A medical staff member holds a phial of the Pfizer/BioNTech Covid-19 vaccine jab at Guy's Hospital in London, Britain, 8 December 2020. (Photo: EPA-EFE / Victoria Jones / Pool)

A medical staff member holds a phial of the Pfizer/BioNTech Covid-19 vaccine jab at Guy's Hospital in London, Britain, 8 December 2020. (Photo: EPA-EFE / Victoria Jones / Pool) With 2021 just around the corner and the UK starting to roll out the Pfizer BioNTech vaccine this week, optimism and expectations are mounting that next year will be completely different from this exceptionally trying one.

Covid-19 brought the world to its knees this year and it is herd immunity that will allow economies to stand tall again. Without it, economies won’t be able to rebound to their full potential and will face the prospect of periodic shutdowns should infection rates get out of control again.

So it’s not really surprising that stock market responses to the news of how effective Pfizer’s vaccine had been in the trials have been so outsized.

The graph below shows the rally in stocks in the different regions after the announcement, with Europe playing catch-up to the US stock market after the S&P 500’s record-beating rally this year to date.

However, the road ahead is still fraught with known and unknown challenges. Here are two of the critical known unknowns that we will all need to keep a careful eye on after taking a well-deserved – hopefully uneventful – break into the New Year.

Navigating the uncharted road towards achieving herd immunity

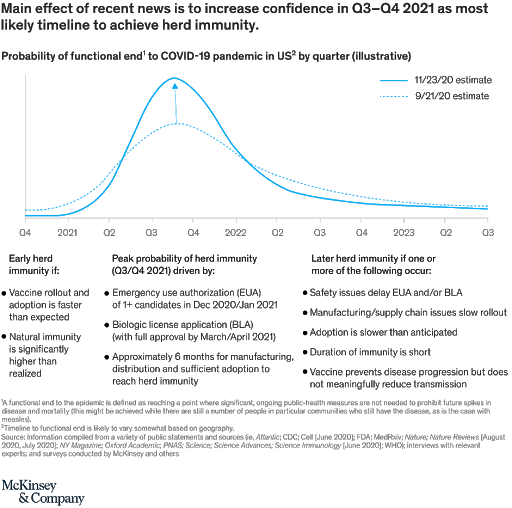

The biggest unknown we face in 2021 is addressed by McKinsey in a recent report titled: “When will the Covid-19 pandemic end?”

To assess this, it starts by specifying the critical factors that, if not achieved, are likely to derail the more optimistic time frames towards achieving herd immunity.

“These include the long-term safety, timely and effective distribution of the vaccine, the vaccine acceptance by the population, and the duration of immunity.”

The graphic below paints an optimistic timeline, with herd immunity achieved in the third or fourth quarter next year. Others don’t expect this to be achieved until 2022.

McKinsey spells out what would be needed to achieve this peak probability scenario below, namely emergency US authorisation in December 2020/January 2021, which is doable by all accounts as the US FDA is expected to give the go-ahead around December 15.

It also premises this outcome on sufficient adoption to reach herd immunity. This is arguably the most critical factor because initial indications are that some 50% of the population have indicated they will not be willing to take the vaccine, particularly in the US where Covid-19 denialists, spurred on by Trump, are many.

McKinsey points out another critical unknown: what impact vaccines will have on transmission rates.

Yes, tests have shown remarkably high levels of effectiveness in “reducing virologically confirmed, symptomatic disease among individuals”. So we are on a good wicket when it comes to the proportion of people who take the vaccine and are less likely to get sick.

But we don’t know how many of those who are vaccinated will continue to transmit the virus to others.

That has implications for the proportion of the population who will need to have had the vaccine if herd immunity is to be reached at all.

According to McKinsey: “If vaccines are only 75% effective at reducing transmission, then coverage of about 60% to 80% of the population will be needed for herd immunity. And if a vaccine is only 50% effective at reducing transmission, coverage of over 90% would be required.”

Taking just these factors into consideration, it is evident that the road ahead to the much-vaunted herd immunity is not likely to be smooth sailing.

Combatting the virus means inflation is likely to reappear

Should we indeed achieve anything close to herd immunity in the next year, the threat of inflation will become more prevalent.

With demand suppressed by the pandemic and the lockdowns that have come with it, concerns about inflation appearing after the biggest fiscal and monetary stimulus packages ever have not yet materialised.

However, removing Covid-19 from the economic mix will herald what Investec Wealth and Investment head of research John Haynes describes as a regime change.

Not only does inflation have a profound effect on the real economy, but it also plays a primary role in pricing fixed income assets, which, says Haynes, also drive the valuation of the riskier asset classes. Thus, he says, “the inflation regime is fundamental to portfolio returns.

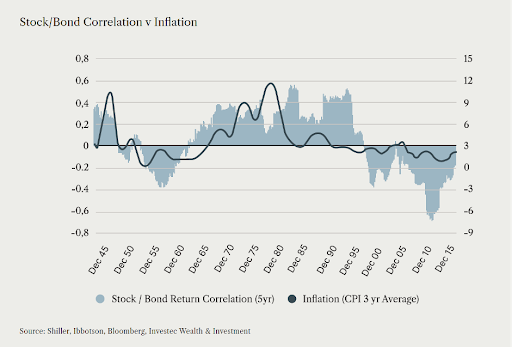

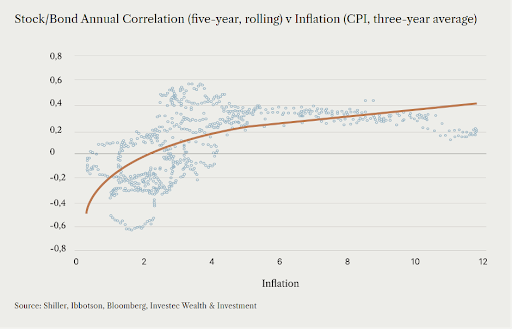

In the graph below, the five-year correlation between US equities and Treasury bond nominal returns is plotted against a smoother measure of inflation.

“This shows clearly that the negative correlation between equity and bond returns, evident since the end of the millennium, has been unusually prolonged and pronounced,” says Haynes.

The explanation put forward is that these asset classes are negatively correlated because of inflation, and that, “if history is the guide, bond and equity returns will become positively correlated once again if inflation moves above 3%”.

Why does this matter?

Haynes explains that a relatively modest rise in inflation could see portfolio volatility materially increase. This contrasts with the recent history, where the negative correlation between equity and bond returns has been “profoundly helpful to multi-asset investors in dampening the volatility of their investment experience, without damaging returns”.

Why does this matter? The negative correlation between equity and bond returns has been profoundly helpful to multi-asset investors in dampening the volatility of their investment experience, without damaging returns.

Investors should be aware that even if the outlook for returns is acceptable, all else being equal, a relatively modest rise in inflation would probably see portfolio volatility increase materially.

Morgan Stanley, in its 2021 Global Economic Outlook, also pinpoints an inflation regime change as one of three key factors that will characterise the next stage of the global recovery.

Says Chetan Ahya, Morgan Stanley's chief economist: “Every recession leaves its mark and the Covid recession will, as well – with the return of inflation.”

Why? She says the stimulus policies put in place to do whatever it takes to create jobs and return employment to pre-Covid levels as quickly as possible will eventually put upward pressure on wages, lifting inflation.

Put simply, the pandemic has caused an unemployment spike to levels not seen in generations, and policymakers are expected to do whatever it takes to create jobs and return employment to pre-Covid levels as quickly as possible – even as economic output improves.

Those stimulus policies will eventually pressure wages upward, lifting inflation.

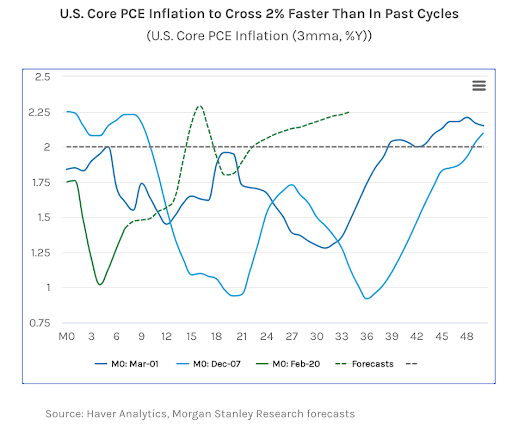

In the graph below, Morgan Stanley illustrates the path it expects inflation in the US to follow back above 2% – just over a year compared to three times as long after the 2001 and 2007 crises.

She adds that the reflationary policies that have been put in place will have key implications for global growth, particularly emerging markets, because the change in regime “will, in turn, drive US dollar weakness and ultimately set the scene for a reflationary impulse for the rest of the world”.

Investec Research Institute chair, Brian Kantor, is more sanguine in his assessment of the impact the central bank stimulus programmes will have on inflation.

He does not expect the extra money created to help the economies recover from economic lockdowns in 2020 to be inflationary, “initially because the demand of the banks to hold extra cash reserves is expected to increase similarly in line with the extra supplies, and over the longer term because monetary policy will in good time reverse direction should such a reversal be called for”.

However, his outlook critically doesn’t include the impact massive fiscal stimulus programmes will have on the economy and inflation.

Together, the trillions of dollars released into the Covid-19 2020 economy will likely prove to take a lot longer to reverse, particularly if the journey towards a pandemic-free world takes longer than we think – and proves to be more of a U- than V-shaped recovery next year.

Looking ahead to 2021, some of the same themes that have commanded so much attention this year will do so again next year, namely the likelihood of inflation returning, whether economies are going to experience a V- or U-shaped recovery and, of course, when we can expect to see the end of the pandemic.

The difference next year, however, is that we won’t be blindsided by these, and other, now known unknowns. BM/DM