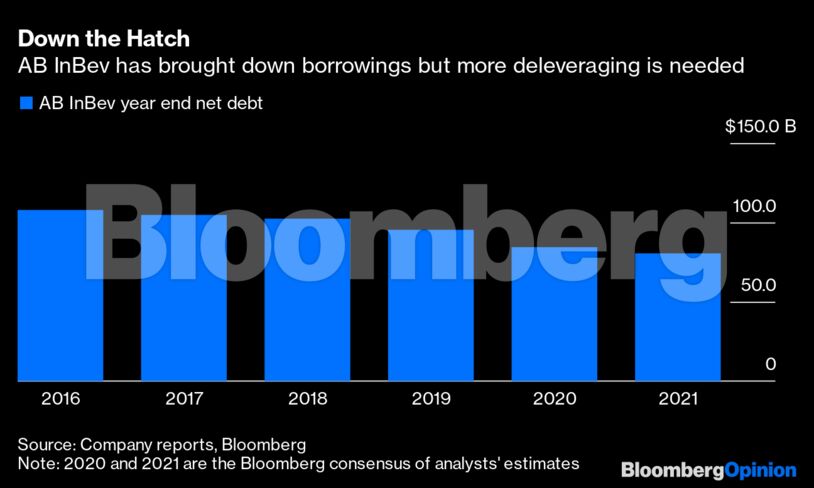

Even with this brighter picture, the so-called Megabrew still needs to tackle its mega debt, which stood at $87.4 billion at the end of June — 4.9 times its earnings before interest, tax, depreciation and amortization.

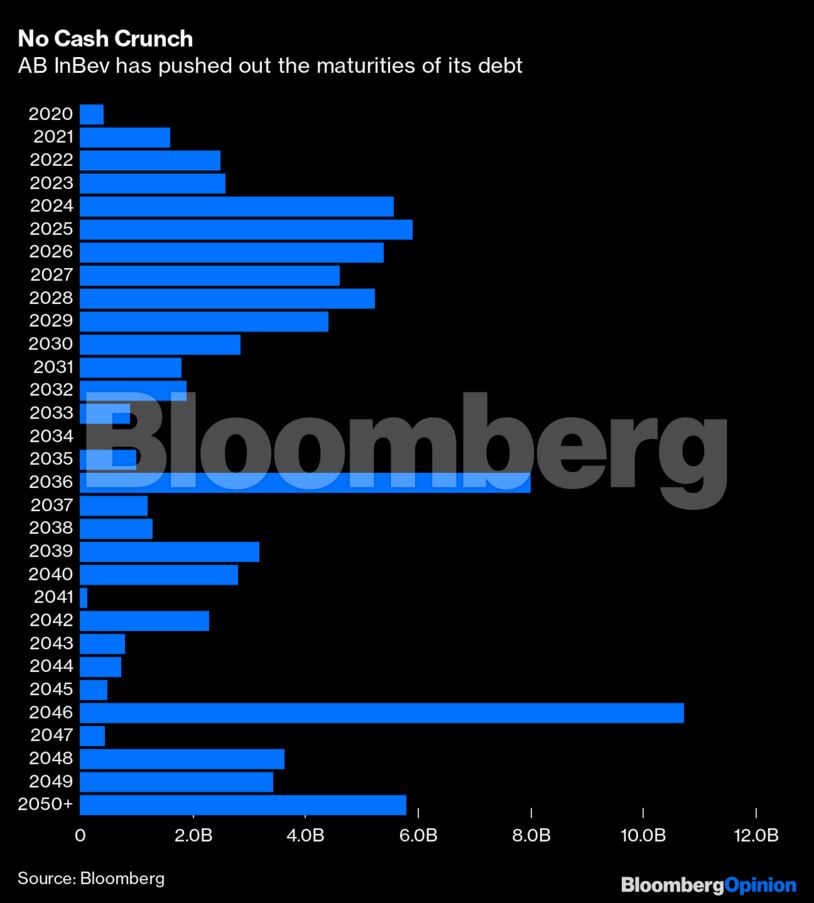

AB InBev has done a decent job of cutting its borrowings from more than $100 billion since purchasing SABMiller in 2016. It has refinanced to take advantage of favorable interest rates and pushed out the time frame for repaying its bonds. It also repaid its $9 billion revolving credit facility in full in June. As long as it retains an investment-grade credit rating, it should be able to keep managing its debt.

But with earnings being hit in key markets such as the U.S., Mexico and South Africa, the company’s leverage ratio still looks too high.

Luckily, the Belgian multinational has a few levers it can pull, even if some aren’t so palatable.

Eliminating its dividend for 2020 would be the simplest move. This would save about $4 billion over the course of the full year.

The group could sell off some of its stakes in other companies. It still holds 62% of Brazilian brewer Ambev SA and 87% of Budweiser Brewing Co APAC Ltd. Taking both of these down to 51% could raise more than $20 billion at current valuations. It might not be possible to reduce its stake in the Asian business all at once, but if done in stages, it could be helpful.

Another option is to dispose of some of its own divisions, and a couple stand out. Late last year, Reuters reported that AB InBev was looking at a minority stake sale or joint venture for its U.S. canning business. This would be a good move because, assuming the group retains control, it could generate proceeds of $2-3 billion, according to analysts at Jefferies. Another logical divestment would be its business in South Korea, which it had sold in 2009 to KKR & Co. and bought back in 2014. This could generate another $3.7 billion, according to Jefferies.

Combining these corporate actions with foregoing the dividend could generate more than $30 billion. This would reduce borrowings to under $50 billion, and based on the Bloomberg analysts’ estimates of net debt being just over $80 billion at the end of 2021, this would imply a net debt to Ebitda ratio of 2.7 times, a level at which investors would feel more comfortable.

Reassurance on borrowings would also be useful given that AB InBev carries a significant amount of goodwill: $115 billion on its balance sheet as of June 30. A slow recovery or a second virus wave could seriously damage the future cash potential of its brands. On Thursday, the company took a $2.5 billion non-cash impairment on its African business. Duncan Fox of Bloomberg Intelligence says more write-downs can’t be ruled out yet.

AB InBev should get some relief from a weak dollar, which increases the value of its earnings in emerging markets, and an increase in beer volumes in June bodes well for the second half of the year. But with changing drinking habits and the risk of more Covid-19 flare-ups, getting to grips with its debt once and for all should be a priority.