(Image: Adobe Stock)

(Image: Adobe Stock) It’s certainly been a year like no other and, although there is light at the end of the tunnel, with the rollout of vaccines gaining momentum, there is still some way to go before forecasts about an economic rebound can be made with any certainty.

As such, the alphabet soup of possible recoveries is notably absent from most 2021 outlooks published so far. Instead, themes include the OECD’s “Turning Hope into Reality” December 2020 Economic Outlook and UBS’s “A Year of Renewal”, with annual predictions of growth rates of between 4% and 5% for the global economy, but a wide range of likely performance anticipated across emerging and developed economies.

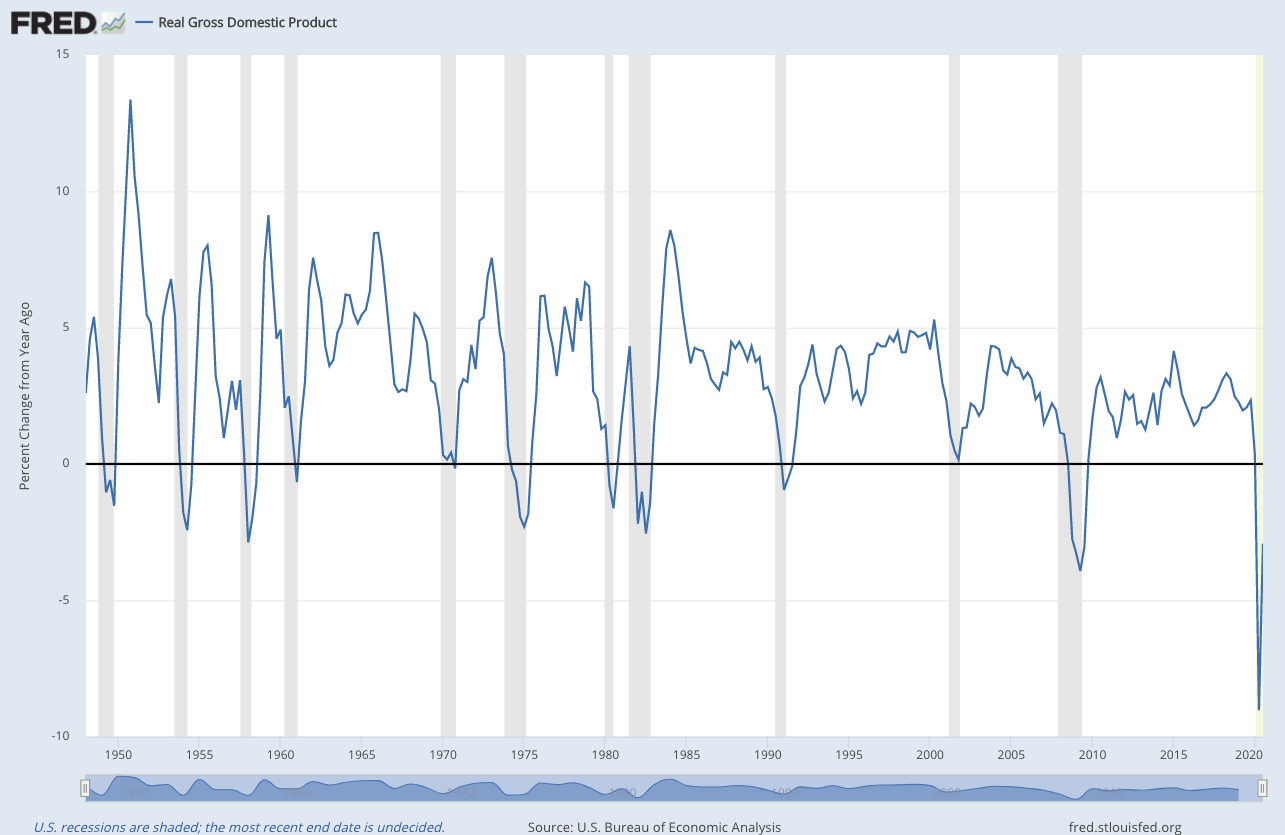

Even after the recovery in the wake of the first wave of infections and associated lockdowns, economies are still in a bigger hole than they were during the Great Recession — 2020 is set to be among the worst years for the global economy in more than 70 years, points out UBS. As such, it will inevitably take some time to reach even 2019 levels. The graph below highlights a longer-term perspective of US growth and highlights how deeply the economy was affected by the sudden stops in the second quarter.

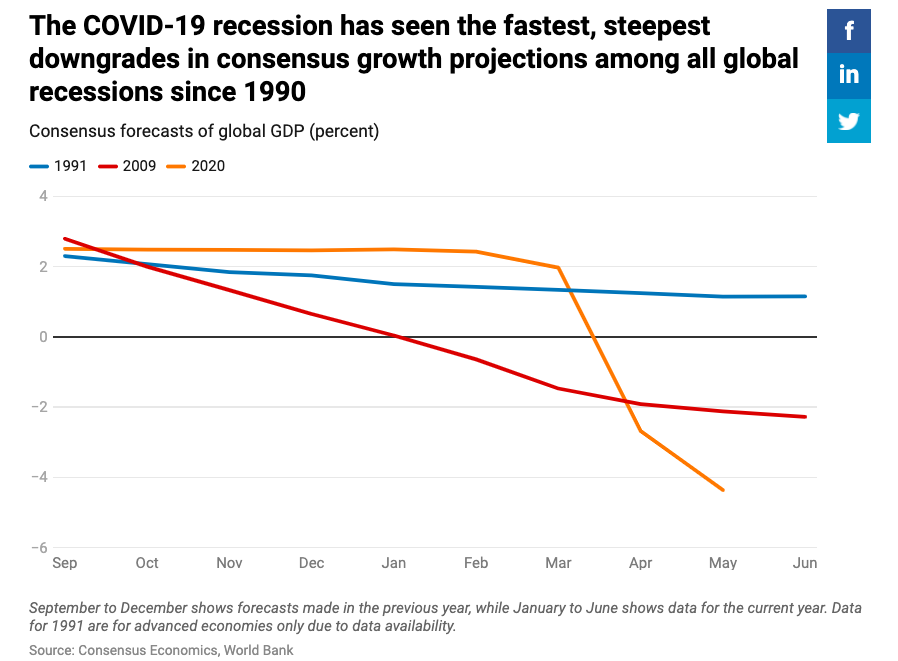

The rapidity of the economic downfall is also reflected in the graph below, which shows that the consensus growth downgrades were the fastest and steepest of all global recessions in the past three decades.

While the initial bounceback across most indicators was equally sharp, the OECD confirms that initial recovery has been easing off, especially in Europe, where, the organisation says, output may be declining again. As the graphs below show, daily measures of mobility have begun to turn down again in the developed world economies as containment measures have been necessitated in the face of renewed virus surges.

Notwithstanding a flatter trajectory in economic activity in the third quarter from the May nadir (see graph B), OECD notes that for the economies that have monthly figures, two thirds of the decline in output between January and April had been restored by September.

Meanwhile, global retail sales had managed to move above 2019 levels, while global industrial production had too, but OECD industrial production remained a few percentage points away from the 2019 production levels (see graph D below).

/file/dailymaverick/wp-content/uploads/BM-Sharon-oped-economicRevival-graph-3.jpg "Note: Panel A and Panel B are PPP-weighted averages. Data for China are not available for Panel A. Countries included in Panel B are Argentina, Brazil, Canada, Chile, Colombia, Finland, Japan, Korea, Mexico, Norway and the United Kingdom. Data in Panel C are for retail sales in the majority of countries, but monthly household consumption is used for the United States and the monthly synthetic consumption indicator is used for Japan.Source: Google LLC, Google Covid-19 Community Mobility Reports, https://www.google.com/covid19/mobility; OECD Main Economic Indicators database; Refinitiv; and OECD calculations.")

In line with the OECD’s caution about the easing off in activity towards the end of the year as a result of reimposed restrictions, Oxford Economics says the global economy will end on a weak note. But it adds that it looks likely to be a relatively mild downturn at a global level.

“Despite the eurozone and UK composite PMIs falling back into recession territory in November,” it explains, “the global composite PMI barely fell, reflecting improvements in the US and elsewhere.”

OECD foresees a brighter outlook for 2021, but cautions that the recovery will be gradual. It anticipates a 4.2% growth in the OECD countries, versus a 4.2% decline in 2020.

Much will hinge on the known unknown — the success of the vaccines in taking the world closer to the light at the end of the tunnel. Based on a faster vaccine rollout than initially envisaged, Oxford Economics has raised its world GDP growth forecast to 5.2% from 4.9% versus 2020’s anticipated 4% decline.

UBS expects global economic output and corporate earnings to reach pre-pandemic levels by the end of 2021. “We think China will be the only large economy to record any growth, and estimate the US economy will have shrunk by roughly 4%, with developed markets as a whole and emerging markets ex-China contracting by 5%-6%.” Slightly fewer than half of the respondents to its Investor Sentiment Survey were very or somewhat optimistic about the global economic outlook over the next year, but on a five-year view that number rose to two-thirds.

UBS is confident that vaccines will be widely available by the second quarter of 2021 and says this will be good news for Europe and the US, which will get back on the path to a sustained recovery.

Oxford Economics says that if the rollout of the vaccines enables “a meaningful and sustained lifting of restrictions” around March/April, a year after the pandemic set in, there could well be a mid-year mini-boom for advanced economies.

Most emerging markets, however, are likely to see a slower vaccine rollout and thus recovery is likely to be further out and milder. But on a positive note, Oxford Economics says emerging markets could benefit from stronger demand from advanced economies, rising commodity prices and the ongoing weakening of the US dollar.

As for South Africa, the OECD expects GDP to contract by 8.1% in 2020 — in line with local expectations — and should increase by 3.1% in 2021 and 2.5% in 2022. It says: “An early and long lockdown to tackle the virus outbreak led to a significant decrease in economic activity in the first half of 2020. A substantial rebound is expected in the second half of the year, driven by high demand and favourable prices for South Africa’s exports.”

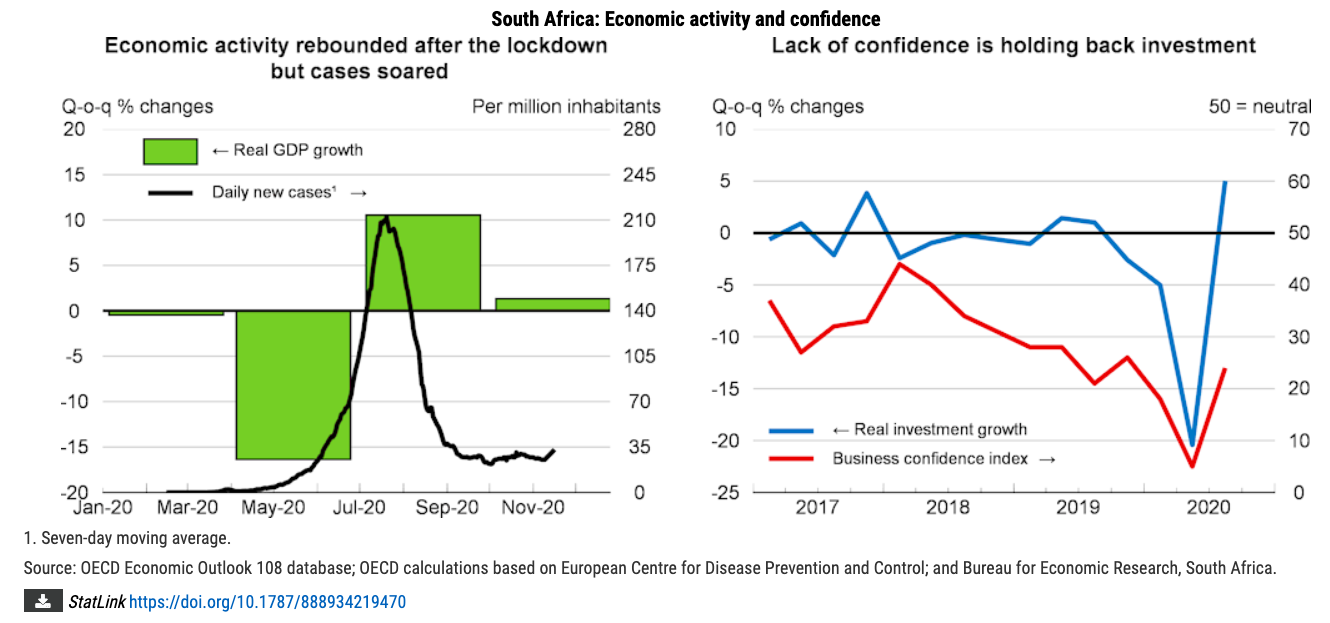

The graph below shows the rebound in growth that coincided with a rise in the number of Covid cases after Level 5 lockdowns were eased. The organisation adds that short-term growth in South Africa is likely to remain modest in the face of lacklustre domestic demand and high unemployment.

The OECD’s prognosis was formulated before the second wave of infections set in, but the organisation does mention the risks of another outbreak given the reduced fiscal policy space the government has to react.

On the policy front, the OECD sees low inflation as likely to allow the SA Reserve Bank to reduce interest rates further. On the fiscal front, it sees the government’s recent moves “to launch the auction of telecom spectrum and procure renewable energy from independent power producers” as positive signals for business leaders and says, if successfully concluded, could lift the confidence that is currently holding back investment (see graph below).

In addition, the OECD notes: “Advancing structural reforms in network sectors, restructuring state-owned enterprises and boosting infrastructure investment could restore growth momentum.”

The length of the tunnel every country is travelling through is still pretty much unknown and, at times, the lights may disappear when there is a twist or turn. However, if some of these projections are right and a large part of the world does, indeed, see the beginning of a sustainable recovery a year after the initial Covid crash occurred, looking back, this unrivalled event will begin to look like a nasty blip on the radar. BM/DM