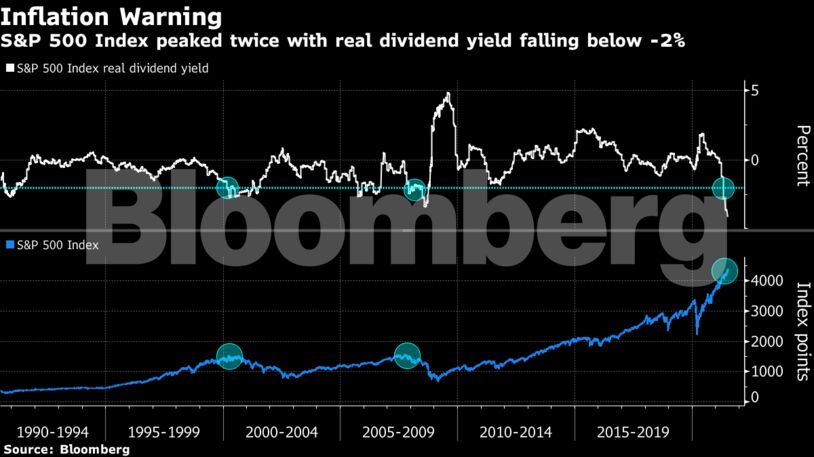

Investors had earlier delighted in the prospect of a strong worldwide economic rebound fueled by easy money and vaccine rollouts. But the combination of price pressures and soaring infection rates raises the risk that growth could fall short of rosy forecasts. And with global equities teetering at all-time highs, there’s no room for error.

In the minds of some investors, the moves represented a pullback in overextended areas of the market, like cyclicals. Others pointed to the usual volatility that comes with earnings season and thin summer trading.

“While macro conditions remain overall supportive for equities, valuations, seasonal trends and positioning leave the room for price corrections and volatility spikes” like Monday’s, said Antonio Cavarero, head of investments at Generali Insurance Asset Management.

Other strategists urged clients to use the weakness as a time to buy.

“I am firmly in the buy the dip camp,” said Marija Veitmane, senior multi-asset strategist at State Street Global Markets. “Stocks had a very strong first half supported by the earnings recovery and we expect corporate earnings to remain strong.”

For Ruchir Sharma, head of emerging markets and chief global strategist at Morgan Stanley Investment Management, there’s still a worry that growth expectations are too high. China’s regulatory crackdown on its technology sector and U.S. consumers saving more than they spend are among the key risks, he said.

Global Growth Boom May Disappoint, Morgan Stanley’s Sharma Warns

Stalling vaccination rates, especially in the U.S., are also dragging down market sentiment, wrote Deutsche Bank AG’s George Saravelos. At the same time, rising prices have caused consumer demand to stall in many economies.

“This is part of broader post-Covid scarring; it is also part of bottleneck demand destruction,” he wrote. “This is the opposite of what one would expect if the environment was genuinely inflationary. It shows the global economy has a very low speed limit.”

I lived and worked amongst these people for years. They are like the wildebeest in the veldt. They suddenly start running the opposite direction and one asks another, “Why did you change course?” It replies, “I think I saw a lion lying in the grass.” By the time that message gets to 10 others, it has become “There is a pride of lions lions lying in wait for us.”

I’m not saying we should disregard all investment advice but I always take their macro assessments with a HUGE grain of salt. 🙂