Lesson 1 – we are all interconnected

One of the founding principles of Responsible Investing (RI) is the interconnected nature of our social, biophysical and market ecosystems. Importantly RI recognises the impact of unpriced externalities on the safe operation of the market, society and environment. Examples include the social and environmental costs from burning fossil fuels or societal health impacts of high- calorie foods. By considering externalities in its approach, the RI field essentially asks all participants in the investment value chain to consider the wisdom of pursuing short-term returns at the expense of long- term resilience of social and environmental systems.

The COVID-19 crisis has laid bare the very real interconnectivity between our social, environmental and market systems. The lesson here is - don’t neglect interconnectivity and long-term system resilience.

Lesson 2 – shared value

Professors Kramer and Porter of Harvard Business School penned their famous article on shared value in the early 2000s. In it they argued that the best business strategy to adopt in a world with increasing social and environmental pressures was one that generated profits while solving for long-term social and environmental resilience. They proposed a stakeholder inclusive model for capitalism which encourages value to be shared across participating stakeholder groups. In effect, this type of strategy requires company management to carefully consider a broad range of stakeholders and the associated business “impacts”. For some management teams, this is a sharp departure from the age-old adage that the business of business is business.

COVID-19 puts a sharp focus on management approaches to human capital management, corporate culture, and the treatment of customers. Corporate responses around these issues can potentially have lasting impacts for all company stakeholders. For investors that are ESG literate, it’s no news that workforce management, employee satisfaction and corporate culture have a long- term impact on productivity, share price performance and returns. Similarly, that companies’ treatment of customers is an important driver of brand equity and improved customer relationships over time. How management teams respond in this time of crisis will be telling for their long-term profitability. Aside from management practices, the COVID-19 crisis also exposes the underlying business model, specifically what goods and services the company provide. As we are collectively finding out, essential services means something very specific. It redefines what we can and can’t do without, and what we are prepared to pay for. Business models that solve for food security, connectivity, online education, entertainment, sustainable mobility, finance, water, energy, sewage, waste, healthcare, etc have prospects for growth.

Those investment teams with deeply integrated ESG processes will no doubt be attuned to these issues. They will have a view of which business models and management teams are therefore best placed to retain value through the cycle.

COVID-19 has been indiscriminate in whom it infects, and doing so it has become everyone’s problem. Those with the best chance of fighting it are doing so collaboratively across a broad range of stakeholders. The COVID-19 crisis reminds us of the power of working proactively with all stakeholders to achieve shared value outcomes.

Lesson 3 – understanding the science

As a consequence of its focus on ESG issues, the field of Responsible Investing relies on much scientific data to make the business case for sustainability. Most asset managers with a focus of RI will thus have a clear understanding of the science behind climate change and the attendant risks and opportunities. Notwithstanding this, in the current age of populist politics, the role of science has increasingly taken a back seat.

Despite being one of the most scientifically peer-reviewed publications produced by humanity, the Intergovernmental Panel on Climate Change assessment reports failed to inspire political leadership.

Although the COVID-19 crisis is more near term compared to climate change, it is instructive to see how rapidly political leaders, despite their differing views, have fallen in line with prevailing medical and scientific consensus. The lesson of COVID-19 is – don’t forget the science. Importantly, asset managers with these specialist skills will be well placed to look ahead.

As tough as the lessons from the COVID-19 crisis are, we expect that they will strengthen RI as an approach to investments.

ESG is not just a nice-to-have but it is also good to have

Old Mutual Investment Group has long maintained that analysis of ESG issues can, and does, drive long-term investment performance. It not just a nice-to-have, it is a good-to-have. We see sustainability as a macro thematic trend that is fundamentally reshaping the competitive landscape across all sectors. Companies that respond to this trend early enjoy a stronger social licence to operate, lower staff turnover, better resource efficiency, lower cost of capital, better innovation and stronger access to the market.

As a group, we have invested in building out our product offering to capture this theme through

a series of ESG indices. These funds have attracted inflows in a manner that is consistent with the growing global trend. Sustainable investing has grown exponentially in the past five years. For example in the US, the net flows into sustainable funds reached US$20.6 billion in 2019, more than four times the previous annual record that was set in 2018.

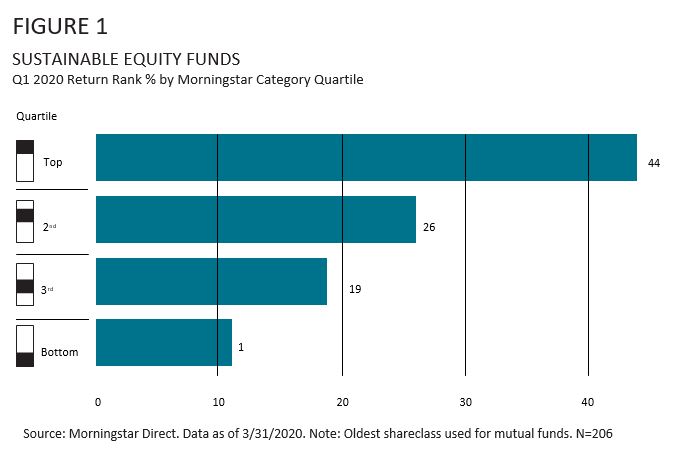

Like all funds, sustainable equity funds suffered large and sudden losses of value in the first quarter of 2020 due to the global coronavirus pandemic. However, Morningstar reports that sustainable investment funds held up better than conventional funds during this period. They report that seven out of 10 sustainable equity funds finished in the top halves of their Morningstar categories, and 24 of 26 environmental, social and governance-tilted index funds outperformed their closest conventional counterparts.

This is also evidenced by the MSCI ESG index tracker funds that Old Mutual offers, which have shown resilient performance over the past quarter. Figure 2 shows the cumulative returns of the MSCI Emerging Market ESG Index to the end of March 2020.

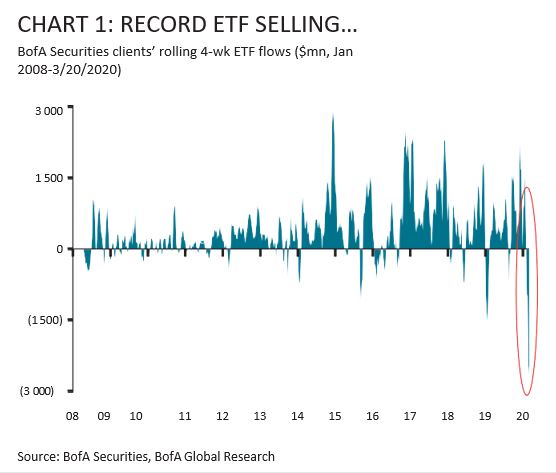

An additional point to consider in the “good to have” bucket is that ESG fund flows remain intact. Research from Band of America Securities indicates that while there has been record ETF selling over the last few weeks (Chart 1), ESG funds have seen inflows for ten straight weeks (Chart 2). Even after the market sell-off, ESG ETF assets under management (AUM) are still up nearly 5% year to date, while S&P 500 ETFs have seen AUM decline by over 30%. In Europe, ESG funds have seen persistent inflows including recent weeks, even amid EU stock outflows.

Perusing green growth

As society seeks to rebuild in a post-COVID-19 world, we expect the idea of green growth to continue to gain traction. The notion of green growth emerged after the last financial crisis and envisages an alternative growth path guided by climate awareness, resource efficiency and social inclusion. At a global level, green growth features in national growth strategies and the EU is putting in place legislation to drive and incentivise these kinds of outcomes. At the local level, work is being undertaken to develop a green economy taxonomy for South Africa as a basis for supporting our growth agenda. As the South African government struggles with an increasing debt burden, we can expect a resurgence of the prescribed assets debate and increasing pressure for all actors in the financial markets to align with green economy outcomes.

Old Mutual Investment Group has specialist green economy investment capabilities, managing some R131 billion of client assets in the green economy. It is important to note that given the structure of the South African economy, accessing green growth assets has required that investors look to unlisted markets via Private Equity and Infrastructure type funds. Accessing these investments has traditionally been the domain of institutional investment funds. Green growth is not only a scientifically bounded economic idea but is also a set of globally consistent consumer preferences, as more and more consumers align with the sustainability agenda. Doing more with less has always been a good idea, as has caring for the environment along with being a good neighbour. As such, we expect demand for “green” assets to grow beyond the institutional market to the retail market as well. Asset managers that have green growth capabilities and assets, will have an advantage over their peers as the world seeks to re-normalise in a post-COVID-19 environment.

What next?

It is not clear what’s next. The COVID-19 pandemic is unprecedented in modern times. There is much we don’t know about how this will play out. However, what we do know is that the world will be much changed. Our sense of interconnectivity will be enhanced, we’ll have learnt that it’s not just returns that matter, and that businesses that focused on long-term outcomes will be remembered. Sustainable investing is about delivering competitive financial returns by leveraging ESG insights. It is also about shifting the global economy to a path that is low carbon, resource-efficient and socially inclusive. Now, in the midst of this crisis, is the perfect moment for all actors in the financial services sector, whether they be advisers, consultants, asset owners or asset managers, to realign their understanding of RI and ESG issues. It is critical that decision-makers should be clear on how ESG issues affect long-term risk and returns, and additionally how the growing trend towards sustainable investing impacts the ability to attract and retain client capital. DM/BM