(Photo: Flickr / Marco Verch)

(Photo: Flickr / Marco Verch) If you have sufficient capital on which to retire, you can use almost any retirement annuity on offer and preferably a combination of a living annuity and a guaranteed annuity.

But, even if you retire with sufficient capital, and then make mistakes in investing your retirement capital, you are likely to become unstuck.

The one thing all retirees and soon-to-be retired people need to know is how to manage their investments to ensure it provides a sustainable income, given these repeated shocks. These shocks are likely to get worse and, in particular, need to be taken into account by people who are in the disinvestment stage of their lives.

I am going to deal with the main selling points of living annuities made by product providers and what you must take into account.

Right now, 90% of pensioners, by amount, buy living annuities, investing R585-billion in 2018, with all their risks, as opposed to traditional annuities, where you carry little risk.

Living annuities come with a lot of complex risks, which most people do not understand or are able to manage.

Research by Alexander Forbes shows that many retirees with living annuities were already in serious trouble, even before the Covid-19 pandemic, the downgrading of South Africa’s debt and the market crash.

Last year, at the Actuarial Society of South Africa’s annual conference, Warren Matthysen, principle consultant at Alexander Forbes Investments, asked why so much money was allocated to living annuities as they are seldom optimal if they are intended to provide maximum income in retirement.

He questioned if people never really understand what they are buying, and if they understand the charges and opportunity costs associated with living annuities.

Matthysen told the conference that living annuities have two-component benefits, one being the income and the other, the death benefit.

“But we can’t place a value on these benefits as no one really knows what they will be,” he said.

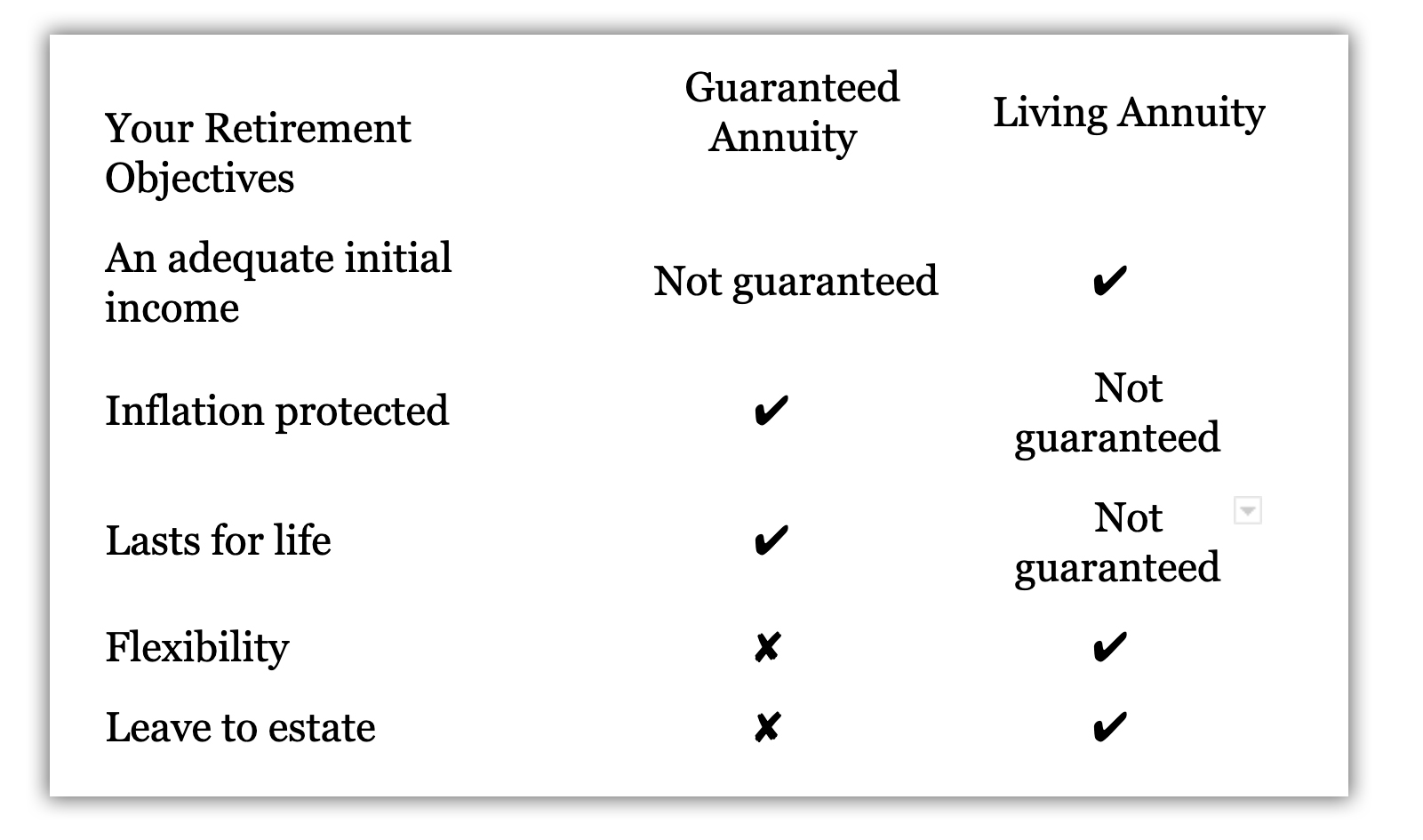

The best way to look at the pros and cons of living annuities is to use the product providers simplistic diagram used to promote them.

Here is the diagram:

I will deal with an adequate initial income and inflation this week and the other three next week.

An adequate initial income

The diagram shows that an adequate “initial” income is less certain if you used a guaranteed annuity (pension) provided by a life assurance company, where your pension is guaranteed for life.

But the product providers claim that the “initial” pension provided by a living annuity is likely to be spot on.

But “initial” is the key word. My quotes.

If you give me R5-million, I can guarantee you the “initial” income for the first 12 months, simply by dividing the amount by 12, after deducting all the fees and costs.

The question should not be: “initial” payment of an income. The questions that need to be asked are: What will your income be in 10, or 20-years time; and what happens if you live to be 100?

Matthysen’s argument stands up here, namely whether your pension will last, at the required level with inflation increases to sustain your income needs, until you die.

It is the long-term effects that need to be dealt with and this will be determined by the following number of unknown factors.

The only answer is to provide assumptions, looking at both the worst case and the best-case outcomes. But, be warned, the assumptions may change depending on the state of investment markets at and while you are retired, and your drawdowns.

John Anderson, the actuary leading the Alexander Forbes research, says if you start at age 65 to withdraw your pension income from a living annuity, with a rand amount linked to an initial 6% drawdown, by the time you are between 74 and 77 years old, you will reach the “point of ruin”, when you reach the maximum drawdown of 17.5% and then start drawing down less every year. This also depends on your investment strategy and its ability to generate inflation-related returns after costs.

With a 7.5% drawdown at age 65, which is the average drawdown of its pensioners provided by Alexander Forbes research, you reach the point of ruin between the age of 71 and 73 years. The higher your drawdown, the sooner you will reach the point of ruin.

Inflation protected

Here the argument that living annuity product providers use is more honest. If you want long-term inflation protection, the only way to get it is by buying a traditional guaranteed annuity issued by a life assurance office. However, with a guaranteed annuity, you need to buy one that is linked to inflation.

Generally, if inflation goes up at a faster rate or even at the same rate as your investment returns before costs, you will be forced to reduce your standard of living. (Remember that the inflation rate is an average. Your personal inflation rate could be higher or lower.)

If you buy a guaranteed “level” annuity, where the same amount is paid out every year of your retirement, you will lose your rand buying power very quickly. Members of the Transnet Second Defined Pension Fund found this out when they were limited to a 2% a year increase, and how, within a few years, they could no longer afford to meet their basic financial requirements.

So, the annuity must be linked to inflation, which will mean a lower initial pension, but one that will grow with inflation.

Inflation is a major concern for people with living annuities. The main reasons are that underlying capital values go up and down, which will determine the amount of your drawdown in rand terms, particularly when there are uncertain investment returns.

If there is a long period of investment markets falling, as they probably are now, you will be drawing a lot more income from your already depressed capital. A rough rule of thumb is for every year investment markets remain down, it will take you two years to recover.

A reminder that cannot be repeated too often: If you have not saved enough for retirement, you are not likely to suddenly create more after retirement from your investments. You may have to continue working, or relying on friends and family, or the State Old Age Pension.

Next week I will deal with: Lasts for Life, Flexibility and Leave to an Estate. BM

Bruce Cameron, the semi-retired founding editor of Personal Finance of Independent Newspapers, over a number of weeks, will look at the state of pensioners of retirement funds, which will cover research undertaken by Alexander Forbes on retirement income in South Africa. Bruce Cameron is co-author of the best-selling book, The Ultimate Guide to Retirement in South Africa.