(Photo: Unsplash / Chris Leboutilier)

(Photo: Unsplash / Chris Leboutilier)

Greg Muttitt is Senior Policy Adviser, Energy Supply, at the IISD. Shruti Sharma is an Associate and Energy Specialist in the IISD's Energy programme and the India Project Coordinator. Mostafa Mostafa is an IISD policy adviser. Kjell Kühne is research co-author, founder and director of Leave it in the Ground. Alex Doukas is Senior Consultant for the KR Foundation. Ivetta Gerasimchuk directs the sustainable energy activities of the IISD's Energy Programme and its Global Subsidies Initiative. Joachim Roth is a policy analyst with the IISD's Energy team.

The International Institute for Sustainable Development (IISD) report, Step Off the Gas: International public finance, natural gas and clean alternatives in the Global South examines the choices countries face in how to develop their energy systems while meeting socioeconomic needs.

The report finds that:

- Gas projects in low- and middle-income countries are receiving more international public finance than any other energy source: four times as much as wind or solar.

- This investment risks driving a new dash for gas that locks countries into a high-carbon pathway, imperilling their economic future and the global climate.

- Gas is not needed, as renewable-based alternatives for most of its uses are either already cheaper or are expected to be within a few years.

- Renewable electricity is an increasingly cost-competitive and effective means of providing clean cooking, helped by improvements in the efficiency of electric stoves and devices.

- Countries in the Global South need greater international support to finance clean energy projects, including to help integrate renewables into often weak or unstable electricity grids.

The Covid-19 pandemic has exposed how rapid global change can affect countries in deeply inequitable ways and the importance of building resilient and socially just economies. As economic resources remain constrained in the coming years, it will be vital that scarce public funds are devoted to building back better.

This report recommends that international public finance should no longer support fossil fuels, focusing instead on creating the enabling conditions for countries to build energy systems based on renewable energy.

International public finance is driving a new dash for gas

The greatest impacts of climate change will be felt in the Global South, especially by the poorest people (Intergovernmental Panel on Climate Change [IPCC], 2014; Special Rapporteur Extreme Poverty and Human Rights, 2019).

Southern countries differ widely in their circumstances and needs. What they have in common is that they have done less to date to cause climate change and have access to fewer resources to mitigate it compared to the wealthier countries of the Global North. Often, significant portions of their populations are energy-poor, while energy demand is growing fast.

The gas industry increasingly sees its future growth potential in the Global South. Gas advocates are calling on governments to pave the way for gas expansion, especially in Asia and Africa. New liquefied natural gas (LNG) exporters, such as the United States and Australia, are seeking new markets while gas companies look for new resources to extract and export.

Efforts to expand gas are being underpinned by international public finance from multilateral development banks (MDBs) and from G20 bilateral financial institutions such as bilateral development banks and export credit agencies. While accounting for only a small portion of total energy finance, international public finance plays a disproportionate role: it both unlocks private finance by reducing project risk and gives signals that influence wider investment trends. According to the International Energy Agency (IEA, 2020a, p. 276), public funding and policy support for gas in these economies in the coming years will be a key factor in determining whether global gas demand increases into the 2030s.

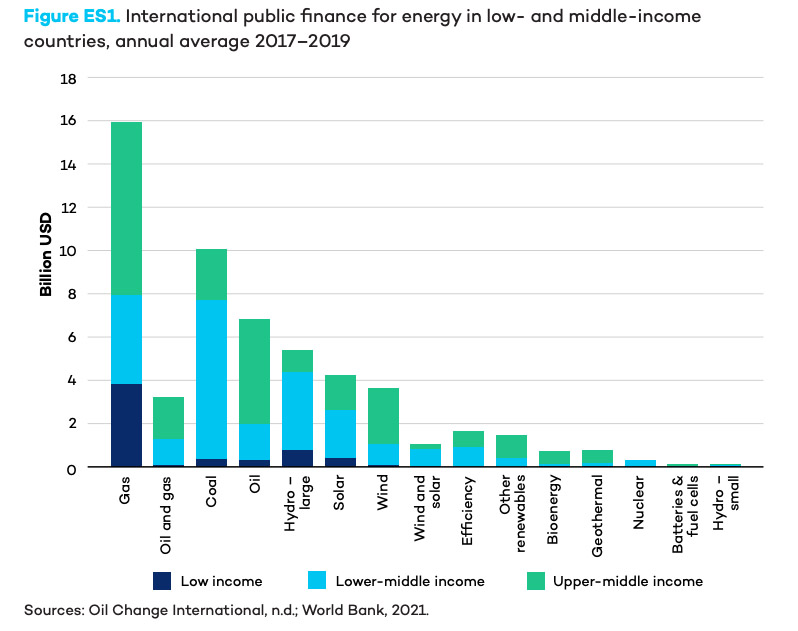

Using Oil Change International’s Shift the Subsidies database, the report finds that in low and middle-income countries:

- Gas projects received an average of nearly $16-billion in international public finance per year from 2017 to 2019. This is more than any other source of energy and four times as much as wind or solar.

- The majority of this finance is going to power generation, where gas is least needed, and high-emission LNG infrastructure that risks locking large sections of the economy into gas.

- International public finance invested in all fossil fuels was more than twice as high as for clean energy.

- Initial data on the MDBs’ direct project finance shows that they continue to prioritise gas during the Covid-19 pandemic: gas accounted for more than 75% of MDBs’ support for fossil fuels in 2020.

Gas investments are environmentally damaging and economically risky

Gas advocates have long argued that gas can serve as a “bridge fuel” until renewable energy can be developed at a larger scale. Today, this idea is obsolete for three reasons. First, the climate crisis is now urgent: remaining atmospheric space is so limited that there is no room for any additional fossil fuels. Second, since wind, solar, and energy storage and other supporting technologies have fallen rapidly in cost and are deployable at a large scale, there is no longer a need for a bridge. Third, recent findings on the extent of methane leakage from gas infrastructure undermine claims of environmental benefits over other fossil fuels.

Furthermore, now that renewables are competitive, additional gas tends to displace renewable energy as well as coal (McJeon et al., 2014; Zhang et al., 2015). Gas starts to look more like a wall than a bridge, impeding rather than enabling the energy transition.

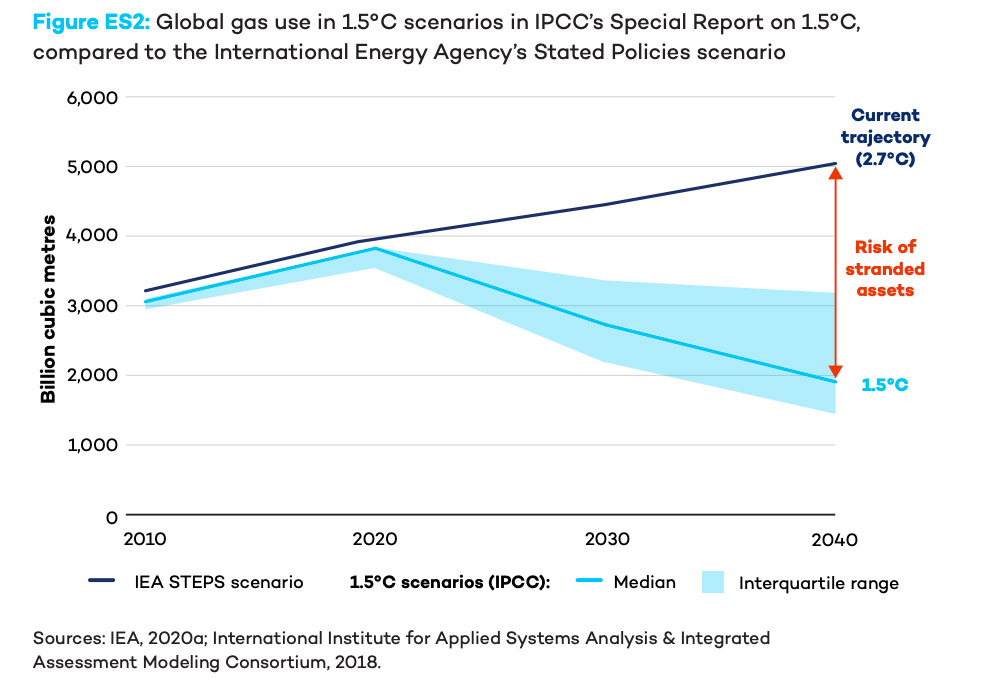

In the median 1.5°C scenario used in the IPCC Special Report on 1.5°C (IPCC, 2018; International Institute for Applied Systems Analysis & Integrated Assessment Modeling Consortium, 2018), global gas use is halved from 2020 to 2040. Most scenarios see power generation almost completely decarbonised by mid-century, even in a 2°C world.

As climate limits drive an accelerating global energy transition, the falling costs of renewable energy will squeeze the whole gas supply chain, creating financial risks for investments in both producing and consuming facilities. Meanwhile, long-lived infrastructure can lock an economy into a carbon-intensive development path that is difficult to leave (Friedrichs & Inderwildi, 2013). Countries are in danger of being left behind in the global energy transition, saddled with stranded assets, more expensive energy, dependence on imports, and trading disadvantages.

Some countries plan to increase their domestic gas production either to generate export revenue or to reduce dependence on imports. However, as global energy markets change, these look like increasingly risky investments. Evidence of the resource curse suggests racing to stay ahead of the energy transition is likely to lead to disappointment: without taking time to build institutions and domestic supply chains, much of the revenues and jobs will flow overseas. Ironically, domestic gas production can increase dependency on imports by creating public expectations and political pressure for gas subsidies, which then encourages consumption to grow faster than production (Gomes, 2020). Rapid gas development in Mozambique is already showing signs of a “presource curse” (Frynas & Buur, 2020) through deepening public debt, increasing militarisation, and exacerbation of militia violence.

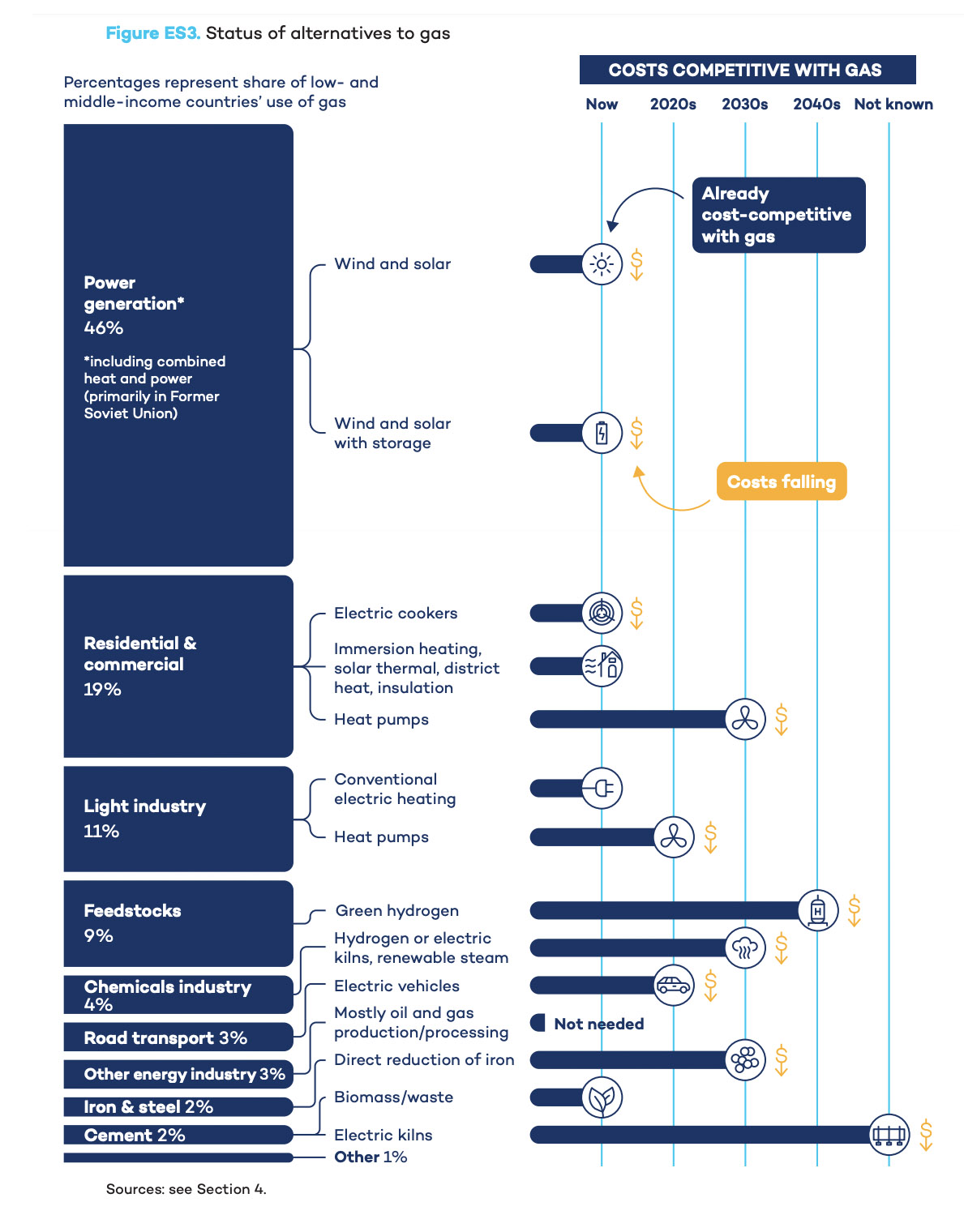

Gas is not needed, as renewable-based alternatives are available and affordable for most uses

The Global South has the world’s largest wind and solar resources, and harnessing them creates opportunities to develop without depending on volatile international markets.

For the majority of present uses of gas, alternative technologies are either already cheaper than gas or are expected to become cheaper within a few years (Figure ES2). Often, the lowest-cost decisions are those that reduce energy requirements, such as efficiency standards, insulation, or urban planning. For the minority of gas uses where clean alternatives are not yet available or affordable—such as in heavy industry—rapid technological development is underway, with commercialisation expected by the early 2030s.

In most countries for which data are available, wind and solar now generate power at a lower cost than gas (BloombergNEF, 2020a). Battery costs are also falling rapidly, and in some countries, the combined cost of wind or solar with batteries is less than that of flexible “peaker” gas plants (BloombergNEF 2020a, 2020b). Tropical countries have a strong advantage, as greater sunlight consistency through the year makes solar energy strongly pairable with batteries, creating less need for longer-term storage. At the low penetration levels currently seen in most of the Global South, grid management needs for integrating renewables are modest and low-cost; well-tested approaches will be adequate until penetration rises, by which time storage costs will have fallen further.

Gas is a poor solution to the energy access problem. Of the 800 million people worldwide who are lacking electricity, 85% live in rural areas (IEA et al., 2020, p. 4), where distributed renewable energy is, in most cases, better able to provide electrification at a lower cost. To provide clean cooking fuels for the three billion people relying on dangerous solid biomass, costly plans to expand natural gas connections to residential consumers will face competition from electric solutions due to both reductions in the cost of renewables and improvements in the efficiency of electric stoves and cooking devices (Couture & Jacobs, 2019).

As sustainable alternatives become cheaper and easier to implement, and since they are more suited to meeting development needs, there is little rationale for international public finance institutions to continue supporting gas at scale in the Global South.

International public finance can enable the global south to overcome energy transition challenges

International public finance can play a vital role in overcoming three challenges Southern countries often face in building renewable-based energy systems. The first obstacle is obtaining finance when private investors perceive high risks and low returns. The second is accessing and benefiting from technology whose patents and manufacturing capacity are held abroad. The third is integrating renewable energy in grids that suffer from blackouts due to poorly maintained infrastructure, ineffective grid management, and financially weak utilities.

The report argues that, if well targeted, public support can unlock the clean energy future instead of supporting large incumbent industries.

The report recommends that international public finance institutions:

- End all direct and indirect support to gas exploration and production, as well as to new gas power plants and other long-lived gas infrastructure, such as pipelines and LNG terminals.

- Reorient and substantially scale up clean energy finance to enable countries to transition from (or leapfrog) gas by:

- Investing in the technologies and institutions that facilitate grid integration of variable renewable energy;

- Enabling technology transfer to contribute to local technological and industrial development;

- De-risking private investments in renewable energy while providing concessional finance where need is greatest;

- Supporting achievement of universal access to clean electricity and cooking in line with Sustainable Development Goal 7, including off-grid renewable energy in regions where access is lowest; and

- Ensuring the free, prior, and informed consent of impacted communities for all clean energy projects.

- Prioritise support to the poorest countries that face the greatest challenges in developing renewable energy systems, notably least-developed countries and small island states.

- Provide support to help enable a just transition for affected workers and communities.

- The report recommends that governments in the Global South:

- Plan energy and climate development strategies that are based primarily on renewable energy, energy efficiency, and electrification, and aligned with the Paris Agreement goals.

- Avoid building new infrastructure that locks their economies into gas or other fossil fuels.

- Build experience and skills in managing variable renewables in the grid and in deploying non-fossil technologies in industry, buildings, and transport.

- Stop issuing new licences for oil and gas exploration and extraction.

- Enact policies that enable a just transition for workers and communities currently dependent on gas production and consumption.

Argentina, Egypt and India: Exemplifying the challenges for emerging economies

The report examines the future of gas in three case study countries based on interviews with government officials, stakeholders, and researchers, and supplemented by desk research. We focus on these three large, emerging economies because it is such countries that will have the largest impact on global gas demand.

Today, Argentina relies heavily on gas consumption and remains trapped between high subsidies and debt. When Argentina was previously a gas exporter, plentiful supplies created public pressure for subsidies, which in turn led to a rapid increase in gas consumption that now exceeds dwindling production (Gomes, 2020). While renewable energy is cheaper over its full life cycle (Secretaría de Energía, 2019, p.19), the higher upfront capital costs have been prohibitive, especially with unfavourable borrowing terms. The government has instead pursued unconventional gas extraction, providing production subsidies to overcome the resource’s unfavourable economics.

Egypt has ambitious plans to increase renewable energy’s share of generation, but its development has been put on hold in order to prioritise gas. The country aims to become a gas trading hub, pooling its own production with that of neighbouring countries for export to Europe. This strategy, however, depends on European gas demand, which may not be sustained as climate pressures increase. Support for domestic gas consumption is driven by fears of dependence on oil imports. Egypt incentivises the conversion of vehicles to gas fuelling but is now also seeking to expand electric vehicle manufacturing and use, creating a danger of redundancy with parallel charging and gas-fuelling infrastructure.

India is a fast-growing importer of gas. Given the high costs of imported gas, more than half of installed gas power capacity sits idle, and renewables are now the main competitor with coal in power generation (Ministry of Power, 2021). Meanwhile, new import and distribution infrastructure is now being built, with the threat of a second phase of redundancy as energy economics transform. The largest use of gas is in the industrial sector (IEA, 2020b), largely dominated by fertiliser production, which has little alternative feedstock until green hydrogen becomes competitive or the use of fertiliser decreases due to land use or other practices; meanwhile, India remains vulnerable to gas import costs. Like Egypt, the government is encouraging increased use of both compressed natural gas and electric vehicles, building out two parallel sets of infrastructure for fuelling and charging. DM