Illustrative image | Source: Finance Minister Tito Mboweni. (Photo: EPA-EFE/NIC BOTHMA) | Leila Dougan

Illustrative image | Source: Finance Minister Tito Mboweni. (Photo: EPA-EFE/NIC BOTHMA) | Leila Dougan Most responses to the Medium Term Budget Policy Statement (MTBPS) tabled by Minister of Finance Tito Mboweni have focused on the explosive trajectory of SA’s sovereign debt. However, the most alarming sentence in the whole document was the Treasury’s assessment that, “based on current projections output [GDP], is only expected to return to pre-pandemic levels in 2024.”

Think about what this means for a moment.

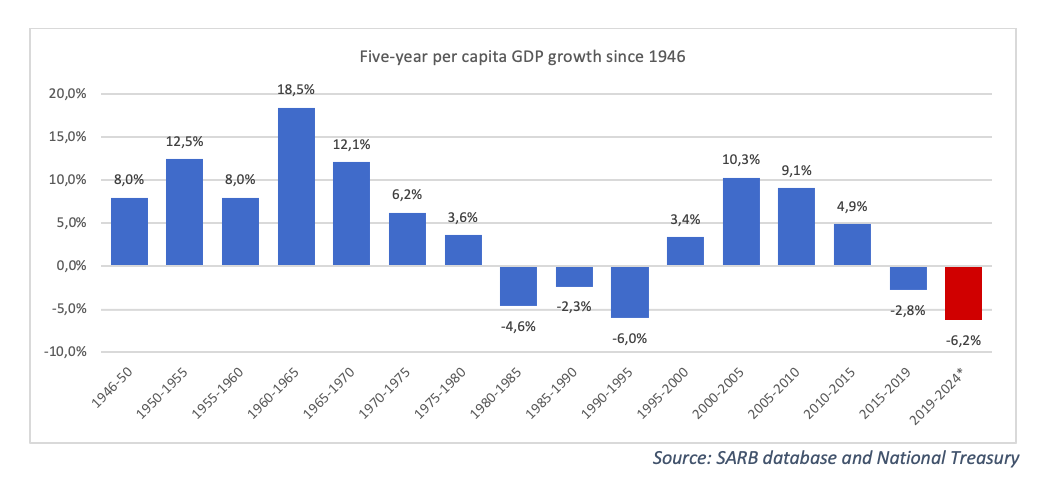

By mid-2024, the population will be some 6% larger than it was in 2019, so per capita income will be lower by that amount (see chart). Employment levels will also be lower: employment growth (especially in the formal sector) is always slower than economic growth, so the “rebound” of GDP to 2019 levels won’t be accompanied by a return to 2019 levels of employment. And in 2019 South Africa already had the world’s deepest unemployment crisis – with some 10.3 million unemployed. That catastrophic number will be larger in 2024.

Lower levels of employment in 2024 mean that poverty will rise even more than would be implied by the 6% decline in per capita income and that income inequality will rise yet further. They also mean fewer people paying personal income tax, implying an even greater burden on the few who do.

Lower levels of employment in 2024 mean that poverty will rise even more than would be implied by the 6% decline in per capita income and that income inequality will rise yet further. They also mean fewer people paying personal income tax, implying an even greater burden on the few who do.

These are appalling outcomes. And they could be even worse: Treasury’s predictions for economic growth have, over the past decade, consistently erred in being too optimistic. If that happens again, then we will not hit 2019 levels of GDP until some time after 2024.

The sheer horror of all of this has been obscured by the focus on Treasury’s projections regarding the debt trajectory, which it now says will peak at over 95% of GDP in 2025/26 (again, dependent on SA’s economy growing at the rates Treasury has pencilled in).

At this level of debt, a county has very little margin for error, particularly when the rate of economic growth is lower than the rate of interest government pays on its outstanding debt. In these circumstances, the only way to stabilise debt levels is to run a substantial primary surplus. This means that non-interest spending must be considerably lower than taxes collected. Politically, this is extremely challenging, especially when voters are increasingly impoverished.

The critical link between the dire socioeconomic outcomes and our exploding debt trajectory and all the pain that entails is the catastrophic collapse in economic growth over the last decade. Growth is now at levels not seen since the dying days of apartheid, a time, not coincidentally, when our public finances were last in a crisis comparable to the one we face today.

The Centre for Development and Enterprise has long argued that the fiscal crisis we face is at least as much a problem of slow growth as it is of over-spending. We have also argued that the disconnect between the slow rate at which the economy has grown and the fast rate at which public spending has grown over the last decade has itself helped slow what growth we have seen because it has increased risk and the cost of capital.

Having said that, the underlying reason for the rise in debt as well as for the slowdown in growth is the same: the complete collapse of standards of governance.

Governance always matters for how growth transmits itself into rising living standards. Better governed societies tend to have much more inclusive growth processes than poorly governed societies. This is true whatever the current level of income in a society. But once a society has achieved middle-income status, the quality of governance becomes more and more important to growth processes, and not just to whether growth is inclusive or not.

The main reason for this is that the richer a country is, the more economic growth depends on productivity growth and innovation rather than on brute-force methods of growth through extracting more natural resources or accumulating ever larger stocks of physical capital.

Productivity growth is a fundamentally social process that works best when institutions and policies are stable, when authorities’ decisions are predictable and rational, when the rule of law prevents government dispossessing its citizens of their assets, and when individuals, firms and investors have a measure of confidence in the country’s future.

Seen from this perspective, the collapse of governance in SA over the past 15 years represents a massive shock to the country’s productive capacity. This is most evident in the state-owned companies (Eskom, being only the most egregious example), but these are just symptoms of wider rot.

There is no easy answer to SA’s many challenges. What is clear is that if the Treasury is right and GDP will not return to 2019 levels until 2024, we are set for a very miserable decade. To avoid this fate we need a much more plausible growth strategy, one that is not over-reliant on the fantasy that our state is capable and that the route out of the disaster is to expand it.

Nor is the rot “merely” a question of corruption. The quality of governance is not defined exclusively by the presence or absence of corruption, but also by the predictability and efficiency of decision-making by bureaucrats and policy-makers, by stability in policy, and by the degree to which politics is driven by those who wish to see long-term prosperity or by those who wish to deliver short-term sugar highs to their constituencies.

Along all of these dimensions, SA is a worse-governed society today than it was 15 years ago. It is true that under President Cyril Ramaphosa, there has been some improvement in some dimensions. But this has been too limited where it has happened and it is offset by worsening uncertainty elsewhere (land reform, proposals to nationalise the Reserve Bank). Nor is there any guarantee that SA will not return to outright looting at some point in the near future.

More broadly, the whole notion of a developmental state has proved itself to be a hollow one. But government, bizarrely obsessed with trying to save SAA, simply refuses to recognise this reality.

These are not propitious conditions for growth. We have long been worried that government’s policy-making capacity has been weakened and overwhelmed, that the Cabinet does not function well, and that it is ill-served by senior levels of the bureaucracy. With the best will in the world, no-one who reads the full version of the economic recovery plan released two weeks ago would have any confidence whatever that the team responsible for getting us out of this mess has the capacity to do so.

Not that the answers are easy. We are in such a deep hole that no one can confidently assert that her strategy will generate growth in the short term. What we do know is that SA needs a much more effective Cabinet and senior levels of the civil service, a much greater role for the private sector throughout the economy, and considerably more honesty about what has gone wrong as the first step to adopting the right reforms and rebuilding. In the short term, however, investors are super-wary, and government doesn’t have the fiscal headroom to spark a growth acceleration. Worse, if the fiscal space did exist, there would be every reason to worry that funding would be badly spent or simply stolen, leaving SA worse off than if nothing had been done.

Having said that, we cannot expect a return to growth without a capable state. The private sector will not drive a growth acceleration if the rules of the game are not clearer and more efficiently complied with and enforced. In the context of a weak state, what is needed is that it focus much more clearly and much more effectively on a narrower range of activities and make sure that it does them well. The worst-case scenario is the one we have now: a weak state that is over-ambitious.

There is no easy answer to SA’s many challenges. What is clear is that if the Treasury is right and GDP will not return to 2019 levels until 2024, we are set for a very miserable decade. To avoid this fate we need a much more plausible growth strategy, one that is not over-reliant on the fantasy that our state is capable and that the route out of the disaster is to expand it.

It is in all of our interests, the ruling party’s included, to get this right, if only because something else is going to happen in 2024: we are going to have another general election. DM

Ann Bernstein is executive director of the Centre for Development and Enterprise.

Comments

Scroll down to load comments...