It is important, whether you have a low-level living annuity income or you’re very wealthy, that you get advice on offshore investments, says the writer. (Photo: Rawpixel)

It is important, whether you have a low-level living annuity income or you’re very wealthy, that you get advice on offshore investments, says the writer. (Photo: Rawpixel) Wouter Fourie, a top-flight financial planner, recently delivered a presentation on offshore investment at the first Global Matters virtual engagement online conference, sponsored by Momentum Investments. He demonstrated that most people who invested offshore, using their assets in their investment-linked living annuities (living annuities or illas), had made gains – it didn’t matter about Covid-19 or the Jacob Zuma kleptocracy regime.

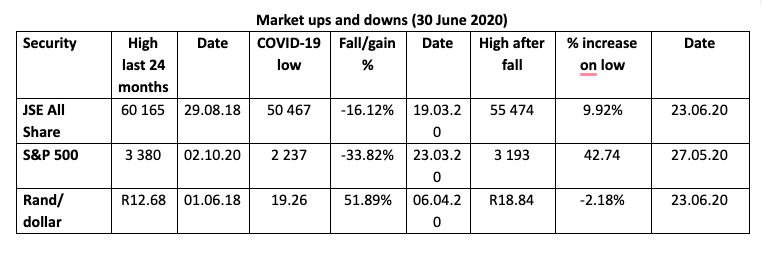

This is what the data now looks like:

In his presentation, Fourie referred to South Africa as the “1% country” – not in a nasty way, but in a realistic way.

His reasons are:

- The gross domestic product of South Africa is about 0.5% of the world GDP,

- The JSE stock exchange accounts for about 1% of global investment opportunities, and

- The rand accounts for less than 1% of world currency markets.

We are actually quite a small economy, only equalling one of the US’s smaller states.

Fourie says if you are going to concentrate on South Africa’s markets, you are going to lose out on investment returns for the following reasons. You will not:

- Participate in global growth, and

- You lose out on the compounding growth on the investments you have not made,

- You will not receive the diversification and the reduction in risk by spreading your risk to more types of industries and services. This means you will not receive the benefits of an income stream that will flow from these sources. This is particularly important for pensioners,

- You will not benefit from receiving guidance from world-class financial investment professionals, or from world-class international financial centres, and

- Finally, you will not have the peace of mind that those who did invest offshore have. The political risks of all our local crises are an add-on benefit.

Fourie says that in investing offshore, you have two main choices, namely:

- Investing through a local or offshore endowment policy, which opens the way to more underlying investments, or

- Through a direct share portfolio or more traditional Financial Sector Conduct Authority (FSCA) category 3 investment, namely a unit trust fund. This is the option used more usually by living annuity pensioners. This avenue is also open to pre-retirement annuity funds, pension funds, provident funds and preservation members. Investment in retirement funds, retirement annuity funds, provident and preservation funds are governed by Regulation 28 of the Pension Funds Act that only allows 30% to be invested offshore. Regulation 28 is a prudential investment regulation that limits how much you may invest in different assets and percentages of underlying assets.

However, living annuities are not affected by Regulation 28. You can take all your money in a living annuity and invest it offshore. This is not being suggested, but it gives you more freedom of movement. Again, how much you invest offshore will be dependent on how wealthy you are and the drawdown rate in your living annuity.

One of the issues with default annuities is that they limit your offshore investments to 30% in line with Regulation28.

Everyone has a choice on what vehicle to use. The main limitation is the extent of your wealth.

Someone who is well off with both a living annuity and other assets can choose both with those less wealthy using local unit trusts or life assurance policies while those who are wealthy choose to use both rand and foreign-denominated vehicles.

For example, they could use a rand-denominated unit trust fund, which invests offshore, for their living annuity, while using their R10-million annual foreign investment allowance to invest directly offshore.

To invest directly offshore does take a lot of money, if it is not to be eaten away by costs.

Fourie says there are a number of steps involved in investing directly offshore from getting a tax clearance, buying foreign exchange, choosing a foreign no-tax, or low-tax investing environment, while also considering your tax situation and estate planning.

Fourie says that people investing:

- In a rand-denominated (South Africa platform) unit trust or life assurance policy need the following: international diversification, reduced emerging market risk, a hedge against any fall in the value of the rand as well as a geographical and political hedge. You invest rands and you get any withdrawals in rands in South Africa.

- In a foreign-denominated (international platform), you use rands to buy a foreign currency. You can withdraw that money anywhere in the world to reinvest or spend where you like. When planning to emigrate, you can use your annual foreign currency allowance to transfer funds without impacting on the allowance for emigration. Fourie, however, warns that you must take care in choosing the offshore jurisdiction through which you choose to invest. You must ensure that it has proper consumer protection policies as well as the international company handling your investment.

Inside a retirement fund either in the build-up, or in an annuity, you will not be taxed. South African residents who invest directly through a rand-based unit trust or life assurance policy or in using the foreign investment allowance, will pay South Africa tax at the applicable rates.

Fourie’s presentation, “Fundamentals of Offshore Investments”, which can be watched here, is worth watching as it goes into all sorts of things from taxation to international financial centres to what happens if you die.

Much of what he deals with will not affect the ordinary living annuitant.

It is important, whether you have a low-level living annuity income or you’re very wealthy, that you get advice on offshore investments. Compare the returns and different options, including whether to invest through a unit trust, or direct shares, or a life assurance policy (endowment), or using a passive investment or active managed investment. DM/BM

Bruce Cameron, the semi-retired founding editor of Personal Finance of Independent Newspapers, over a number of weeks, will look at the state of pensioners of retirement funds, which will highlight research undertaken by Alexander Forbes on retirement income in South Africa. Bruce Cameron is co-author with Wouter Fourie of the best-selling book, The Ultimate Guide to Retirement in South Africa.

Comments

Scroll down to load comments...