A vibrant Chinese economy could be a rising tide that gets South Africa, and other emerging markets, closer to dry land, says the writer. (Photo: Paul Yeung / Bloomberg via Getty Images)

A vibrant Chinese economy could be a rising tide that gets South Africa, and other emerging markets, closer to dry land, says the writer. (Photo: Paul Yeung / Bloomberg via Getty Images) China managed to move relatively quickly through the eye of the Covid-19 storm, enabling it to begin rebuilding its economy and its efforts are starting to pay off as the country is likely to make it back into positive territory when second-quarter growth statistics are published at the end of this week.

While US financial market fortunes tend to sway emerging market sentiment whichever way the wind blows, China has a more fundamental economic influence on the economic fortunes of emerging market economies because of its demand for commodities and increasing contribution to the global economy.

After a near -7% decline in economic growth in the first quarter, when second-quarter GDP figures are released on Friday, the world’s second-largest economy is expected to notch up a positive growth rate of about 2%.

Blackrock Head of Investment Strategy, ETF and Index Investments EMEA, Wei Li notes that manufacturing Purchasing Managers’ Index (PMIs) are back into expansionary territory, internet companies are ramping up their investments and infrastructure investments are boosting productivity. “China is further along in the pandemic cycle and the restart has happened quickly,” she said in a recent webinar on China hosted by Satrix CEO Helena Conradie.

However, services continue to lag for behavioural reasons, she says. The return to non-essential purchases has been muted and weekend travel in China is still lower than before in an indication that consumers are not ready to return to weekend shopping yet.

She notes that the economy is back to 94% of pre-Covid-19 production capacity. However, hotel occupation, flights and subway travel remain depressed. “Consumers are not comfortable and are taking time to get back to normalcy.”

From a longer-term structural perspective, Conradie says the Chinese economy is on an even faster track to become the world’s largest economy, with expectations that it will reach pole position in five to seven years versus the 10 years expected previously. Its contribution to global GDP in 2019 was 33% versus the US’s 40% contribution, she says, adding: “There is no doubt that the engine of growth is shifting towards China.”

In its July 2020 outlook for emerging markets, Lazard Asset Management says China’s economic recovery, which it views as a possible leading indicator of what Western countries may experience, is “somewhat” better than expected, driven by both domestic demand and better-than-expected exports. “While there has been an increase in new infection rates in certain regions of the world, we know the playbook for flattening the curve and we currently do not expect major economies to revert to the large scale and broad-based shutdowns previously experienced.”

What is China doing right to get its economy back on track so quickly?

It helps that China got on top of the virus by cracking down early and getting infections under control. There have been recent flare-ups, but it has also been proactive and decisive in stamping these out.

Another key element of its so far successful rebound is that it has engaged in targeted stimulus measures, unlike some of the advanced economies, which have implemented massive and far-reaching fiscal programmes to get money to hard-hit individuals and companies. The People’s Bank of China recently indicated that it would continue in the same carefully considered vein because it doesn’t want to fuel markets with liquidity.

For that reason, Li believes that the country’s stimulus measures are less likely to propagate across emerging markets because the measures are domestically-focused and thus are less likely to prompt an emerging market-wide bounce.

China is also benefiting from beginning to open its economy to foreigners. In a recent assessment of US-China relations, titled Despite the Rhetoric, US-China financial decoupling is not happening. Peterson Institute for International Economics (PIIE) authors Nicholas Lardy and Tianlei Huang say that “for all the fireworks over tariffs and investment restrictions, China’s integration into global financial markets continues apace”.

In fact, they find that many US financial institutions have taken advantage of China’s recent liberalisation in finance, investing substantial sums in China’s $47-trillion financial services sector. These have included Paypal, Goldman Sachs, JP Morgan, American Express and US credit rating agencies.

Say Lardy and Huang: “Previous restrictions meant that foreign firms have only a tiny slice of most sectors of this market, for example, less than 2% of banking assets and less than 6% of the insurance market.” Now, they have been given the opportunity to compete for greater market shares.

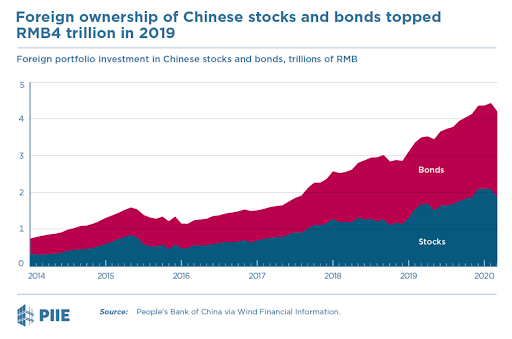

In addition, cross-border capital flows into China have been increasing, according to the PIIE research, both in terms of foreign direct investment and portfolio inflows. The graph below shows the increase in foreign ownership of stocks and bonds, which reached RMB4.2-billion (about $600-million) by the end of the first quarter of 2020.

“This amount is almost certain to grow over time as the US-based financial company MSCI and other major firms that provide global indices driving much institutional investing gradually increase the weight of Chinese listed firms in their indices,” say the authors.

With these tailwinds behind China’s economic turnaround, what are the headwinds the country could potentially face?

Growing authoritarianism and the crackdown in Hong Kong could potentially pose risks, but it’s very difficult to assess the economic effects at this stage.

More immediately, US-China relations are the number one risk to the global economic equilibrium and these are not getting any better. In fact, last week, US President Donald Trump indicated that he was not considering a Phase 2 trade deal.

Blackrock’s Li says frosty tensions between the two superpowers are here to stay, but there is still reason to be cautiously optimistic on the investment outlook for China. The risk of decoupling makes it even more important to hold China as a standalone investment, she adds.

The fact that the Chinese consumer hasn’t yet got back into the driving seat is another potential headwind because consumption is such an important driving force in ensuring a vibrant and sustainable economic recovery. Also, the possibility of a longer-lasting global economic recession as a result of the worrying increases in Covid-19 infection rates in the US, Australia, Brazil and Mexico would not bode well for a Chinese economy that still depends heavily on external sources of revenue.

Should China manage to benefit from the tailwinds it is currently experiencing and successfully navigate the headwinds, its economic rebound could, however, provide the fillip other emerging markets need if they are going to reach their pre-pandemic levels of economic activity. However, China won’t be their saving grace because of the significant challenges some of them face at home. Until these are resolved, a country would not benefit fully from a robust Chinese economic recovery.

Emerging markets entered the pandemic in a largely homogenous fashion, but the exit is proving heterogeneous and thus country-specific risks will determine how well their economies do versus the emerging market universe.

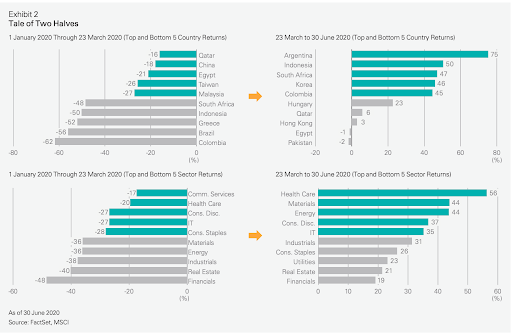

The graph below was produced by Lazard and highlights how quickly financial market conditions can change, with emerging markets experiencing a tale of two halves during the first half of 2020. For instance, South Africa saw equity market returns plummet 48% from the start of 2020 to 23 March 2020, when financial markets reached their nadir after a bear market sell-off. By 30 June 2020, however, South African equities had managed to turn around virtually all those losses, rallying by 47%.

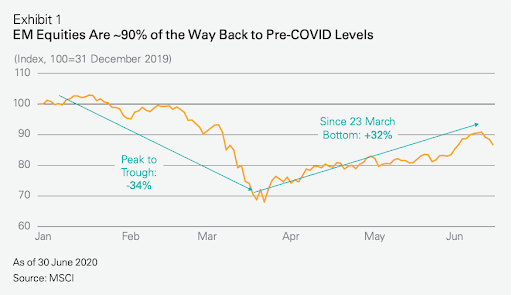

From a broader emerging market equity perspective, the graph below shows that stock markets are almost 90% back to their pre-Covid-19 levels.

Looking forward, Lazard says the fate of emerging markets stocks in the third quarter and beyond will depend on global growth. The asset manager will be watching for four catalysts that could signal a comeback in global growth, namely lower infection rates, stabilising unemployment rates in developed and emerging market countries, improving PMIs and everyday product demand, and, finally, treatment or a vaccine for the virus.

Emerging markets are likely to benefit from the search for yield in a lower for longer interest rate world. The undervaluation of selective equity assets and emerging market currencies, and the elevated global liquidity levels as a result of the trillions of dollars of stimulus packages will also hold emerging-market assets in good stead.

However, investors will need to be selective and invest based on the particular risk/return potential of each country. ING says the heterogeneity of emerging market economic performance means that deviations across regions and countries are likely to be substantial.

How are the different emerging markets stacking up and why?

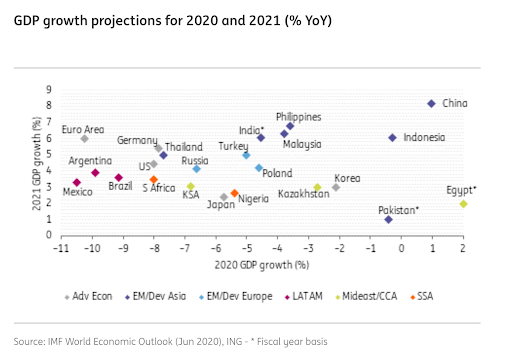

Asia is faring best and facing a more modest contraction, with the IMF World Economic Outlook seeing the region slipping 0.8% in 2020, but then rebounding a healthy 7.4% in 2021. Much of the region’s turnaround would be a result of the 8.2% growth anticipated in China. Li says emerging Asia is well-positioned to withstand a growth shock and its recovery will be based on how well they have handled the outbreak.

Latin America saw the biggest downward revision in growth as a result of the struggles these countries have had in containing the virus. In the IMF figures, points out ING, the region is expected to decline almost 10% in 2020, -4.2 percentage points below the April 2020 forecast, before recovering to 3.7% in 2021. Li says Mexico and Brazil were already trading at higher equity valuations and thus they are likely to pose greater downside risks for investors too.

The outlook for Turkey and Argentina is also gloomy because they pose solvency risks, and Li considers them as outright negatives from an investment vantage point.

In the sub-Saharan Africa region, commodity exporters and South Africa are expected to decline 8% before gaining 3.5% in 2020 – steeper declines than the region as a whole. South Africa’s challenging economic situation is based on the fact that the country hasn’t reached a peak in Covid-19 infections and, instead, is seeing the rate of infections accelerate markedly. But, as President Cyril Ramaphosa pointed out when announcing the rolling back of certain lockdown conditions on 12 July 2020, South Africa does have a far lower death rate of 1.5% versus the 4.4% world average.

The other well-known hurdles to economic growth in South Africa are the fiscal indebtedness, the slow progress made on State-Owned Enterprises (SOEs), which Fitch again highlights in a sub-Saharan Africa Monthly Outlook Presentation, and government and business have yet to reach consensus on how to get going on the huge proposed infrastructure programme.

On the government’s progress in reforming SOEs, Fitch says: “While it is making some progress with South African Airways, efforts by the South African government to reform ailing state-owned enterprises continue to prove challenging.” It points out that heavily indebted Eskom has already indicated it won’t be able to meet its June 2021 deadline to unbundle the energy producer into three entities responsible for generation, transmission and distribution.

With so many challenges to overcome, a vibrant Chinese economy would be welcome. Although it is highly unlikely to be a panacea, at least it could be a rising tide that gets South Africa, and other emerging markets, closer to dry land. DM/BM