Proponents of value go further, speculating that this rally may spark a return to the glory days of protracted performance for this investment style.

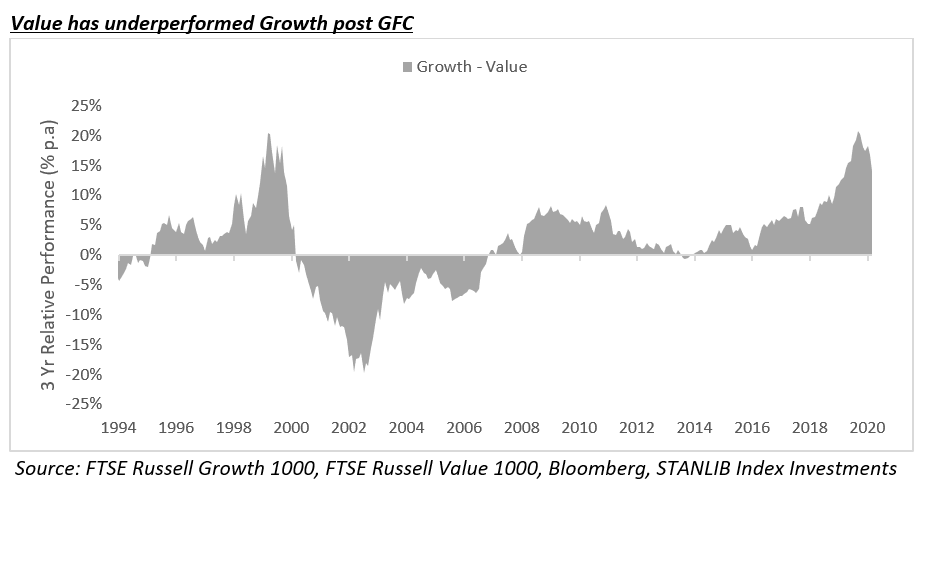

It has been starkly evident (as shown in the chart) that value investing as a long(er) term strategy has struggled in the 12 years since the global financial crisis (GFC) of 2008.

Theories about why value no longer performs as an investment style and why it may continue to underperform include:

1) Too many investors are now chasing the well-known value premium and this may be crowding out and eroding the associated alpha.

2) Exogenous elements such as the low interest rate regime post GFC and the rise of index funds which made value investing less attractive to investors.

3) Structural changes in underlying business models, which mean traditional markers or measurements of value (e.g. Price / Earnings (P/E), Price to Book (P/B) and Dividend Yield (DY)) are archaic in devising a successful long-term value investing strategy.

These views on the failure of value may be valid from various perspectives. However, when we closely examine the sharp and short-lived nature of recent value rallies, it is clear that the initial burst of any value rally can be largely attributed to the macroeconomic environment, particularly market exuberance over an anticipated recovery phase in the economic cycle. This in turn fuels the price performance of these previously cheap and out-of-favour value stocks. The initial surge in prices is typically short-lived as it becomes clear that the earnings of these value stocks inevitably fail to significantly justify, match and sustain their initial price rally. To put it simply, earnings just do not catch up to price. The disappointing result for long-term investors is being “left on the dancefloor” when the music stops playing.

Another value rally or sustainable performance?

Our view is based on firstly understanding when and why value stocks outperform the market. We then broaden the discussion to whether the value rally that started in mid-2020 is any different from other value rallies in recent history. Here, we will put forward our reservations about whether this recent value rally is sustainable for the next five years (and perhaps longer). Finally, we close with what we think is the outlook for value investing in 2021.

Value performs on the basis of a better tomorrow

Our analysis shows that the value factor (a term used by quantitative investors to capture value style as a factor of equity market performance) outperforms when there is a pervasive market belief in the improvement of the immediate future macroeconomic environment.

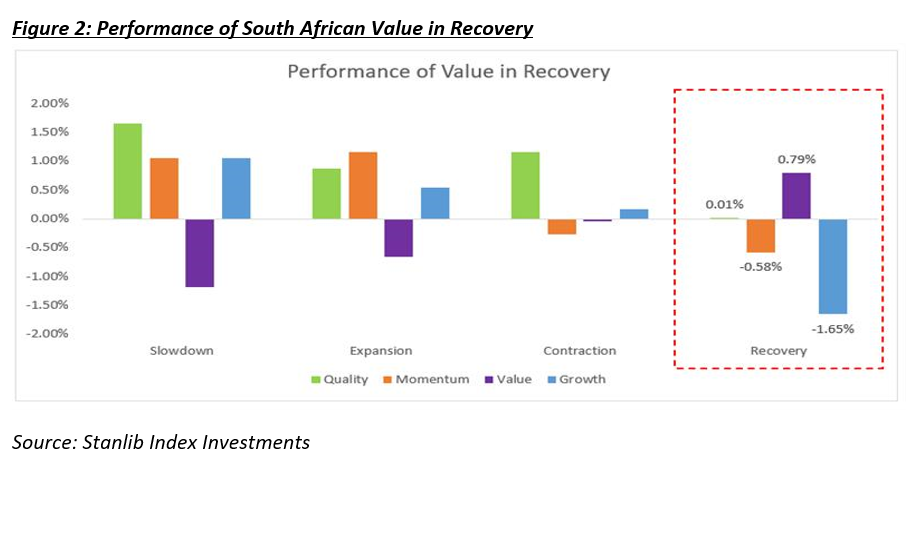

Using STANLIB Index Investments’ proprietary macro indicator (see Figure 1), and averaging the returns of the value factor in the different macro phase environments, shows that value performs best in the recovery phase of the economy (see Figure 2). Interestingly, it is also the only factor that performs in a recovery phase.

Why? Cheap value companies tend to be riskier investments because they are less agile, nimble and adaptable (in comparison to their growth counterparts) to the changing macro-economic environments, so they are more vulnerable to the market’s perceptions of the future. When markets anticipate a better future because of improving macroeconomic data such as GDP, PMI, regime changes (and even socioeconomic news like vaccine rollouts), the out-of-favour cheap companies rally on this positive ‘risk-on’ market sentiment.

But for how long?

To understand the concept of a sustainable rally, i.e. whether a rally can continue for five years or longer, we need to consider what key ingredients define it. As noted above, the first event is that improving macro information stimulates market participants’ expectation of the future.

The resulting ‘risk-on’ appetite will then fuel the performance of risky cheap companies in what we perceive as a value rally. The differentiator for sustainability comes in the final, critical phase when the “cheap” companies follow through by delivering earnings in line with or exceeding market expectations.

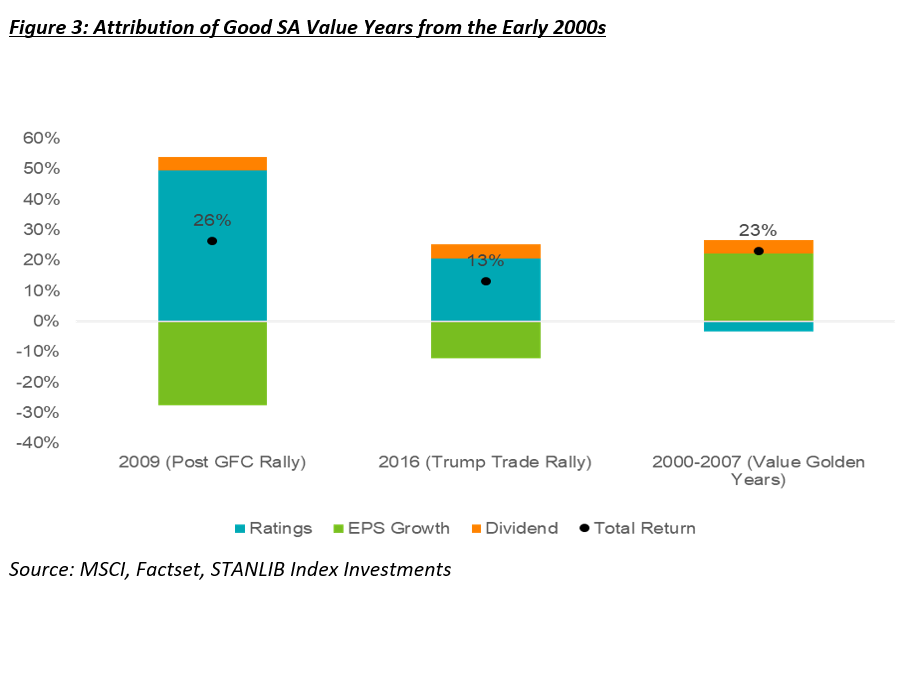

To better understand these elusive fundamentals of the value factor, we borrow the return attribution tool shown below (see Figures 3 and 4) used by many fundamental managers to dissect the returns of the quantitative value factor by assessing the factor’s performance from the early 2000s. It is important to note that there were two notable calendar periods recently when value investing reported excellent market-beating returns: 2009 (post-GFC crisis) and 2016 (the ‘Trump trade’).

What is evident from these events is that the double-digit returns are primarily attributable to changes in market expectation or re-ratings (see blue shaded portion of Figure 3) and not due to changes in the underlying earnings of the companies (green portion of Figure 3). This implies that these companies have rallied on the basis of positive market expectations, not because there were any fundamental earning shifts or improvements in their underlying earnings.

On the other hand, if you contrast this with the value golden era between 2000-2007, we see that most of the returns of the value factor then were due to the meaningful improvement in earnings of these value companies (see green shaded portion of Figure 3), which allowed value to rally for these seven years (see Figure 3).

More recently, we see that in 2020, in the midst of turbulent COVID-19 markets, value stocks initially tanked, primarily driven down by ratings downgrades as market analysts doubted how robust these businesses would be in managing COVID-19. After that, when an improving COVID-19 outlook revived the macroeconomic recovery, we saw these companies being bought up again as risk-on appetite based on re-ratings returned. But, again, because this rally is not based on core changes in business earnings, it closely resembles the short-lived ratings-driven performance trends we saw in 2009 and 2016.

Although this rally resembles 2009 and 2016, could this time be different? Or, to rephrase, will value companies actually improve their earnings in comparison to the rest of the market after the crisis period of COVID-19?

Our research into these value stocks reveals that, because they were actually cheap for valid reasons in the first place, they are unlikely to provide earnings that justify their initial price rally. While these stocks may perform well for short-term traders, they are unlikely to yield favourable results for longer-term investors looking for sustained growth from the investments. Again, our view is not that value investing is useless or dead but rather that any stock, sector or factor will only have a sustainable rally if eventually the earnings fundamentals justify the higher price.

Value style: 2021 and beyond

In 2021 there are high expectations for the COVID -19 vaccine rollout and a resultant recovery in the macroeconomic and socioeconomic environment. We, therefore, agree that in the short-term the value factor is likely to continue to outperform growth and other style factors, provided that the vaccine rollouts are implemented with no major hiccups and no other macroeconomic shocks lie in wait. However, we contend that the ‘risk-on’ appetite will eventually fizzle out, as previous value rallies did, as companies inevitably fail to deliver earnings that justify, match and sustain their initial price rally.

For the past few years, pressures on South African companies have got heavier with each economic cycle, and value companies have suffered the most as they struggled to negotiate turbulent financial markets. Economic cycle rotation is very tricky to predict: you can have a great deal of confidence in what exactly needs to happen to spur a move from growth to value stocks, but you cannot be sure of the timing. This delicate and intricate portfolio manoeuvring has humbled even the most seasoned of portfolio managers.

Style diversification is critical

This is precisely why investment style diversification is key. As quantitative portfolio managers, we believe that the value factor has a meaningful role to play in investment portfolio construction, since it is the only factor that performs during a recovery environment (see Figure 2). The STANLIB Index Investments’ house view is that diversification through a multi-style (multi-factor) approach is essential for long-term successful portfolio construction, rather than the single style and inflexible value vs growth debate. We are keenly watching the value rally, but we remain cautious about its sustainability in the long term. BM/DM

This article was written by Ann Sebastian, STANLIB Index Investments