BUSINESS MAVERICK ANALYSIS

The economic future: Inflation, Deflation or Stagflation?

Financial markets are starting to price in the prospect of inflation, but deflation still remains a risk and the outside view is that we may be heading for stagflation. There are likely to be many surprises along the way before we are able to make a definitive call on which of the greater evils, if any, is most likely.

Unexpected increases in inflation in the US and the UK, along with a record high nominal gold price, have put the prospect of inflation – and, for some, even stagflation – back on the table for economists, market analysts and central banks.

Inflation, deflation or stagflation are all undesirable economic outcomes. Inflation exacerbates income inequality, deflation is the product of an economy caught in quicksand and is hard to get rid of and stagflation is the particularly toxic combination of a stagnant economy and rising prices.

The generally accepted “ideal” inflation rate is considered to be an annual increase in consumer prices that is just enough to reflect a growing economy but not enough to put pressure on low-income earnings and exacerbate already gaping social inequalities. For the advanced economies, that’s about 2% and for South Africa, it’s mandated to be anywhere between 3% and 6%, given the dollar-rand differential.

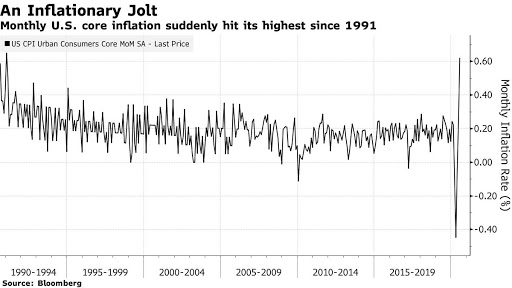

Disinflation has predominated for some time in the advanced economies, particularly the US and Japan. The pandemic and economic sudden stops raised the threat level to deflation. However, this concern was, to an extent, alleviated when US inflation data for July came out ahead of expectations. The US consumer price index rose 0.6% month on month, higher than an expected 0.4% increase, translating into a year-on-year increase in prices of 1% – a four-month high.

The rise in the core inflation rate was even more significant, as highlighted in the graph below, with the measure of inflation that excludes food and energy experiencing its largest increase since 1991. Recovering oil prices contributed about 25% to the monthly increase in the core inflation rate. Other categories that increased included goods that benefit from a reprieve from the lockdowns: rents, new and used vehicles and apparel.

Although a surprise, the rate of inflation remains half the US Federal Reserve’s target rate of 2%, a level last seen in February this year before the coronavirus crisis hit. For that reason, the threat of deflation continues to hang over the short- to medium-term outlook notwithstanding the trillions of dollars of central bank money that has been released into the economy. It seems all that money may have been let loose in the financial system but it’s not being put to good use, with the money supply skyrocketing but the velocity of money still mired in anaemic consumer demand.

The unprecedented and unpredictable nature of the pandemic arguably makes it a foolish endeavour to bet on the future of inflation based on a single data point. The July inflation rate largely reflects an economy coming out of lockdown and a perception that the Covid-19 risks were waning. August may well prove otherwise, with a still worrying uphill climb in infections reintroducing widespread uncertainty, economic disruptions and, in all likelihood, less scope for price increases to feed through to the next US inflation number.

Predicting the inflation rate may well become slightly less of a guessing game after the Fed meets virtually this week for its annual Jackson Hole monetary policy symposium retreat. The most-anticipated outcome of the meeting is expected to be a change in the US central bank’s monetary policy framework, which could see the Fed target an average inflation rate of 2% going forward.

The significance of targeting an average, versus a fixed percentage in the inflation rate is that the central bank will have more flexibility as to when, and how quickly, it reduces or increases interest rates when inflation under- or overshoots the desired rate.

At home, SA Reserve Bank Governor Lesetja Kganyago continues to stand firm on maintaining the central bank’s existing mandate: to achieve and maintain price stability to protect the value of the rand and in the interest of balanced and sustainable economic growth.

In a recent address at the University of Pretoria, titled “In the shadow of COVID: lessons from 20 years of inflation targeting”, the governor reminded the audience that inflation targeting was “responsible for a long period of price stability and should be considered a success for South Africa and for many other countries”.

He asserted: “Even now, at this very difficult time for the economy, we can see the inflation-targeting framework functioning properly, delivering historically low interest rates in the context of low inflation. With inflation well anchored, moves to lower interest rates should get us more real growth than inflation. And this is exactly where we are now.”

Kganyago addressed what he says is a common argument: that lower inflation has been a global phenomenon and thus “not an accomplishment of inflation targeting”.

“Low inflation is not just a worldwide fact that countries can have ‘for free’. If individual countries don’t make an effort, they can easily get stuck with high inflation,” he warned.

Where does he sit on the deflation versus inflation continuum? According to Kganyago, “While inflation has eased and created space for lower rates, I am not aware of any professional analyst who project deflation in South Africa. Our own SARB forecasts are in line with this consensus.”

He adds that if deflation were to take root, the bank would deploy all the tools at its disposal to maintain inflation in its 3% to 6% target range.

“Our inflation-targeting framework would help us make that decision, and would underpin the credibility of any steps we might need to take.”

Kganyago acknowledges that inflation targeting is facing “large challenges” in advanced economies, with inflation consistently undershooting central bank targets for years, notwithstanding aggressive monetary policies. The possible explanations he puts forward include changes in labour markets or demographics; debt pulling down inflation and interest rates permanently or, alternatively, low interest rates encouraging financial risk-taking, resulting in a vicious cycle of bubbles, crises, low economic growth and falling inflation.

Fortunately, he doesn’t believe South Africa has these problems “yet”. Why? “Right now, we don’t have the high inflation and high interest rates of the past, but we also don’t have the zero rates and close-to-zero inflation of the rich countries. The inflation-targeting paradigm is working pretty well.”

Investec chief economist Annabel Bishop doesn’t see inflation and oil prices as likely to experience a sharp upwards trend this year because she expects the global economic recovery to be slow and uneven, “battling against headwinds of weak demand, depressed appetite for fixed investment and damaged labour markets, with unemployment unlikely to jump substantially lower, while fiscal stimulus wears down.”

However, she foresees higher oil prices next year contributing to higher inflation domestically and globally, “with market exuberance on recovery likely at times, and a strengthening in the global economic recovery over 2021 expected, as activity becomes more even, and the global recovery itself more synchronised between economies”.

A synchronised global recovery with inflation under control currently feels like an economic nirvana and way out of reach. But just as consumer inflation data in the US and UK surprised on the upside, there are likely to be many more surprises along the way before we are able to answer the question with confidence: inflation, deflation or stagflation? BM/DM