SCORPIO

South African insurance industry rocked by Insure Group ‘premiums misappropriation’ scandal

When the fraud at VBS Mutual Bank was uncovered in 2018, the bank’s implosion pulled away the blanket covering another black hole, of R1.7bn – this time in the insurance sector.

It’s a scandal that has largely remained out of the headlines until now, even though insurance giants Santam, Hollard, Old Mutual and Guardrisk have, between them, lost R944-million as a result. But behind closed doors, it has rocked the industry, rattled the regulators, and led to the dramatis personae – Charl Cilliers and Diane Burns, directors of Insure Group Managers – being debarred as financial service providers, based on their lack of honesty and integrity.

Both Cilliers and Burns deny all culpability for what happened. But the facts paint a different picture. The story here is that Insure Group Managers, an intermediary which collected insurance premiums from customers, which it was meant to pay over to the insurance companies, instead secretly invested that cash in its own very illiquid, high-risk and ultimately loss-making assets.

These “investments” included a mining rehabilitation plant in Gauteng, a deepwater port in Mozambique, a property portfolio in KwaZulu-Natal, and a stake in an asset management company. It also used the cash to build its own business, by financing brokers and intermediaries.

But not only didn’t Insure tell the insurers, to whom it was meant to pay the premiums, that it was using their money for a different purpose – its conduct was also unlawful. The regulator, the Financial Sector Conduct Authority (FSCA), describes it as “tantamount to a misappropriation of the premiums collected”. Industry body Financial Intermediaries Association of Southern Africa (FIA) labels this conduct “illegal”.

Cilliers, as CEO of Insure, is a chartered accountant – an industry that can hardly afford any more bad publicity – while Burns was the “director for strategy and compliance”.

Their goal, according to the FSCA, was to make a “secret profit” without the consent or knowledge of about 45 other insurance companies, who stood to lose out.

In September 2018, after Insure’s shoddy investment decisions led to a cash crunch, it was placed under “voluntary curatorship”, with Pieter Bezuidenhout appointed as the curator.

While Bezuidenhout’s investigation so far indicates no evidence that there was any intention to steal the money, the indication is that Insure’s directors wanted to make larger profits for personal gain by secretly “misappropriating” the premiums before paying them over.

The FSCA says this practice of “rolling over” premiums – in which a particular month’s premiums are used to pay the previous month’s debt – is unlawful. This is because it’s only sustainable if the money coming in exceeds the amount that has to flow out to your clients; it leaves no cushion, should anything go wrong.

But the fact that Insure was using these premiums for its “investments” is even more dubious since, as one company insider told Scorpio, these were “hare-brained investments”.

In particular, one environmental lawyer described Insure’s investment in the Mozambique port as “ill-conceived”, since the development has stalled repeatedly, and hinged on the tenuous cooperation between Botswana, Zimbabwe, Mozambique and China.

Brandon Topham, the head of enforcement at the FSCA, and Lizelle van der Merwe, CEO of FIA, say Insure’s scheme amounted to “illegal” conduct, involved a “misappropriation” of the premium money, and created a possible “systemic risk” to the wider industry.

Cilliers and Burns were at all times the “directing minds”, says the regulator.

As a result, the FSCA has debarred both Cilliers and Burns for five years – a decision they both intend to appeal in July.

“It is evident,” the FSCA argues, “that Cilliers and Burns were no longer fit and proper with regard to the personal character qualities of honesty and integrity. The debarment of both individuals was an appropriate administrative sanction.”

Bezuidenhout, in turn, said that “a number of irregularities occurred in the management of the business of [Insure]. These irregularities are being investigated and reported on to the FSCA.”

Quite how serious these “irregularities” were aren’t yet known to Scorpio, while the extent to which Cilliers and Burns personally benefited from the scheme also remains unclear.

Meanwhile, Insure’s operations have been sold as a going concern, as Bezuidenhout tries to unwind the assets to pay off the debt.

However, in a 33-minute interview with Scorpio, Burns strongly denied claims of illegality, misappropriation, or that she and Cilliers were the “directing minds” of the company. Neither she nor Cilliers did anything wrong, she insists.

Instead, she sketched an entirely different picture – one in which she is a “whistle-blower” who has been “targeted by the FSCA and insurers”. As a result, she says, her debarment is “ludicrous”.

Burns claimed she will become a “whistle-blower who will make protected disclosures about the worst financial scam in South Africa’s history in terms of the Protected Disclosures Act”.

However, when asked to elaborate on what this “scam” entails, she and her lawyer Harvey Nossel declined. Nor did she provide any evidence to back up her allegations.

Nonetheless, she says that being on the receiving end of this grand conspiracy has affected her “mental health” – though again, she declines to explain why, or how.

Cilliers, through the same lawyer, declined to comment – citing his pending appeal against the FSCA’s finding.

So who lost out? And will there be accountability?

While the law ensures the policyholders won’t carry the can for the R1.5-billion in premiums which Insure couldn’t repay, about 45 insurers were forced to take it on the chin.

Ironically, VBS Mutual Bank, which was looted to the tune of R2-billion by its own managers, auditors and local politicians, some of whom now face criminal charges, also lost out in this mess.

Insure held a R250-million credit facility at the bank, of which it had used R180-million. But when VBS ran out of money, Insure wasn’t able to use the other R70-million of its credit line – hastening the rug being pulled out from under it. It means that today VBS has a claim against Insure for about R180-million.

But the big insurance giants also felt Insure’s collapse in their pocket.

Santam and Hollard each took a knock of about R300-million; Guardrisk lost about R200-million while Old Mutual lost R144-million, according to their financial records.

Thanks to their weighty capital buffers, all these insurers told Scorpio that the loss wouldn’t impact their solvency, liquidity, or ability to pay out claims. However, some acknowledged they may never get the money back.

Hollard said this scandal was significant for “the greater insurance industry”. Hollard, along with Santam and Old Mutual, said it is closely working with the curator to claw back their money. Santam added that it was critical “to ensure accountability”.

Guardrisk says the money was “effectively misappropriated from the insurers”, and says proven criminal activity must lead to criminal charges and legal action.

Behind closed doors, however, insurers are demanding accountability for this scandal, eight sources have confirmed.

Privately, the insurers blame the FSCA for poor oversight and lax controls, which they say allowed this to happen in the first place.

In response, the FSCA argues that the insurers themselves are obliged to conduct proper due diligence and oversight over their service providers.

Both parties have a point, says a director of one of the large insurers who lost money.

“What we actually need is accountability,” this well-placed source told Scorpio. “Someone needs to end up paying a huge fine and maybe get criminally charged. Getting debarred is not enough. We need accountability to serve as a deterrent to safeguard the industry.”

While the larger insurers are weathering this storm, this scandal has proven too much for one company.

The small black-owned Lion of Africa, which was owed R28-million by Insure, had to close its doors in late 2018, shortly after Insure went into curatorship.

Fred Robertson, chair of the board of Lion of Africa, said Insure’s inability to pay the premiums owed to it wasn’t the only factor prompting the decision, but it “was certainly a contributing factor”. At that stage, Lion of Africa couldn’t afford another setback.

Some insurers owed money by Insure chose to convert a portion of this debt to equity – a total of R300-million – hoping the curator would claw back enough money for them to recover something.

At this stage, it’s not clear they ever will.

The scheme: The way it worked

As a dominant player in the premium collection industry, Insure Group Managers collected and paid over about R19-billion in premiums per year to the underwriters, according to its financial statements.

But while things may have reached a head in recent years, the earliest “misappropriation” of the premium money at Insure seems to go back as far as 2012, one insider suggests. If so, this underscores claims that the regulator may have been asleep at the wheel.

Several industry and company sources told Scorpio that Insure had a perpetual and “desperately” growing need for cash leading right up to 2018.

And it may all have remained hidden had Insure’s investments made lots of profit. Only, they didn’t.

And so Insure began using the future month’s premium money to pay its historical debt.

Then when VBS collapsed in March 2018, it meant Insure couldn’t call on its extra credit with the bank. Six months later, in September that year, Insure’s years-long secret bubbled to the surface, when it couldn’t pay its debt.

It had no option but to file for curatorship – and the rot soon emerged.

‘Rolling’: How did Insure work the scheme?

The contracts between Insure and the insurers stipulate that Insure had to “strictly” pay over the premiums it collected, in accordance with section 45 of the Short-term Insurance Act, says the FSCA’s Topham.

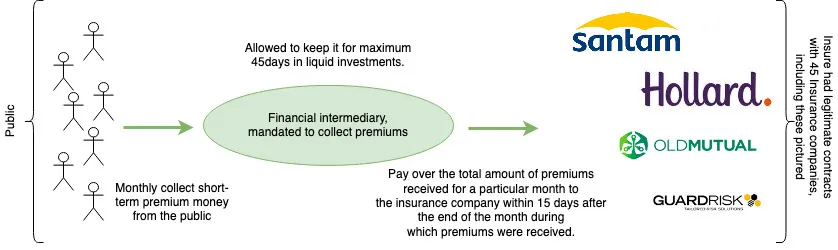

An intermediary should collect the short-term premiums from policyholders, and keep them for a maximum of 45 days in a liquid investment (like a high-interest bank account), before paying them to the insurer. The only money that can be deducted is clearly set out – like fees.

In simple terms, this graphic depicts what should have happened:

The process Insure Group Managers Limited should have followed in terms of the STIA, its regulations and Insure’s contracts with the various insurance companies.

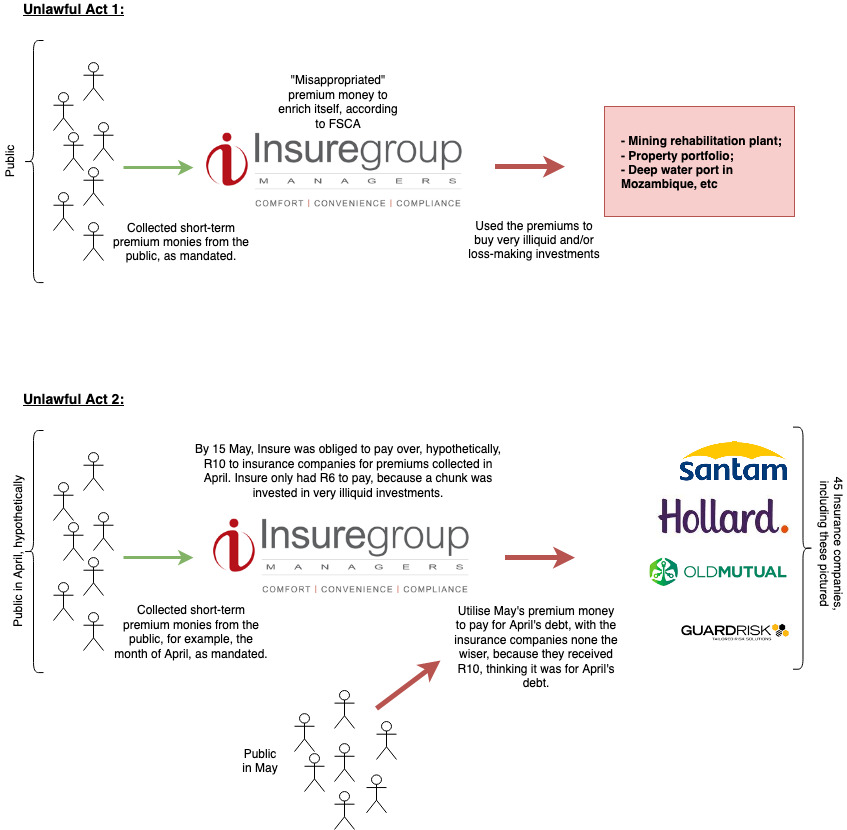

In Insure’s case, the insurers did not authorise the intermediary to reinvest those premiums in any long-term, high-risk or illiquid assets. “There was no express or implied term permitting Insure to use the premium for its own benefit,” Topham confirmed to Scorpio.

Then, to cover up the secret, Insure began using the premiums collected for future months to pay the premiums due for the previous month. This is what the FSCA means when it speaks of a “roll-over”.

One of the potential consequences, says Topham, is that it “created a systemic risk for the insurance sector”.

This graphic depicts in a hypothetical and simplified way what Insure actually did:

The two unlawful acts Insure Group Managers Limited followed in secret, intending to line its own pockets, which is a contravention of the STIA, its regulations and Insure’s contracts with the various insurance companies, the FSCA argues.

“An aggravating factor was that the investments were into illiquid assets,” Topham said.

An illiquid asset is an investment that can’t easily be sold and converted to cash. By contrast, a liquid asset includes cash in a bank account.

Scorpio spoke to 52 sources in this investigation – including brokers, underwriters, insurers, lawyers, regulators, Insure-insiders as well as directors of large insurers – and all, without fail, spoke of “unhappiness” and “a lot of anger” with Cilliers and Burns.

This is understandable, considering that while the big established companies could absorb the knock, smaller companies – like Lion of Africa – had to close shop.

While fingers are also pointing at the regulator, the FSCA says it has its finger on the pulse, and will consider debarring other Insure employees, once the curator’s report is finalised.

Meanwhile, Burns continues to stick to her view that she was a “whistle-blower” – hopefully, she’ll spell out exactly why in her appeal of the debarment in July.

In the next article, we will review how Cilliers was debarred by the FSCA, but escaped the net of the SA Institute of Chartered Accountants. DM

![]()

Pauli van Wyk is truly an investigative journalist of note. Uncovering the EFF’s looting at VBS, and now this one. Diane Burns appears to be an Ivanka Trump lookalike, and thus maybe a case of “birds of the same feathers”. And in typical corruption fashion, denying any wrong doing. Eish!

It is broadly accepted that the insurance industry do not operate on human values. Only monetary value counts. The big isurers will not foot the bill but pass on its losses by resisting pay-outs.

Regarding your first observation – it is a value inherited from the much misguided but vaunted US… especially by the Republicans . Any attempts to ‘regulate’ (common practise in most European countries) is promptly labelled as ‘big government’ or even worse & scarier ‘socialist’ ! 2nd – spot on !

HAHA! FSCA asleep?? Never.. VBS is proof that they are all a bunch of Rip Van Winkles.

How are these criminals not disbarred for life?? – 5 years – so they can do it again in 5 years time and the industry will probably let them and certain parties will take a cut. The legal system won’t even have processed them by then (if ever). Crime definitely pays in SA.

Long ago in the UK workers used to bet on the number of draws expected in the following Saturday’s football matches. The small amounts of money were collected by a fellow worker acting as an Agent who handed it to the Pools company. Regularly there was a rogue who collected but did not hand over.

….. This could go on for years and was only discovered when somebody in the group won, and the Pools company had no knowledge of the bet.

This is a very clear cut case of fraud so why haven’t these people been sentenced to jail terms yet? This country simply can’t progress while the criminal justice system is so inadequate.

I’m not sure this is the only problem with the short term insurance industry. Pauli should have a look into the way premiums are calculated. I’ve challenged the regulator to look into this but they’ve dodged the bullet. Basically the industry is uniformly charging more than legally required.

That such “misappropriation” was happening as far back as 2012 – but only discovered now? This means that the Insurance companies as well as the Regulatory Authority were fast asleep at the wheel! All should face charges & its time that punitive personal costs become the norm!

They probably all had some idea about what was happening but “turned a blind eye” as the premiums were being paid. So why “rock the boat”. I think a bit more digging into the financial industry will uncover many, many unsavoury schemes.

It is not true to say that policyholders won’t take the effects. The insurers are going to have to leverage their margins (by charging more or paying less) to maintain their profit margins.

The insurance companies and FSCA slept and found the culprits and unsurprisingly it is not them. Did the insurers actually lose the money? Or did they simply refused to pay claims and passed it DIRECTLY to the public so the public lost out?

Many years ago I was advised by a very shrewd adviser that insurance should be avoided and only paid when lack of it could bankrupt me. His advice was that that I should do what the insurance companies do and invest the premiums. This certainly paid off.

Couldn’t agree more Mr Young! In my opinion, insurance is basically one of the most well-established yet somehow socially and morally accepted financial scams inflicted on humanity. The sector’s strategy is simple: sell policies and avoid claims by employing vast sales and legal resources.

Surely Insure Group’s auditors should have detected some of this. They had enough time if it started back in 2012… And SAICA sits on it’s hands as another of their esteemed members gets up to mischief. The SA accounting profession has become an embarrassment.

It’s not limited to SA. Some quick examples: Steinhoff, Enron, Worldcom etc. The auditing profession is inherently conflicted – how can the watchmen charge fees to those being watched?

Regarding your first observation – it is a value inherited from the much misguided but vaunted US… especially by the Republicans . Any attempts to ‘regulate’ (common practise in most European countries) is promptly labelled as ‘big government’ or even worse & scarier ‘socialist’ ! 2nd – spot on !

Sickening corporate greed has become a way of life in the upper echelons of SA big business. Perhaps it always has?

Go Pauli, go! I salute your courage and tenacity. Investigative journalists like you and of course everyone at Scorpio and amaBhungane are doing the country’s work, supported by DM insiders with zero government links or big biased media involved (I hope).

Hear, hear!! Very well said Geoff, thanks.

Orange!