For South Africa, in particular, recent market movements have strongly suggested that the bad news has been priced into bond market valuations and the currency. (Photo: Adobestock)

For South Africa, in particular, recent market movements have strongly suggested that the bad news has been priced into bond market valuations and the currency. (Photo: Adobestock) Hard-hit emerging market currencies appear to have hit a plateau over the past week. The SA rand is almost 3% firmer to R18.3 to the dollar since the beginning of May after depreciating nearly 10% from R19.08 after risk-off sentiment took hold in the last week of April.

The recent recovery hadn’t won back the significant ground lost against the dollar this year though, with the domestic currency some 31% weaker than it was at the start of the year when it traded at about R14 to the greenback.

The rand’s recent strengthening is mirrored by other emerging market currencies, which have benefited from the significant stimulus packages put in place in home countries and elsewhere globally. As a result, investors are continuing to look through the appalling economic data to an anticipated recovery in economies on the other side, whenever that may be.

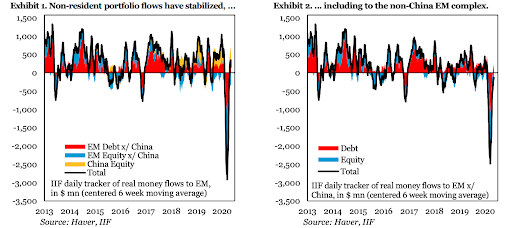

Latest Institute of International Finance (IIF) research shows that there’s been a fundamental change in investor flows into emerging markets after the unparalleled “sudden stop” in March and record outflows during March. The organisation comments: “The March ‘sudden stop’ is now in the rearview mirror, and EM is stabilising.”

In addition to the stabilisation in exchange rates, IIF points out that net issuance of bonds abroad is at record strength and, even more importantly, its high-frequency indication of non-resident flows has shifted in a positive direction.

It sees the “violence” of the selloff in March as having a silver lining. “At the time, we called outflows a ‘five-sigma’ event, meaning that the scale of outflows lies far beyond any historical analogue, representing a statistical outlier. That now means that a lot of negativity, perhaps too much, may be priced and means that the hurdle for further weakness is high.”

For South Africa, in particular, recent market movements have strongly suggested that the bad news has been priced into bond market valuations and the currency. Government benchmark bond yields still offer attractive real yields compared with the major developed markets and many other emerging markets. This yield premium could hold our domestic financial market in good stead, barring a significant deterioration in global risk appetite or South African specific economic and health dynamics.

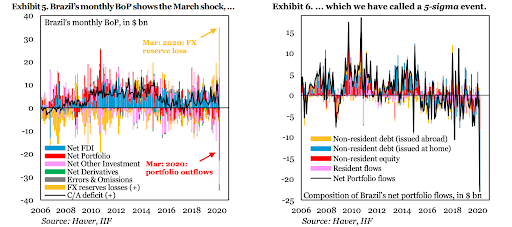

It’s also notable that the South African rand and Brazilian real have traded places in the past month. For most of the year, and during the financial crisis, the rand was sold off more sharply than the real. However, since late April, the real has depreciated by 1.4% versus the rand’s almost 10% appreciation. Year to date, the Brazilian real is 42.4% weaker compared with the rand’s 30.1% slide.

In the IIF’s graph below, the extent of Brazil’s “five-sigma” event is highlighted.

The welcome reprieve that has followed for emerging markets, including Brazil, since then may prove short-lived if two significant ticket risk events materialise. These risks are the possibility of countries experiencing a second wave of coronavirus infections and a resumption of the US-China trade war.

Since the start of March, countries have been emerging from lockdown to varying degrees. In the US, more and more states are normalising. US President Donald Trump is insistent the world’s largest economy needs to be fully opened up as soon as possible even if there is a risk that the rate of infections, which are still a concern in some states, continue rising. Even more worrying is that director of the United States National Economic Council, Larry Kudlow, has gone on record saying that the economy will remain open even if there is a second round of infections. Last week, South Korea and China highlighted the risks of a second wave returning, with both countries having to contain a pick-up in infections notwithstanding strict and comprehensive measures to contain the spread of the virus.

The other risk that looms over emerging markets is the prospect of a resumption of the US-China trade war. Trump has been ramping up his criticism of China. He is investigating whether China misled the world about the extent of the risk and the origin of the virus.

The competition between the two nations is unlikely to ease up as China emerges from its economic slump. Last week China published export data that was better than expected, with exports rising 3.5% year-on-year in April versus the -13.7% consensus. The surprise uptick in exports was in stark contrast with the US’s spectacularly bad jobless data. Last week the full impact of the coronavirus on the US jobs market was captured in the 20.5 million job losses in April – a decline not seen since the Great Depression.

The divergent economic fortunes of the US and China are not going to sit well with Trump as he tries to secure his chances of re-election in November by showcasing his ability to get the US economy back on track as soon as possible.

Against this backdrop, emerging market currencies are likely to experience volatile market conditions as they are subject to escalation and de-escalation in the economic conflict between the US and China. However, as the IIF points out, at least the sharp depreciation in emerging market currencies this year has built-in some cushion in the event of a renewed selloff. Thus there is a chance we may not experience declines quite as severe as those experienced in the 2008 financial crisis and as steep as the selloff in the first few months of this year. BM