“As was the case last year, only 6% of respondents felt comfortable with their retirement prospects,” said Eddy.

These results are based on findings of the 2020 Brand Atlas Survey, which tracks and measures the lifestyles of the 15.1 million economically active South Africans. The data are weighted to reflect the profile of this universe as defined by Unisa’s Bureau of Marketing Research in their 2019 Household Income and Expenditure report. The data in the report includes the early effects of Covid-19.

Unsurprisingly, the poor prospective outcomes are partly down to economic hardship: it is simply impossible to save without a minimum level of income. More than half the respondents in the survey indicated severe financial stress.

It is not only an income issue though, says Eddy, who notes that people in the low, medium and high-income brackets are equally worried about making ends meet in retirement.

Rather, he says, it is a savings problem that is rooted in the widespread lack of engagement around retirement planning, which manifests as financial ignorance and ill-discipline.

As Winston Churchill once remarked, plans are worthless, but planning is essential. A total of 49% of respondents admit they have no plan, only 6% believe they are carefully executing a thought-through plan.

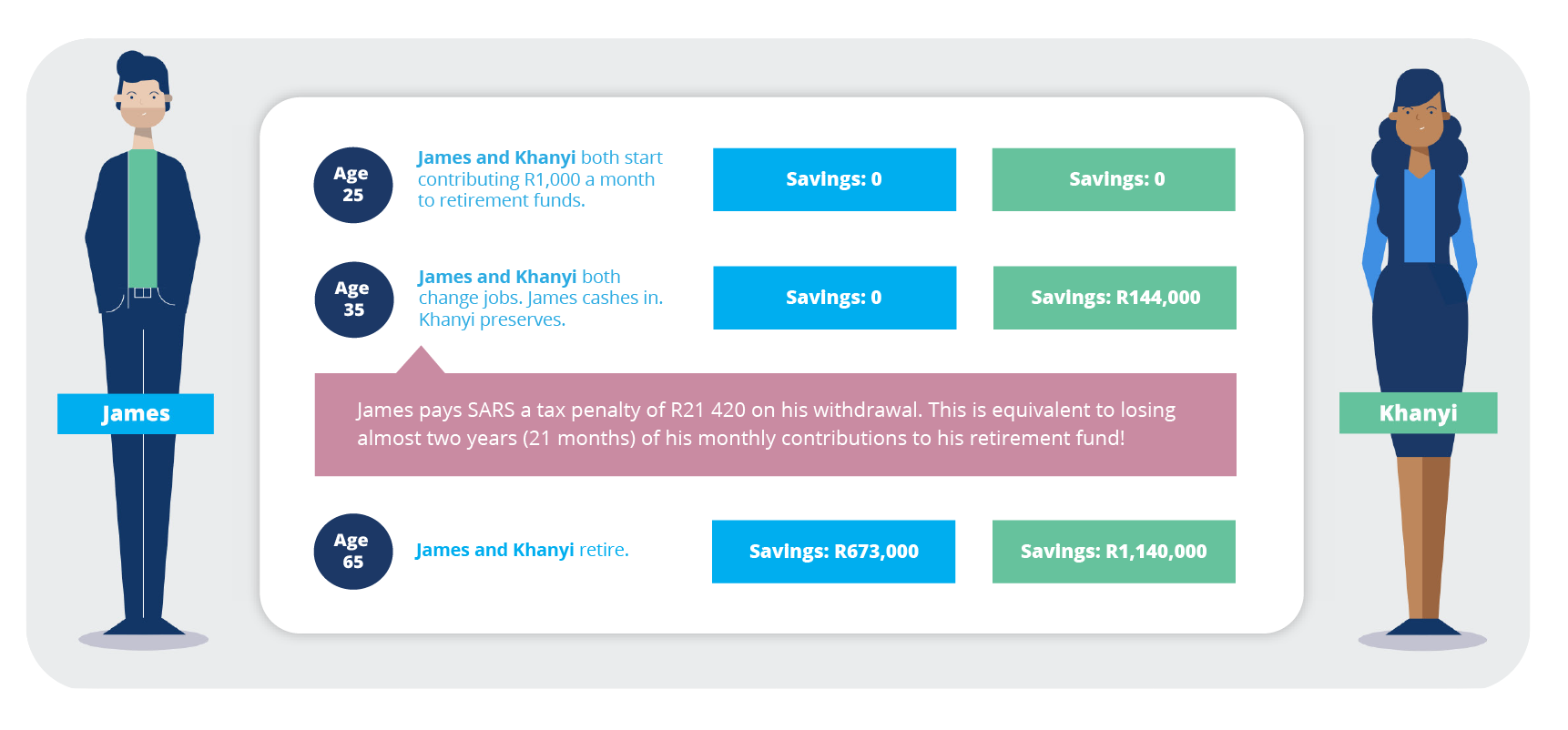

A total of 40% of respondents believe their retirement can be funded within 25 years, “seemingly unaware that long-term compounding returns are essential to achieving a comfortable retirement”. This helps explain why more than 60% of respondents cash in their corporate fund on leaving their employer. And why, for almost 30% of respondents, saving for retirement is just not a priority at this stage, as though they can make it up later.

Realistically, they cannot. Eddy explains that a savings plan that delivers a 60% income replacement ratio after 40 years would replace only 30% of final income after 25 years. One would have to save twice as much – “requiring a large, and improbable, cut-back to an accustomed lifestyle” – to make up the shortfall.

Along similar lines, 40% of respondents younger than 35 expect to retire before age 60, ignoring that retiring early not only cuts into their saving years, but also adds to the years those savings must last.

“These are all illusions that some timeous retirement planning (or basic financial education) early on in their working life would quickly dispel.”

But, he says, the preferred route seems to be to have those illusions shattered by reality.

Much of this disconnect would be cleared up if people engaged with one of the many financial tools and calculators freely available online. These tools are designed to help individuals understand how the decisions they make today – such as their saving rate or whether or not they cash in their pension fund when they change jobs –will impact their retirement outcome.

Little can be done to rectify a retirement shortfall in later life, besides working longer and readjusting expectations. But much can be done to educate younger people on what it takes to achieve a comfortable retirement. It starts with some basic long-term planning, and continues with appropriate follow-through and modest, but ongoing, engagement, to monitor progress. DM/BM

10X Investments’ South African Retirement Reality Report 2020 is available for download here