(Photo: Adobestock)

(Photo: Adobestock) Pensioners who beat both Covid-19 and the Zuma-era kleptocracy generally had one thing in common: they had the benefit of a financial adviser to make sure they had a sound and well-considered plan upfront.

Many pensioners who invested the bulk of their invested linked living annuities (living annuities) offshore have found themselves in a stronger position, even when foreign investment markets and the rand were at their worst. The rand dropped by more than foreign investment markets. This meant that both foreign equity and bond markets benefited local investors.

Foreign markets have recovered significantly, but the rand has not recovered by anywhere near as much, placing foreign investments in an even stronger position.

Pensioners on living annuities, particularly those who had less than 5% drawdowns, must be feeling pretty good about what has happened and thankful to their financial advisers.

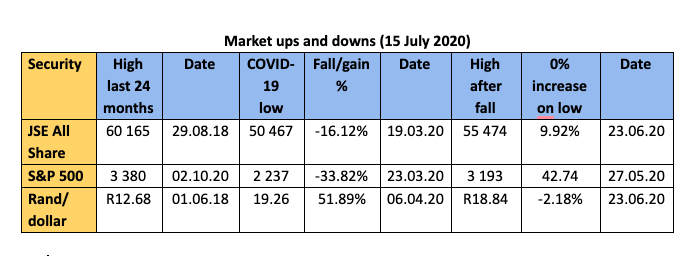

Here is a table to show how markets bounce around. (Graph1)

But this does not mean that those who did not benefit should now rush off and do a major reassessment of their investments. Do a reassessment, but make very considered decisions, particularly with the help of your financial advisers. Three big warnings:

- Don’t rush and sell all your local investments now and invest offshore, or quickly buy and sell or sell any other investment.

- Don’t think the crisis is over or even nearly over (no matter what Trump says). The Covid-19 pandemic has affected markets in entirely new ways. No one really knows the future outcomes. Never before has there been an international shutdown of businesses keeping employees locked up at home that led to a cut or reduced pay.

Many businesses will go bankrupt while others will flourish. There will be a lot of collateral damage to businesses you might expect to survive. Take for example the ban in South Africa on alcohol sales. The biggest threat is to the glass manufacturing businesses which have breweries as a major source of income, who have stopped ordering glass bottles. Everyone is going to have to stay on their guard, even if a Covid-19 vaccine is discovered early, as the fallout will last for a long time.

The biggest question mark is how successful is the relaunch of business, from micro to macro, going to be? Look at it this way. People around the world have lost their jobs or been put on short-time. This means they will buy far less and those with jobs will save a lot more, impacting on the sale of consumer goods and production processes. And with this comes less travel, more working from home and the reduction of fuel sales. Tax income of countries will be down, while the world has reached record levels of debt.

- The impact on yourself: Some pensioners, no matter how rich or poor you may be, can expect other fallouts such as adult children losing their jobs on a lengthy or permanent basis and relying on them for an income. It is worth remembering that prior to the current crisis it was found that five people lived off one state old age grant. There are likely to be a lot more now!

This all shows that even those who have followed the right route may still suffer from both economic fallouts and/or from personal circumstances.

What you must do is:

- Talk to your financial adviser about what the right way forward is for you. There are things that you may need to change to make your income more sustainable in the future. It must be a financial planner who can deal with all your needs – not just your investments. They must understand your tax, estate duty and your other investments. All these mean you must be judged on your financial status from every point of view.

Wouter Fourie, a top-flight financial planner, who is a professional accountant and Certified Financial Planner, a financial planner of the year in 2015/16 and the co-author of our book, The Ultimate Guide to Retirement in South Africa, says financial planning is becoming increasingly valuable. A financial planner’s worth used to be simply based on the adviser’s ability to beat a financial benchmark — and that was never easy.

Fourie says a planner’s value is far better measured by the impact that their services can have on investors’ financial outcomes. New metrics and research findings show that the interpersonal aspect of advice may have more impact on a person’s finances than anything else. This outlook favours services like behavioural coaching—helping you to mitigate your biases and stay the course—and personalised advice versus traditional selling points like maximising returns and asset allocation.

Here is some important backup to the need for advice:

- This metric introduced by two members of data company Morningstar, David Blanchett and Paul Kaplan, measures the additional expected retirement income achieved through wise financial-planning decisions, and many of these decisions are made with an adviser’s assistance. Morningstar’s Gamma research demonstrates that making sound financial planning decisions in five areas — asset allocation, withdrawal strategy, guaranteed income products, tax-efficient allocation, and portfolio optimisation — can generate 29% more income on average for a retiree.

Morningstar research also found that offering clients personalised advice and using a combination of interventions — like increasing someone’s retirement fund contribution rate to 6% and retirement age to 67 — can help 71.2% of households avoid extreme austerity and still have what they need when they retire.

- Vanguard’s Advisor’s Alpha measures the value-added, in basis points, by the seven best practices in wealth management: asset allocation, cost-effective implementation, rebalancing, behavioural coaching, spending strategy, and total-return investing versus income investing. This research suggests that behavioural coaching is the single most impactful thing an adviser can do. As investors, emotions can be our own worst enemy, especially when the markets are volatile and guidance from a financial planner behavioural coach can save us from panic selling and abandoning long-term financial plans.

- You must consider alternatives. It is not as simple as saying don’t transfer to cash. There are things that may be done to improve your years in retirement. The type of things that should be looked at is:

- Switching all or part of your living annuity, particularly to a hybrid annuity, which could make your income more sustainable by using a guaranteed annuity as one of your underlying investments.

- Restructuring your living annuity to one where you only draw from a particular source while others recover. A good thing about a living annuity is that you can switch the underlying living annuities at any time. It is only the drawdown rate that can only be altered on your anniversary date of your living annuity that is apart from the current government exemption allowing you to change during the next four months. Many people draw from all their investment every month. This is worth having a look at.

- Foreign investments. If you are weak in foreign exposure you should look at it again how to structure this.

Investment advisers can be contacted on the following websites: findanadvisor.co.za; or, for the well-qualified Certified Financial Planner accredited by the Financial Planning Institutes on www.letsplan.co.za; or, the South African Independent Financial Advisers Association, which has a special qualification as a Certified Post-Retirement Practitioner on saifaa.co.za, which among other things has a course for helping pensioners. DM

Bruce Cameron, the semi-retired founding editor of Personal Finance of Independent Newspapers, over a number of weeks will look at the state of pensioners and retirement funds, which will highlight research undertaken by Alexander Forbes on retirement income in South Africa. Cameron and Wouter Fourie are co-authors of the best-selling book, The Ultimate Guide to Retirement in South Africa.

Comments

Scroll down to load comments...