However, for many South African investors, it still does not appear simple. Rand hedging, ETFs, LIFE wrappers, endowments, sinking funds, asset swaps, LISPs… the list of terminology in this world can result in confusion, if not a pounding headache.

Michael Summerton, head of proposition and marketing at INN8, an investment platform built with advisers in mind, believes that the minefield of jargon should not deter investors from taking the leap. In fact, he says, even if you think you haven’t, you might already have skin in the offshore game.

“People have offshore exposure already, they just don’t know it,” says Summerton. Considering that imports make up around 30% of the country’s GDP, residents’ lives are already impacted by what happens outside our borders.

“Living in South Africa, chances are that you own imported goods that were priced in foreign currency, perhaps the latest smartphone or designer jeans. Everyone is impacted by the US dollar to some extent because we use fuel made from crude oil which is priced in that currency,” he says.

Hence, the need to make sure you have some non-Rand exposure.

Secondly, says Summerton, South Africans who have a pension fund through their employer, might be surprised at how much exposure they already have to different offshore asset classes, through the underlying funds that make up their pension fund investments. This is also true for retirees who are drawing an income from their living annuities since you may select funds with offshore exposure within that product.

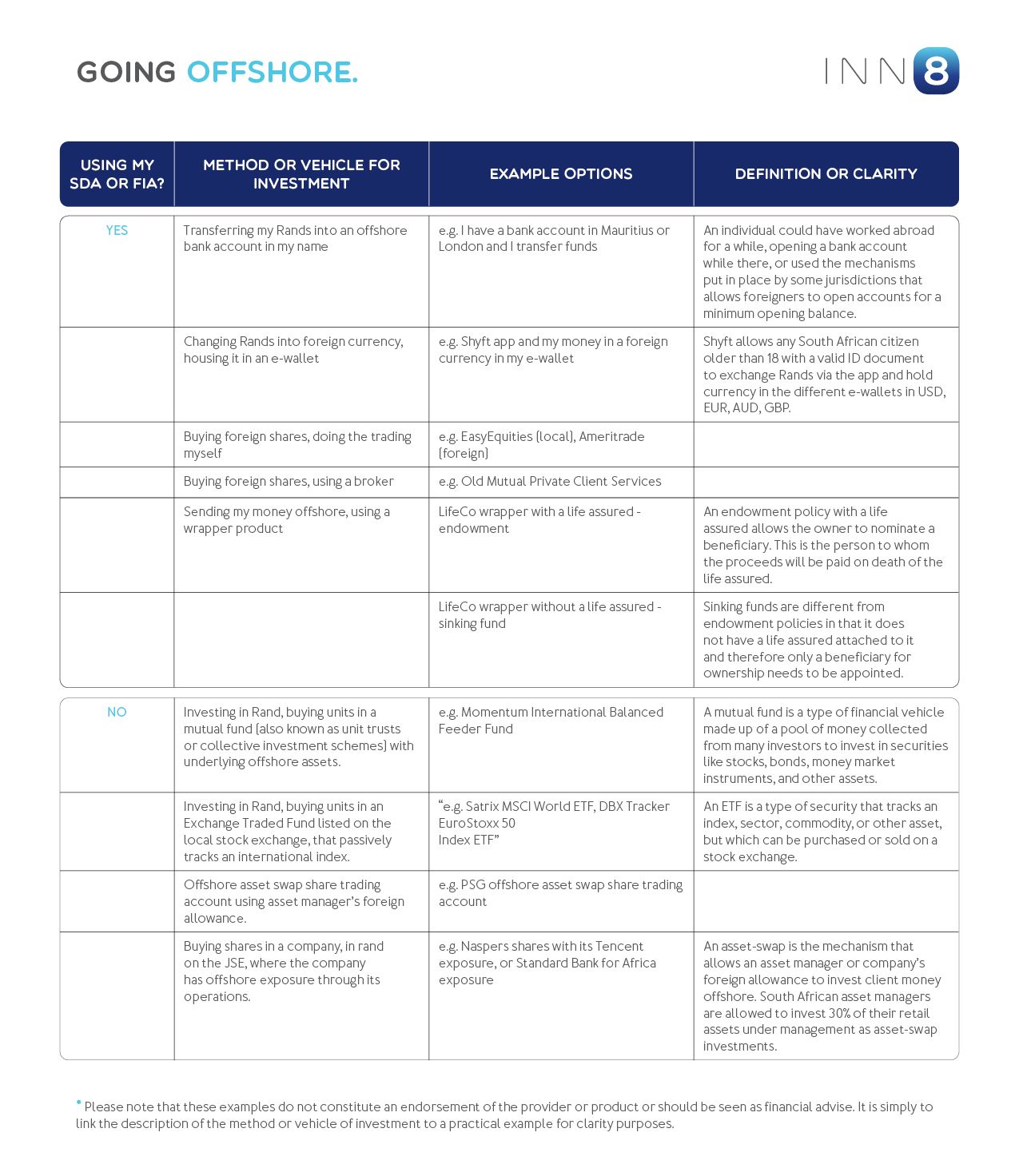

If you want to exchange your Rands into foreign currency, the South African Reserve Bank (SARB) provides each and every citizen an offshore allowance. Every year, without any approval from SARB, as part of your Single Discretionary Allowance (SDA), you are free to take up to R1 million out of the country - whether it be by swiping your credit card overseas or transferring money into a sinking fund with a life company domiciled in Guernsey, for example. If you go through a few simple steps to get tax clearance from the South African Revenue Service (SARS) - they simply acknowledge that your tax affairs are in order - the SARB allows you a further R10 million per year as part of your Foreign Investment Allowance (FIA).

“There are no more barriers to entry,” says Summerton. “If you have a bank account in South Africa, you can open an app on your phone and remit that R1 million overseas without leaving your couch,” he says. “It is so simple and a lot more transparent these days.”

And if you want to move more than the R1 million through your FIA, companies like Exchange4free make the process a lot easier, to the point where asset managers such as Coronation suggest their services on their online application forms.

If we then wade through the options for offshore investments or exposure, this is perhaps a good starting point – whether you must use your SDA or FIA, or whether you can obtain that exposure without using your allowance. You can, for example, purchase a share on the local stock exchange that has offshore exposure due to its operations in China, or you can invest in a rand-denominated unit trust fund where the asset manager is using its allowance to invest in underlying assets abroad. If you look at the table provided below, you will see that there are various options available depending on the amount you have and the type of exposure you want.

INN8 has compiled a white paper to demystify the world of offshore investments. The paper goes into the detail of the advantages as well as risks that could be associated with the options at your disposal. It is available here.

Summerton suggests that, due to the very personal nature of financial planning, it is worthwhile for you to discuss your financial goals and plans when it comes to offshore exposure, with a registered financial adviser that you trust.

“Some of the topics to cover when having the conversation with your adviser are access to your savings, how the fees work, the frequency and transparency of reporting, access to fund commentary, the legitimacy of the jurisdiction where the money is invested and your tax obligations,” he says. DM/BM

Liberty Group Limited is a Registered Long-Term Insurer and an authorised Financial Services Provider (“FSP”) with FSP number 4209 and registered office residing at 1 Ameshoff Street, Braamfontein, Johannesburg, 2001; INN8 is a registered trademark of STANLIB Wealth Management (Pty) Limited, an authorised FSP with licence number 590 and registered office residing at 17 Melrose Boulevard, Melrose Arch, Johannesburg, 2196, South Africa; and a registered business name of STANLIB Fund Managers Jersey Limited, regulated by the Jersey Financial Services Commission with registration number 30487 and registered office residing at Standard Bank House, 47-49 La Motte Street, St Helier, Jersey JE2 4SZ. © 2019 INN8