“He came out swinging,” said Roberto Perli, a former Fed economist who is now a partner at Cornerstone Macro in Washington. The press conference “was an exercise in hammering through the same message over and over: we are committed to the new framework and what we are doing.”

Read More: Powell Holds Dovish Line as Fed Signals Zero Rates Through 2023

As a result, the Fed will wait for accumulating proof of “substantial further progress” on its employment and inflation goals before paring back its $120 billion in monthly bond purchases.

“Until we give a signal, you can assume we are not there yet,” Powell said after the Fed held rates near zero and signaled they’d stay that way through 2023. “As we approach it, well in advance, we will give a signal that, yes, we’re on a path to possibly achieve that, to consider tapering.”

Ten-year Treasury yields rose to 1.687% earlier on Wednesday, the highest in more than a year, but ended the day slightly lower as investors absorbed the message.

Powell’s challenge was to embrace the coming economic strength that will be delivered by massive fiscal aid from Washington, while assuring investors that “we’re not going to act preemptively on forecasts.”

”It was a clean break,” from past Fed practice, said Lou Crandall, chief economist at Wrightson ICAP LLC. “They’re willing to take the risk of being behind the curve. They don’t think the risk is particularly severe and they don’t think the costs of a miss on that side are as large as the costs of suppressing economic growth unnecessarily.”

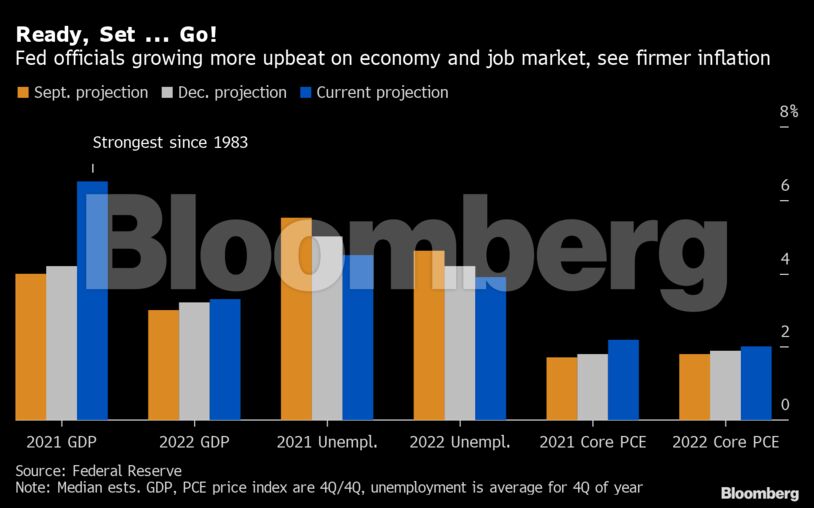

The Fed’s forecasts showed unemployment dipping to a pre-pandemic levels of 3.5% by the end of 2023, with inflation nudging slightly above its 2% goal.

Officials raised their economic growth forecast to 6.5% for this year — which would be the fastest pace since 1983 measured fourth quarter over the same three months a year earlier — but then the impulse from pent-up demand and fiscal policy fades. Officials see growth advancing 3.3% in 2022 and 2.2% in 2023.

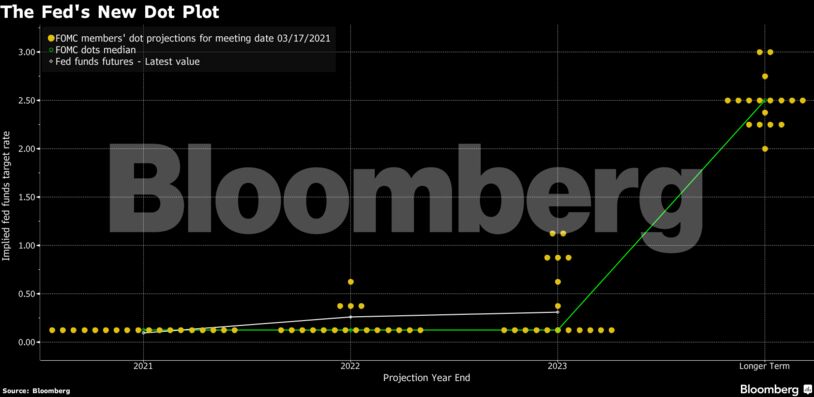

Powell dismissed the Fed’s rate outlook — or dot plot — which showed seven of 18 officials predicted higher rates by the end of 2023 compared with five of 17 at the December gathering. He said the bulk of the committee expected rates to be near zero for the next three years. Prior to liftoff, they would also need to see “actual progress, not forecast progress — and that’s a difference from our past approach.”

U.S. central bankers conducted a broad internal review of monetary policy and announced their findings in August. They discovered that their previous focus on narrow indicators for employment and forecast-based policy leaned against more inclusive labor-market gains. Their new strategy seeks to average 2% inflation over time and they define maximum employment as a broad and inclusive objective.

The last rate-hike cycle began in December 2015. At the time, the unemployment rate for Black Americans was over 9% for November and inflation never reached 2% on a sustained basis in subsequent years, raising questions about whether the increase was premature.

In January, Fed Governor Lael Brainard said gains in employment “may have come sooner and been greater” if the new framework had been in place during the previous recovery.

Powell stressed that a global pandemic and a fiscal response of this size was not something forecasters have a lot of experience with calibrating, while both the labor market and inflation remain far from the Fed’s goals.

“They are looking back to the pre-Covid period and viewing their forecasts as too optimistic,” said Conrad DeQuadros, senior economic adviser at Brean Capital LLC. “They are saying, ‘We don’t want to make that mistake again.”’

–With assistance from Steve Matthews and Rich Miller.

Comments - Please login in order to comment.