(Photo: Waldo Swiegers / Bloomberg via Getty Images)

(Photo: Waldo Swiegers / Bloomberg via Getty Images) While the decline in the prime overdraft rate to 7% (since July 2020) has certainly led to an increase in the demand for mortgage loans and injected some much-needed life into the residential property market, the real prime rate remains at the relatively high level of almost 4%.

However grateful one should be for the lowering of the cost of capital by 30% (from the perspective of prioritising growth), the question arises whether monetary policy has, in fact, assumed an accommodating stance — the latter having become an alien concept to the Reserve Bank’s Monetary Policy Committee (MPC) ever since Gill Marcus retired as the bank’s governor at the end of 2014.

Unfortunately, the answer is no. During the five-year term served by Gill Marcus, South Africa enjoyed average real GDP growth of just below 3% per annum, on the back of an average real prime rate of around 3%. The MPC that was appointed in 2015 by the country’s previous president, Jacob Zuma, immediately adopted a hawkish stance towards monetary policy, ultimately leading to an increase in the real prime rate to more than 6% — which represented an increase in the cost of capital of more than 100% (as measured by prime).

SA is the odd one out

The monetary policy approach followed between 2009 and 2014 could best be described as neutral, with a marginally more lenient approach immediately after the 2008/09 global financial crisis.

With the current real prime rate at a level of almost 4%, South Africa is out of kilter with a number of its peers, including Brazil, Poland and Chile. It should be fairly obvious that the MPC is continuing to err on the side of caution and has not yet bid farewell to its obsession with the objective of low inflation.

With some key sectors of the economy still battling to recover from the pandemic and the consumer price index (CPI) languishing at the lower end of the inflation target range (which is, in any event, not cast in concrete), ample scope exists for a further reduction of the repo rate by at least 100 basis points.

Lowering the prime rate further, together with a firm commitment to assist the recovery process by prioritising economic growth and job creation, could be just the remedy required for a return to GDP growth of around 5% — a feat that was achieved for four successive years prior to the 2008/09 recession.

Retail trade sales for January and February should send a wake-up call to the MPC. Compared with the first two months of 2020, this key indicator of the state of the economy declined in real terms. It is also a point of concern that January’s nominal retail trade sales declined year on year for the first time since records have been kept.

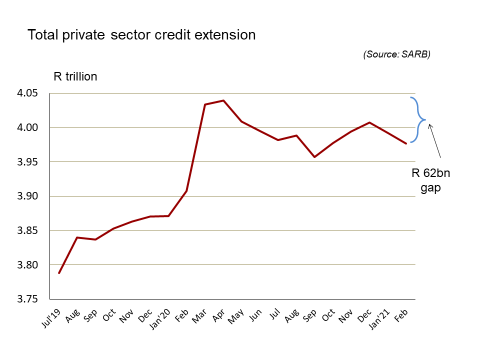

Another alarm bell over the sluggish progress with economic recovery that is ringing loud and clear is the decline in private sector credit extension, which seemed to have staged a slow comeback during the third quarter of 2020, but is now stuttering at a level of R62-billion less than in April 2020.

An economy simply cannot grow at rates commensurate with a meaningful lowering of unemployment unless private sector credit extension keeps expanding. The Minister of Finance and his team at National Treasury must be livid with the lack of support from the MPC, with a broadly stimulating (and appropriate) fiscal policy stance having been adopted in the February Budget.

When the R62-billion credit gap is applied to input-output table analysis, it translates into foregone fiscal revenues of close to R50-billion, which could have been utilised to accelerate the recovery process, including a broadening of the tax base.

Covid-19 was an extraordinary phenomenon that caused one of the most profound disruptions to the global economy in more than a century. It did not lead to a normal recession. Remedies should therefore also not be limited to what has traditionally been regarded as normal.

Getting back to meaningful growth and job creation requires a bold approach. A prime rate at 6% or even lower may just do the trick. BM/DM

Dr Roelof Botha is Economic Adviser to the Optimum Group.