Wanderers stadium, drive through Covid 19 testing site in Johannesburg, South Africa. (Photo: Gallo Images/ER Lombard)

Wanderers stadium, drive through Covid 19 testing site in Johannesburg, South Africa. (Photo: Gallo Images/ER Lombard) As the economic costs of the coronavirus mount up, world leaders are facing the ultimate Hobson’s choice: to put the economy first or to continue taking the drastic, and economically devastating, measures to manage the spread of the virus.

Economic growth forecasts are showing just how sharp the fall could be for developed world economies like the US and Europe. Major international banks, including Goldman Sachs, JP Morgan and Morgan Stanley, are predicting that US growth in the second quarter could tank by anything from 24% to 40% in the second quarter of the year. Federal Reserve Bank of St. Louis President James Bullard sees US growth coming off as much 50% and unemployment increased to 30%.

In the face of these dire economic outlooks, some leaders, including US President Donald Trump and Brazilian President Jair Bolsonara are putting their emphasis on their economies, understating the severity of the pandemic and, in Trump’s case, insisting that the cure shouldn’t be greater than the disease.

There is a method in their madness. Trump faces re-election later this year, if coronavirus circumstances allow for it, and needs a healthy economy to help his chances of serving another term. Bonsonara was elected on the promise of reviving a moribund Brazilian economy. Taking the tough measures to curb the spread of the virus will put paid to any chance of economic revival there.

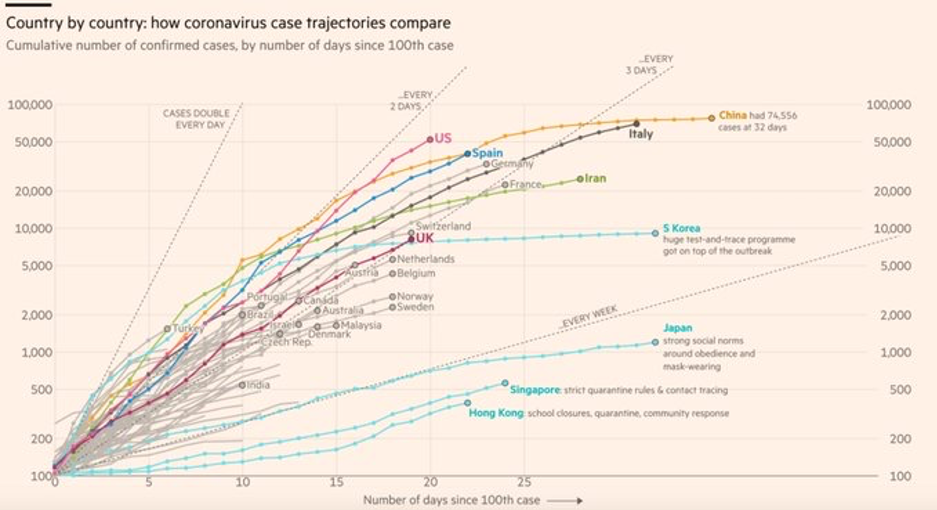

After saying he would relax the social distancing measures by Easter, this week Trump softened his stance somewhat as the US coronavirus count shot up to more than 135 000, with almost 2 500 deaths. The exponential curve illustrating how many cases have been identified in the US has now overtaken all other countries, as shown in the Bloomberg graph below.

Meanwhile, Bolsonara continues to defy prevailing medical advice and is televised deliberately shaking as many hands as possible in his crowds of supporters even as the coronavirus count in the country passes 4 000. “The stumbling response from President Bolsonaro could deepen and prolong the economic damage,” says William Jackson, Capital Economics’ Chief Emerging Markets Economist. In all, Capital Economics estimates that aggregate emerging market GDP will fall by about 1.5% this year, “the worst outturn – and first contraction – since reliable records began in 1951.”

The most visually compelling evidence of how important it is to take social distancing seriously to the point of imposing lockdowns is highlighted in the above graph, where both China and South Korea show a convincing flattening in their curves, while other Asian economies have experienced a far slower and flatter rise than other Western economies over the 44 days since reporting their first 100 cases.

China is coming out of the other end after putting the health of its citizens first. The impact on its economy has been significant and the pain is not likely to end soon. It now has to face a world economy that has virtually come to a standstill and cannot provide the economic momentum it needs to get back on its feet. However, given China’s history of being able to respond quickly to challenges, it wouldn’t be surprising to see the world’s second-largest economy becoming the world’s source for coronavirus protective gear and medical equipment, while also focusing inwards on building up the proportion of the economic activity that stems from an eventually thriving local consumer base.

South Africa is following as closely as is possible in China’s footsteps in its approach to fighting the spread of the virus after going into complete lockdown last week in a matter of weeks after the first coronavirus coming to light in early March. It is a decision that will likely bring the already hard-hit economy to its knees but the alternative would have cost the country a lot more in the loss of human lives if the virus spreads widely in informal settlements.

Where countries have been on the same page in recent weeks is the decision to use all the fiscal and monetary policy firepower they have at the crisis. The US signed off its $2.1 trillion fiscal package, amounting to 10% of GDP, and other packages have come in at between 4% and 5% of GDP.

But will it be enough? Ethiopian Prime Minister Abiy Ahmed, in an opinion column in the Financial Times last week, titled “If Covid-19 is not beaten in Africa it will return to haunt us all”, doesn’t believe it is going to be enough because African countries are not in a position to adopt “similarly meaningful interventions”.

He defines the current approach as uncoordinated, myopic, unsustainable and potentially counter-productive and warns: “A virus that ignores borders cannot be tackled successfully like this.”

Ahmed calls on the G20 must launch a global fund to prevent the collapse of health systems in Africa, he says, and a facility needs to be created to provide budgetary support to African countries.

His views highlight that the policy choices that countries are currently making may well help their economy but will not feed into a healthy global economy in the end.

Sub-Saharan Africa stands to be particularly hard hit. The IMF last week voiced its concerns about the economic impact of the virus on sub-Saharan Africa, writing in a blog: “Across the region, growth will be hit hard. Precisely how hard is still difficult to say. But it is clear that our growth forecast in April’s regional outlook will be significantly lower.”

South Africa is already confronting the harsh economic realities of a sovereign rating downgrade, liquidity pressures and an already weak economy stopping in its tracks. The IMF points out that there have been net capital outflows from the bond and equity markets of more than R100bn ($6.2 billion), the equivalent of 2% of GDP in the past month; the sovereign dollar credit spread has more than doubled to 401 basis points and the rand has weakened by just short of 20% to the dollar.

Giving the government credit, it has acted swiftly and decisively, both in addressing the coronavirus and trying to alleviate a dire economic situation. Last week Finance Minister Tito Mboweni announced an ambitious fiscal package that, while absolutely necessary, was one that the government can ill afford right now. So it is no surprise that he has since acknowledged that South Africa may need to approach the World Bank or IMF for funds to keep the health system on its feet.

Positive news that Ramaphosa has also given the go-ahead for structural reforms long in waiting may have seemed out of place at a time when all resources are focused on the more immediate battles that need to be won.

But it did signal that there could be some light at the end of the tunnel, with the virus providing the opportunity for the government to press reset on the economy and begin building a better functioning state sector with a pared-down, more productive state-owned enterprise labour force and enabling the private sector to move onto a more flexible labour market footing.