Pedestrians walk on Alfandega Street in Rio de Janeiro, Brazil, on Thursday, July 23, 2020. Brazil registered 67,860 new cases on Wednesday, more than 20% above the previous record for daily infections. Photographer: Andre Coelho/Bloomberg

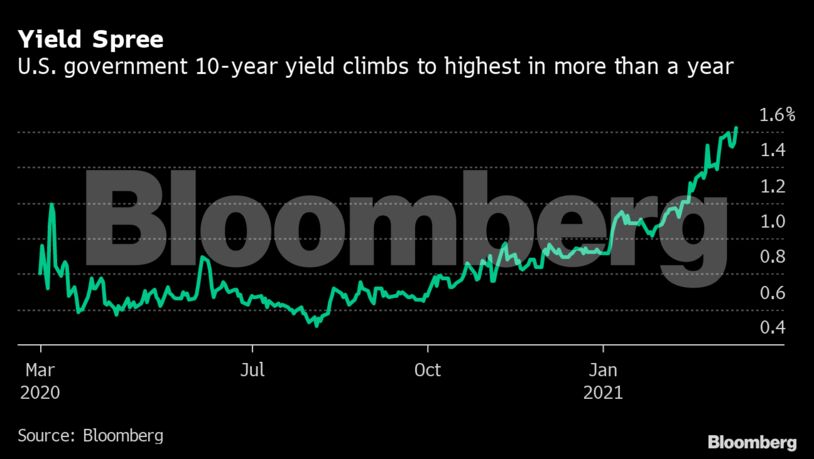

Pedestrians walk on Alfandega Street in Rio de Janeiro, Brazil, on Thursday, July 23, 2020. Brazil registered 67,860 new cases on Wednesday, more than 20% above the previous record for daily infections. Photographer: Andre Coelho/Bloomberg Behind the shift: Renewed optimism in the outlook for the world economy amid greater U.S. stimulus. That’s pushing up commodity-price inflation and global bond yields, while weighing on the currencies of developing nations as capital heads elsewhere.

The turn in policy is likely to inflict the greatest pain on those economies that are still struggling to recover or whose debt burdens swelled during the pandemic. Moreover, the gains in consumer prices, including food costs, that will prompt the higher rates may exact the greatest toll on the world’s poorest.

“The food-price story and the inflation story are important on the issue of inequality, in terms of a shock that has very unequal effects,” said Carmen Reinhart, the chief economist at the World Bank, said in an interview, citing Turkey and Nigeria as countries at risk. “What you may see are a series of rate hikes in emerging markets trying to deal with the effects of the currency slide and trying to limit the upside on inflation.”

Investors are on guard. The MSCI Emerging Markets Index of currencies has dropped 0.5% in 2021 after climbing 3.3% last year. The Bloomberg Commodity Index has jumped 10%, with crude oil rebounding to its highest levels in almost two years.

Rate increases are an issue for emerging markets because of a surge in pandemic-related borrowing. Total outstanding debt across the developing world rose to 250% of the countries’ combined gross domestic product last year as governments, companies and households globally raised $24 trillion to offset the fallout from the pandemic. The biggest increases were in China, Turkey, South Korea and the United Arab Emirates.

What Bloomberg Economics Says...

“The tide is turning for emerging-market central banks. Its timing is unfortunate -- most emerging markets have yet to fully recover from the pandemic recession.”

-- Ziad Daoud, chief emerging markets economist

Click here for the full report

And there’s little chance of borrowing loads easing any time soon. The Organisation for Economic Co-operation and Development and the International Monetary Fund are among those that have warned governments not to remove stimulus too soon. Moody’s Investors Service says it’s a dynamic that’s here to stay.

“While asset prices and debt issuers’ market access have largely recovered from the shock, leverage metrics have shifted more permanently,” Colin Ellis, chief credit officer at the ratings company in London, and Anne Van Praagh, fixed-income managing director in New York, wrote in a report last week. “This is particularly evident for sovereigns, some of which have spent unprecedented sums to fight the pandemic and shore up economic activity.”

Further complicating the outlook for emerging markets is they have typically been slower to roll out vaccines. Citigroup Inc. reckons such economies won’t form herd immunity until some point between the end of the third quarter of this year and the first half of 2022. Developed economies are seen doing so by the end of 2021.

The first to change course will likely be Brazil. Policy makers are forecast to lift the benchmark rate by 50 basis to 2.5% when they meet Wednesday. Turkey’s central bank, which has already embarked on rate increases to shore up the lira and tame inflation, convenes the following day, with a 100 basis-point move in the cards. On Friday, Russia could signal tightening is imminent.

Nigeria and Argentina could then raise their rates as soon as the second quarter, according to Bloomberg Economics. Market metrics show expectations are also building for policy tightening in India, South Korea, Malaysia and Thailand.

| Read More |

|---|

|

“Given higher global rates and what is likely to be firming core inflation next year, we pull forward our forecasts for monetary policy normalization for most central banks to 2022, from late 2022 or 2023 earlier,” Goldman Sachs Group Inc. analysts wrote in a report Monday. “For RBI, the liquidity tightening this year could morph into a hiking cycle next year given the faster recovery path and high and sticky core inflation.”

Some countries may still be in a better position to weather the storm than during the “taper tantrum” of 2013 when bets on cuts in U.S. stimulus triggered capital outflows and sudden gyrations in foreign-exchange markets. In emerging Asia, central banks have built up critical buffers, partly by adding $468 billion to their foreign reserves last year, the most in eight years.

Yet higher rates will expose countries, such as Brazil and South Africa, that are ill-positioned to stabilize the debt they’ve run up in the past year, Sergi Lanau and Jonathan Fortun, economists at the Washington-based Institute of International Finance, said in a report last week.

“Relative to developed markets, the room low rates afford emerging markets is more limited,” they wrote. “Higher interest rates would reduce fiscal space significantly. Only high-growth Asian emerging markets would be able to run primary deficits and still stabilize debt.”

Among those most at risk are markets still heavily dependent on foreign-currency debt, such as Turkey, Kenya and Tunisia, William Jackson, chief emerging markets economist at Capital Economics in London, said in a report. Yet local-currency sovereign bond yields also have risen, hurting Latin American economies most, he said.

Other emerging markets could be forced to put off their own fiscal measures following the passage of the $1.9 trillion U.S. stimulus plan, a danger underlined by Nomura Holdings Inc. more than a month ago.

“Governments may be tempted to follow Janet Yellen’s clarion call to act big this year on fiscal policy, to continue to run large or even larger fiscal deficits,” Rob Subbaraman, head of global markets research at Nomura in Singapore, wrote in a recent report. “However, this would be a dangerous strategy.”

The net interest burden of emerging-market governments is more than three times that of their developed-market counterparts, while emerging markets are both more inflation-prone and dependent on external financing, he said.

In addition to South Africa, Nomura highlighted Egypt, Pakistan and India as markets where net interest payments on government debt surged from 2011 to 2020 as a share of output.