Photo by Ralf Leineweber on Unsplash

Photo by Ralf Leineweber on Unsplash Yes, there are what we term “mania” or “bubble” sectors within the Chinese equity markets that appear to be “bursting”, and we believe this is healthy for the market as a whole. This type of correction contributes positively to the long-term sustainable growth of the Chinese equity markets.

However, in South Africa and the traditional Western markets, China is very under-represented, primarily due to historical market access issues and, more lately, perception issues. This is, however, changing at a reasonable pace as investors search for high returns globally.

Two things stand in China’s favour as an investment destination – favourable stock market valuations and a positive macro-economic backdrop. With most investors substantially underinvested in China, investors should seriously consider taking advantage of the emerging market-type return profiles, with the stability profile of developed markets.

China is, by far, the second-largest equity market in the world. Its size is about one-third of the US equity market and more than four times the size of the UK/London market. In 2021, the Chinese market is simply too large to ignore and too large to fit into a small emerging market (EM) allocation.

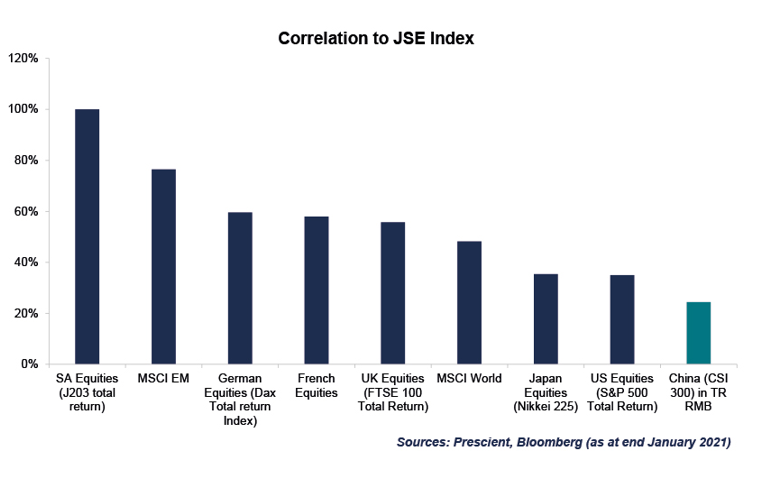

From a South African investor perspective, Mainland Chinese equities offer some of the world's best diversification benefits, as the CSI300 Index has one of the lowest correlations to the JSE.

While we believe the Chinese equity market is no longer cheap compared to its own history, it is very far from “long-term financial trouble”, and the US should be a leading indicator to such an expectation, given the inflated stock market valuations there.

One example that confirms the sell-off has been a healthy correction is Haitian, a company that produces condiments and focuses on products such as soy sauce. The share price has fallen 23.5% in a month, and the forward PE ratio is now around 79 times.

There are many companies with valuation profiles, similar to Haitian. To put it in simple terms, it will take almost 79 years of earnings for an investor to “break-even” if they buy Haitian stock at current prices, all else being equal. Sounds high, right? You will be shocked at how cheap this is compared to many US-listed companies; take TSLA and NIO as examples.

On Haitian specifically, our view at Prescient is that no matter how fast the Chinese economy grows, Chinese people will not suddenly start drinking soy sauce or other sauces like cooldrink.

Without a clear growth trajectory, we believe the current valuation of Haitian, and many other similar stocks, such as liquor companies, are not justified. We, therefore, hold underweight positions in these companies.

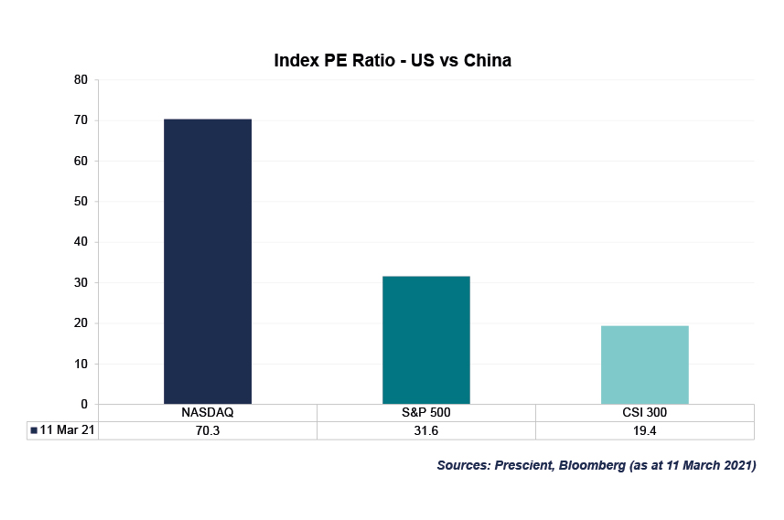

If you compare China to the US equity markets as at 11 March, the price to earnings ratio of the Chinese CSI300 Index was 19.4. That compares with the S&P 500 Index PE of 31.6 and the NASDAQ Composite Index PE of 70.3 – yes, the entire index is almost as expensive as Haitian! On this basis, CSI300 is 39% cheaper than S&P500 and 72% cheaper than the NASDAQ.

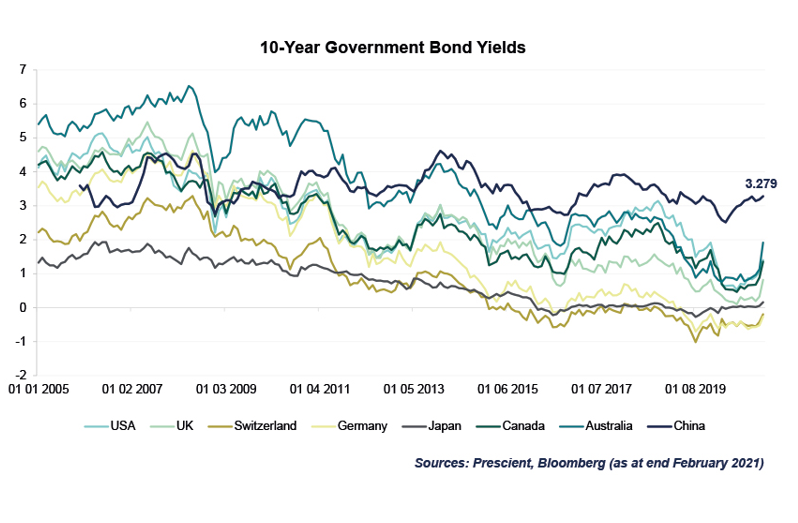

Fixed-income assets are also significantly more attractive in China than developed market peers, where yields are extremely low. Chinese 10-year government bonds are yielding around 3.3% compared to much lower rates in other major developed markets and even negative rates in Europe. The chart below shows a comparison of how China’s yield has stayed fairly consistent while the yields of developed market peers have dropped significantly over time.

From a macro-economic point of view, global economic growth will be mainly driven by China, which adds to the argument that it would be prudent to give China’s market more attention and focus.

China was the only major economy to post positive GDP growth for 2020 at 2.3%. Globally economies have been hit hard by Covid-19 and lockdowns that hampered economic activity. If we look at China, as mentioned above, we feel the economy is in a strong position to grow sustainably going forward. The consensus expectation is for China’s GDP to grow at 8.4% in 2021.

In the wake of the latest NPC meeting, we are very encouraged and believe the policies are positive for long-term sustainable growth in China from what we've seen so far. We believe the Chinese government is being very prudent and responsible in policy direction. We have been investing into China since 2013 and have first-hand experience of the policy progression, which has been consistently moving towards becoming more market-friendly and, specifically, market-friendly for foreign investors.

Some of the key points that came out from the latest Chinese NPC meeting:

- A focus on domestic R&D to reduce reliance on Western technologies in the wake of recent US sanctions, targeting 7% annual growth in R&D spending through 2025.

- A focus on reducing carbon emissions, partly by approving more nuclear reactors.

- Government targeting 6% economic growth, while the economic consensus is at 8.4%. This is positive for the long-term as it gives the government room to focus on longer-term projects rather than “pretty” short-term GDP numbers.

- The government is targeting a smaller budget deficit this year, at 3.2%, which is much smaller than the deficits of other major economies, such as the USA, UK and Japan.

- Monetary policy remains consistent: supporting economic growth and controlling financial risks. We expect levels of liquidity in the Chinese financial system to remain stable.

Overall, we view China's current macroeconomic policies as responsible and “sober” compared with the massive fiscal and monetary stimulus in the West. We expect China to produce more organic and sustainable economic growth going forward.

If we turn our attention to other major economies outside of China, the picture is not as pretty. Economic fundamentals are weak, but asset prices are highly inflated due to the seemingly endless stimulus. One can say that the Western central banks are doing all they can to support the financial markets. Still, we are heading into unprecedented territory in terms of stimulus and overall indebtedness. GDP figures are expected to look much better in 2021 than in 2020, but we are worried about the sustainability of current fiscal and monetary policy in developed market economies.

We hope that vaccination programs will be successful this year so that global economic activity can return to pre-Covid-19 levels. Regarding financial markets, we are worried about the US equity market valuations that make up the bulk of global developed market equities. Europe continues to struggle with a lack of growth and negative interest rates, among other problems. Emerging markets, excluding China, are also all valued at premiums compared to China. So purely judging by the numbers, China is probably one of the safest places to be invested in for 2021. Overall, on a relative basis, we feel China presents a great overall investment opportunity in 2021 across all asset classes. BM

/file/dailymaverick/wp-content/uploads/Tian-Pan.jpg "This article was written by Tian Pan, Head of Product and Business Development at Prescient China")

This article was written by Tian Pan, Head of Product and Business Development at Prescient China

Disclaimer

- The information contained herein is provided for general information purposes only. This information does not constitute a solicitation, recommendation, guidance or proposal, and the service provided is not intended nor does it constitute financial, tax, legal, investment or other advice. Whilst reasonable steps are taken to ensure the accuracy and integrity of information contained herein, Prescient accepts no liability or responsibility whatsoever if any information is, for whatever reason, incorrect. Prescient further accepts no responsibility for any loss or damage that may arise from reliance on information contained herein.

- Prescient Investment Management Ltd, is an authorised financial services provider (FSP 612). There is no guarantee in respect of capital or returns in a portfolio and provided for illustrative purposes. Please note that there are risks involved in buying or selling any financial product, and past performance of a financial product is not necessarily indicative of the future performance. The value of financial products can increase as well as decrease over time, depending on the value of the underlying securities and market conditions.