As Dean Curnutt at Macro Risk Advisors puts it, the VIX is “on an island of its own.” And there are no easy explanations.

As the market rotation reduces correlations and increases risk appetite, Wall Street strategists have long expected a spirited drop in the gauge, which uses the options market to measure the 30-day implied volatility of the S&P 500.

So here are four theories on why things are not so simple in volatility land.

The Aftershocks

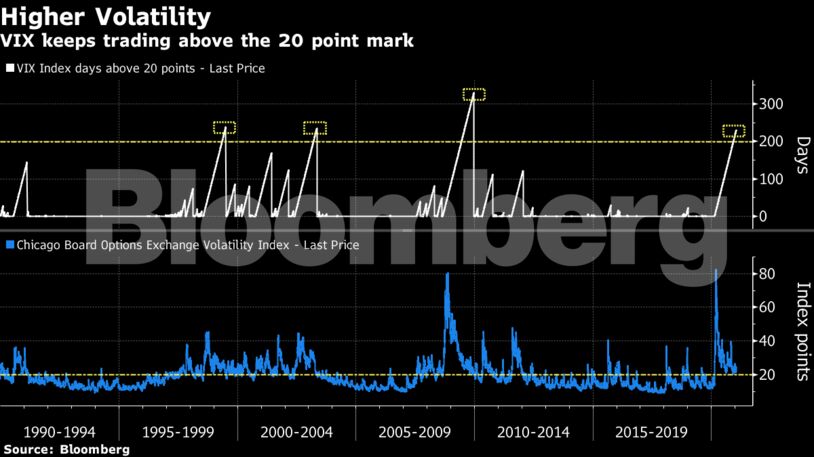

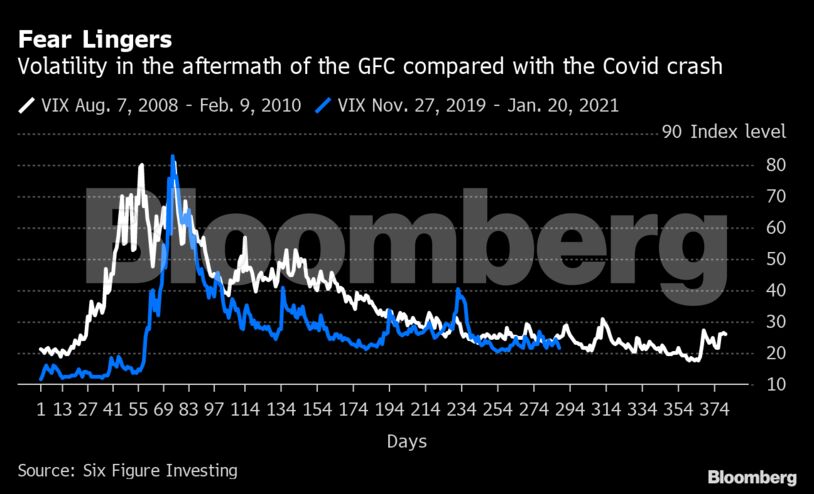

First and foremost: Past is prologue. Historically, volatility shocks like the Covid-spurred mayhem in March have taken time to run their course. After all, implied volatility largely reflects what’s recently happened in markets. In the wake of the global financial crisis, it took some 15 months for the measure to normalize.

Yet it’s been just 10 months since the stock wipeout that sent the VIX soaring to a record.

Given precedent, it could be several months before the fear gauge settles at a more subdued level especially in light of the extended collapse in the global investment and consumption cycle.

“The VIX dropped off more quickly than usual but now has entered a slower decline,” said Vance Harwood of Six Figure Investing, a consultancy specializing in volatility. “We are just seeing the normal after-effects of a market crash.”

Add delays to vaccine roll-outs, and there are good reasons why it’s a long journey back to a pre-pandemic normal of sorts.

Blame Tech

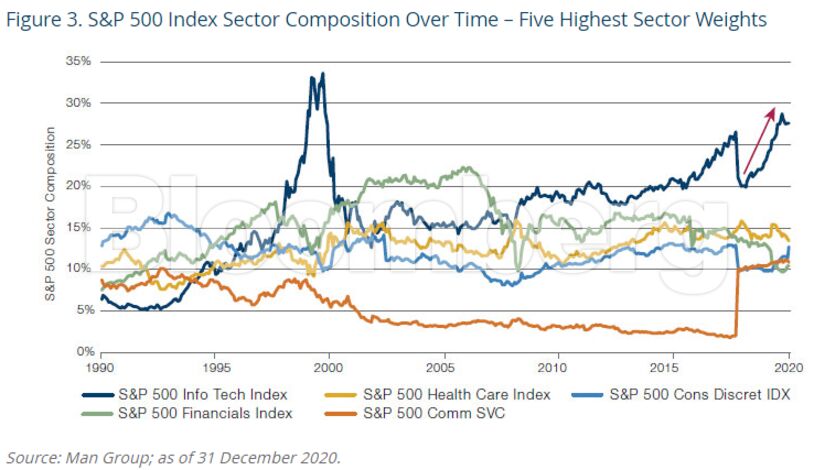

Perhaps something else is at work too. Hedge fund Man Group, for one, blames the increasingly large weighting of technology in the S&P 500 Index.

Tech shares are now approaching a 30% weighting in the U.S. stock benchmark, up from around 20% five years ago, according to Man. Over the past year, investors have piled into these names as part of the stay-at-home trade, leading to sharp sell-offs when sentiment reverses.

When a volatile sector comes to dominate the benchmark, “we get more instances of simultaneous increases in equity markets and volatility, notably during the tech bubble of the late 1990s,” strategists at the firm wrote in a note. “Indeed, we see a similar make-up of the S&P 500 today.”

No wonder stocks have risen along with implied volatility lately — bucking the historic norm.

In Man’s view, a “gentle rebalancing” of the equity market leaderboard at the expense of the tech sector would spur a fall in the VIX. Otherwise, brace for higher implied volatility for longer.

Call Fever

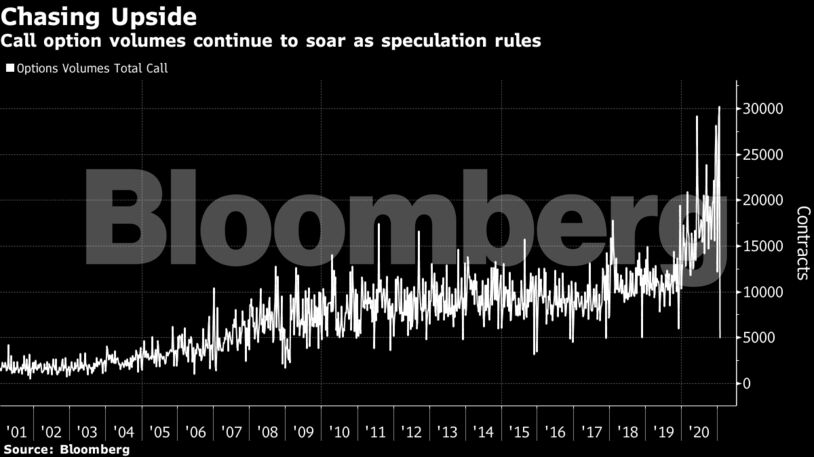

The explosion of call-option buying has also become an undeniable force in markets, with some blaming it for pushing around the underlying stocks. A more direct impact has been to raise the level of equity volatility overall.

Spurred by speculative retail fever, the smallest options traders are making record bullish bets, with volumes running 20% higher than last summer, according to Sundial Capital Research. In the latest frenzy, a record 1 million GameStop Corp. call options were purchased on Friday, followed by another 500,000 contracts on Monday.

Dealers who have sold these calls may buy index implied volatility to hedge themselves — adding upward pressure on the VIX.

Something like this was at work back in August and September, when stocks and volatility moved in tandem.

Read More: Playing With Volatility? Get to Know ‘The Greeks’: QuickTake

Since the VIX is calculated using prices of both puts and calls, when prices rise sharply for the latter, it can push up the index in the same way hedging demand can.

In short, demand for both single-name and index calls may be driving the VIX higher in what’s become more an expression of greed than the traditional signal of fear.

“There’s been a lot of call buying, not just on the index but on single stocks,” said Michael Purves, a strategist and founder of Tallbacken Capital Advisors. “And that has been one of the reasons why the VIX has been elevated.”

Shortage of Shorts

Implied volatility moves on options supply and demand, and since last year’s Covid crash a reliable source of the former has gone missing from markets.

Prior to March 2020, institutional investors sold options en masse as a way to generate income in a low-yield world to take advantage of the volatility risk premium, or the tendency of traders to demand higher compensation for future uncertainty compared with what actually comes to pass.

After many of these players bailed on that trade, there’s less selling pressure. And that means the elevated fear gauge has a lot to do with market technicals and less about the pandemic-driven business cycle.

“A lot of short-volatility guys got destroyed in March,” said Purves. “People are still very nervous to sell it.”

Comments - Please login in order to comment.