Wang Xing, chairman, chief executive officer and co-founder of Meituan Dianping, poses for a photograph ahead of a Bloomberg Television interview following the company's listing ceremony at the Hong Kong Stock Exchange in Hong Kong, China, on Thursday, Sept. 20, 2018. Meituan Dianping, the Chinese food delivery and neighborhood services giant, rose as much as 7.3 percent on its first day of trading after raising $4.2 billion in an initial public offering.

Wang Xing, chairman, chief executive officer and co-founder of Meituan Dianping, poses for a photograph ahead of a Bloomberg Television interview following the company's listing ceremony at the Hong Kong Stock Exchange in Hong Kong, China, on Thursday, Sept. 20, 2018. Meituan Dianping, the Chinese food delivery and neighborhood services giant, rose as much as 7.3 percent on its first day of trading after raising $4.2 billion in an initial public offering. But this wasn’t the flamboyant Chinese billionaire who disappeared from public view eight months ago. It was Mark Zuckerberg, bobbing up and down on a hydrofoil surfboard, clutching an American flag and exuding all the confidence of a man worth $130 billion.

The contrast between the social media mogul’s July 4th Instagram video and the day’s big event in China could hardly have been starker. Regulators in Beijing had just hours earlier banned Didi Global Inc.’s ride-hailing service from app stores, delivering their latest hammer blow to an entrepreneurial elite that once seemed destined to challenge Zuckerberg and his U.S. peers at the top of the world’s wealth rankings.

The age of unfettered gains for China’s ultra-rich now appears to be coming to an abrupt end.

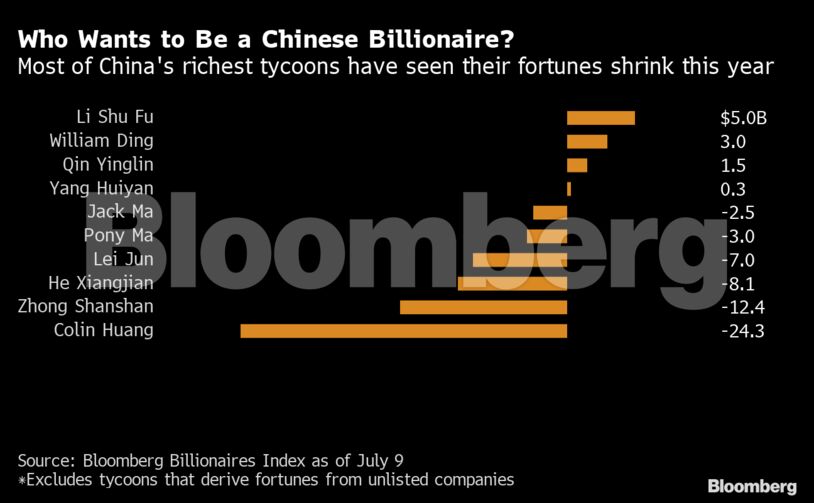

Even as the world’s 10 wealthiest people added $209 billion to their net worth in the first half of 2021, China’s richest tycoons in the Bloomberg Billionaires Index saw their combined fortunes shrink by $16 billion. Shares of their flagship companies sank by an average 13% during the period, the first time in at least six years they’ve recorded declines when the broader Chinese equity market was rising. Didi’s stock has plunged 14% since its June 30 debut on the New York Stock Exchange, slashing the wealth of the company’s co-founders by almost $800 million.

Behind the losses is a crackdown that has only intensified since November, when Ma’s Ant Group Co. was forced to pull its blockbuster initial public offering at the last minute. Policy makers are tightening regulations on some of the most important facets of Asia’s largest economy, from financial services to internet platforms and the data that underpins most big businesses in modern China. In the latest salvo, regulators unveiled new draft rules on Saturday that would require nearly all domestic companies to undergo a cybersecurity review before listing in a foreign country.

Beijing’s motivations for the crackdown are varied. They include concerns about anticompetitive behavior in the tech industry, risks to financial stability from lightly regulated lending platforms and the rapid proliferation of sensitive personal information in the hands of large corporations.

But another undercurrent running through many of the government’s latest initiatives is a not-so-secret desire to rein in the power of China’s tycoons, some of whom have amassed an enormous amount of influence over the $14 trillion economy. As one government official familiar with the leadership’s thinking described it, Beijing wants to prevent its billionaires from becoming a force as strong as the family-run chaebol that dominate South Korea’s economy and many aspects of its politics.

Adding to Beijing’s resolve is the Chinese public’s growing concern over rising inequality. At a major speech on his economic plans in October, President Xi Jinping acknowledged that the country’s development was “unbalanced” and said “common prosperity” should be the ultimate goal.

The upshot is a new era for the country’s billionaires and the investors who back them. Gone are the days when tycoons like Ma could confidently bend the rules to supercharge their companies’ growth and challenge entrenched interests like state-owned banks. Outsized public personas -- long seen as an asset for tech-company founders -- now look like a liability. The new playbook for China’s ultra-rich calls for more deference to the Communist Party, more charitable donations and more focus on the wellbeing of rank-and-file employees, even if it hurts the bottom line.

“Some of the tech companies became larger than life,” said Allan Zeman, a property tycoon who gave up his Canadian passport to become a naturalized citizen of China in 2008. One big lesson from the crackdown: “Don’t get bigger than the government,” Zeman said, shortly after attending the Communist Party’s 100th anniversary celebration in Beijing on July 1.

Didi notwithstanding, the message appears to be getting through. Ma, who criticized Chinese financial regulators in his last public speech before Ant’s IPO was abruptly suspended, has since resurfaced only a handful of times in carefully choreographed appearances.

Colin Huang, whose e-commerce giant Pinduoduo Inc. has come under scrutiny for its relentless working schedules, has given up his roles as chairman and CEO and donated shares worth billions of dollars. ByteDance Ltd. founder Zhang Yiming said in May he would step down as CEO and spend more time on educational charity.

Wang Xing, the chairman of food-delivery giant Meituan, has mostly steered clear of the public spotlight since he posted a 1,100-year-old poem in May that some regarded as an implicit criticism of the government. Wang, who later issued a clarification saying the post had been targeted at the shortsightedness of his own industry, was advised by Beijing officials to keep a low profile, according to people with knowledge of the matter.

The new environment will “fundamentally change” China’s tech sector, partly because investors will become more wary of funding entrepreneurs who could end up on a collision course with Beijing, said Eric Schiffer, CEO of Patriarch Organization, a Los Angeles-based private equity firm.

U.S. President Joe Biden has also taken aim at the billionaire class, calling for increased taxes on the rich and signing an executive order on Friday that aims to weaken dominance of America’s biggest companies. The move echoed an ongoing antitrust campaign in China that has ensnared giants including Alibaba Group Holding Ltd. and arch-rival Tencent Holdings Ltd.

Read more: China Watchdog Rejects Tencent-Led Game Streaming Deal

One key difference is that Chinese authorities, unrestrained by Western-style checks and balances, can act more forcefully than their U.S. counterparts, said Angela Zhang, director of the Centre for Chinese Law at the University of Hong Kong and author of “Chinese Antitrust Exceptionalism.” Zuckerberg’s hydrofoil joyride came just a few days after a judge dismissed two monopoly lawsuits against Facebook Inc. that had been filed by the U.S. government and a coalition of states.

“In the case of China, the pendulum swings very quickly,” Zhang said.

Beijing has a variety of tools for reining in billionaires, including detention in the most extreme cases. An internal disciplinary process for party members, known as shuanggui, has been used for some tycoons in the past. Investigations by antitrust, cybersecurity and other regulators are more common ways to influence the behavior of tech giants. The government also uses “soft” methods including state-media campaigns, Zhang said.

In the days after regulators halted Ant’s IPO, Xi visited a museum in the eastern city of Nantong that was created by Zhang Jian, a 19th century capitalist. The Chinese president described Zhang as a patriotic nation builder and philanthropist. Rather than disrupt the financial system with unregulated loans, he built factories and hundreds of schools.

“When you see a virtuous person, follow his example,” Xi was quoted as saying by Chinese media, calling on private entrepreneurs to “strengthen their feelings for the country and assume social responsibilities.”

Read more: China’s Fading ‘First-In First-Out’ Rebound Sends Global Warning

While China’s crackdown has been most visible in the tech industry, the country’s property billionaires have also come under increased pressure in recent years. Authorities have steadily restricted the industry’s access to funding in an attempt to rein in home prices and reduce systemic risks to the financial system. China Evergrande Group Chairman Hui Ka Yan has been among the biggest casualties of the campaign this year, losing $6.7 billion, or nearly 30%, of his fortune as Evergrande’s stock tumbled on concerns the company faces a liquidity crunch.

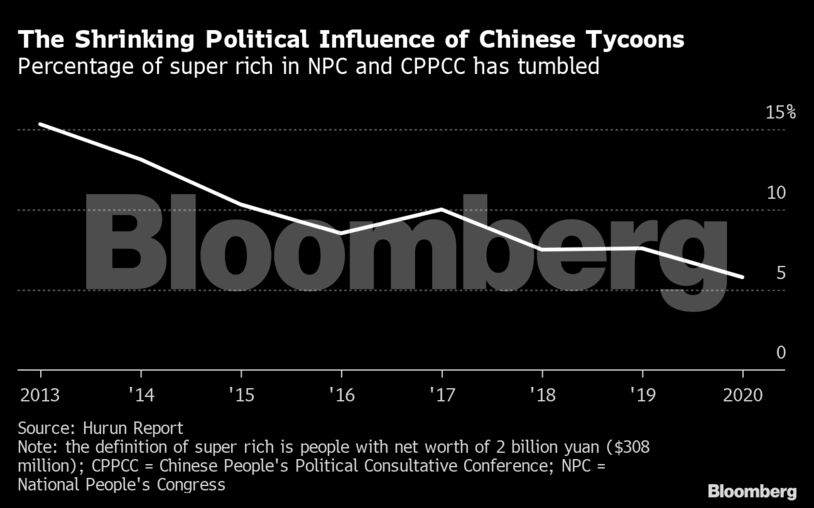

A more subtle sign of billionaires’ waning influence can be seen in their shrinking share of political appointments. Data from the Hurun Report, which produces wealth rankings, shows that rich entrepreneurs accounted for 5.8% of delegates in the Chinese People’s Political Consultative Conference and the National People’s Congress, the lowest in at least eight years and down from 15.3% in 2013.

“There is an evolution in the thinking of which type of people should be within the mix,” said Rupert Hoogewerf, the Hurun Report’s chairman. “It’s becoming much harder for entrepreneurs.”

The big question is whether all of this will be good for China in the long run. One risk is that the onslaught of regulatory probes and rule changes undermines investor confidence, HKU’s Zhang said. That could make it less likely that the entrepreneurs behind the next potential Alibaba or Tencent get the funding they need to make their ideas a reality. Global venture capital firms will likely think twice about investing in Chinese companies if Beijing prevents them from listing overseas, a crucial exit route for early international backers.

Yet some of Beijing’s new policies may foster competition in the oligopolistic tech industry, clearing the way for a new class of billionaires to rise. Stricter regulations on fintech firms will help reduce systemic risks, even if they slow down innovation. China’s crackdown on Ant won praise last month from Berkshire Hathaway Inc. Vice Chairman Charlie Munger, who said in an interview with CNBC that the “Communists did the right thing” by letting Ma know he couldn’t “wade into banking...and just do whatever he pleased.”

Either way, China’s entrepreneurs will have little choice but to embrace the “new normal,” said Chen Long, a partner at consulting firm Plenum. “The good old days of savage growth are gone.”