(Photo: Pxhere)

(Photo: Pxhere) An unscheduled repo rate cut by another 100 basis points to 4.25% recently in response to the devastating impacts of the coronavirus has dropped the prime lending rate to 7.75%. It’s good news for the economy and many of the people in it, but less so for savings invested in the money market.

Nicholas Riemer, investment education head at FNB Wealth and Investments, says the cut will result in less interest earned on current money market accounts and new fixed-interest instruments will also be offered at lower interest returns.

“This is typical with any variable interest rate-linked instrument,” he says. For those customers with existing fixed-interest investments, however, it is business as usual, as returns on these instruments are locked in.

Preference shareholders will also take a beating, as dividends are often linked to the prime interest rate. The value of preference shares usually also declines in the event of a rate cut.

Although property shares usually increase in value on the back of an interest rate cut, the rental relief and refusals on the back of the national lockdown and economic slowdown do not bode well for money tied up in these investments.

“The cut in the rate should, however, see a reduction in interest expense and as a result improve the rental yields,” says Riemer.

“Higher rental yields result in larger profits made by those companies and thus we can expect to see an increase in property stocks.

“Furthermore, property stocks are valued by discounting future expected distributions to the present by using a ‘risk-free rate’ – usually the 10-year government bond yield. As bond yields decline, the value of these companies increases.”

Generally, the value of other equity also increases when interest rates decline, as underlying companies benefit from lower interest rates on debt and cash flows being discounted using a lower bond yield.

However, the market mayhem witnessed over the last month or so has made the asset class less desirable for existing investors.

The real benefactors of the monetary policy committee’s back-to-back decisions are bond yields, which are expected to decline. This is when bond returns become more attractive relative to cash and some equity instruments, especially for individual investors.

The government recently increased the fixed-coupon rates by 3.5% on retail savings bonds to very attractive levels.

These look extremely attractive and if used correctly, can add a lot of value to your financial plan, says independent financial wellness coach Kenny Meiring.

“The key word here is ‘plan’,” he adds.

“No investment should be done in isolation – it needs to form part of a broader financial plan.

“What you need to keep in mind though is the risk that you could lose out on gains elsewhere if your capital is only locked into a five-year bond, for example. The JSE All-Share Index is sitting at levels last seen in 2012 and there are some bargain buys about.”

Rupert Smith, founder of Summa Financial Services, agrees. He says that while 5.5% guaranteed may look attractive, the reality is that there are tax implications, depending on your circumstances, which may reduce the effective return by up to 45%, and, inflation, especially medical, will erode the purchasing power of both income and capital invested.

“Bearing in mind life expectancy is far greater than it’s ever been, anyone approaching retirement, about to retire or in retirement should have a realistic framework based on their means and their needs,” he says.

“The plan should have a growth and income aspect to it. SA retail bonds may have a place in your financial plan but should by no stretch of the imagination be the only component of your plan.”

That being said, wealth manager Desmond Benecke at Brenthurst Wealth Management says the yields available on government retail bonds compared to market money options are phenomenal at present, especially over the longer term, equating to inflation plus 6%.

Income can be drawn on a half-year or annual basis, and for pensioners over the age of 60 monthly withdrawals are allowed.

He does warn that the inflation-linked bond option also offered by the government is probably not a good investment call currently. Returns are linked to inflation forecasts of 3%, 3.5% and 3.75% over two, three and five years respectively, due to benign economic demand.

The fixed-rate option, however, is a good way to go, he adds, especially in the current diverged interest rate scenario between money and capital markets, and because the government is presently paying a premium to attract investment.

Benecke says it is a good call for investors with lower risk appetite and who don’t appreciate the volatility of current markets. The interest payments on retail government bonds are guaranteed by the state.

Beneke adds that it is an ideal vehicle for individuals saving towards a specific investment goal like a child’s education or for a deposit on purchasing a property. The minimum investment is only R1,000, which makes it accessible to the mass market, and one can invest in multiple types of bonds and various intervals.

“The beauty of the product,” he says, “is that there are no fees, costs or commissions involved, and is easy to access online or even to buy at the local post office.

“It is very simple, transparent and capital maturity is certain. There are no worries in the market performance or capital costs involved.”

If it is a question about liquidity, capital can be withdrawn after 12 months at a small penalty.

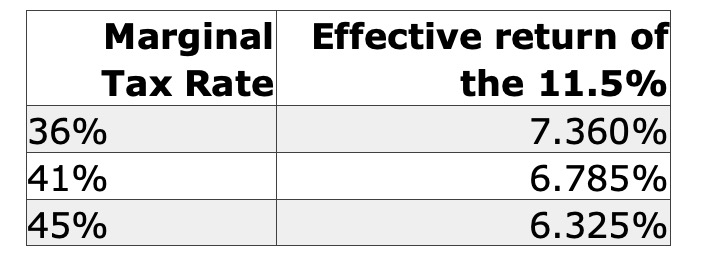

The only caveat, he says, is that returns are pre-taxed, which means interest payments are taxable at individual marginal tax rates after annual tax concessions have been deducted.

The first R23,800 of interest is tax-free if you’re under 65. This increases to R34,500 if you’re over 65.

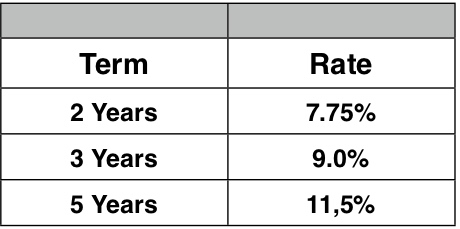

Meiring says if you invest for five years, you will get 11.5% a year in interest. This full amount will be tax-free if you invest less than R206,957 if you’re under 65 and R300,000 if you are over 65.

Above these amounts, you will be taxed at your marginal rate. When you apply your marginal rate to 11.5%, the effective return reduces to:

“These are still decent risk-free returns but no longer have the wow-factor that we initially had before we took tax into account,” Meiring adds.

Below the tax thresholds, if you need an income or want to have money in the bond market for portfolio diversification, the retail savings bonds have a lot of merit up to a point, Meiring says.

“I would certainly consider including these in my clients’ investment plans,” he adds. “However, I will also advise solutions for people under the age of 65 in tax-free accounts and retirement annuities.”

Meiring says the most tax-efficient investment combinations would be to:

- Invest R206,957 in a retail savings bond;

- Invest R36,000 a year in a tax-free savings account; and

- Invest 27.5% of their income into a retirement savings vehicle.

“After this, a financial planner should advise what the most appropriate investment combination for an individual needs should be,” Meiring concludes. BM