Logos sit illuminated on the HSBC Holdings Plc headquarter skyscraper offices in the Canary Wharf business, financial and shopping district in London, U.K., on Tuesday, May 2, 2017. HSBC has appeased investors with $3.5 billion of share buybacks, but after five years of declining revenue analysts are looking for evidence the bank is stabilizing its top line when it reports earnings Thursday. Photographer: Luke MacGregor/Bloomberg

Logos sit illuminated on the HSBC Holdings Plc headquarter skyscraper offices in the Canary Wharf business, financial and shopping district in London, U.K., on Tuesday, May 2, 2017. HSBC has appeased investors with $3.5 billion of share buybacks, but after five years of declining revenue analysts are looking for evidence the bank is stabilizing its top line when it reports earnings Thursday. Photographer: Luke MacGregor/Bloomberg The Europeans aren’t alone. Morgan Stanley Chief Executive Officer James Gorman also told employees on Thursday that the U.S. bank won’t cut its workforce at all this year.

Read more: Morgan Stanley CEO Assures Staff ‘Jobs Are Secure’ in 2020

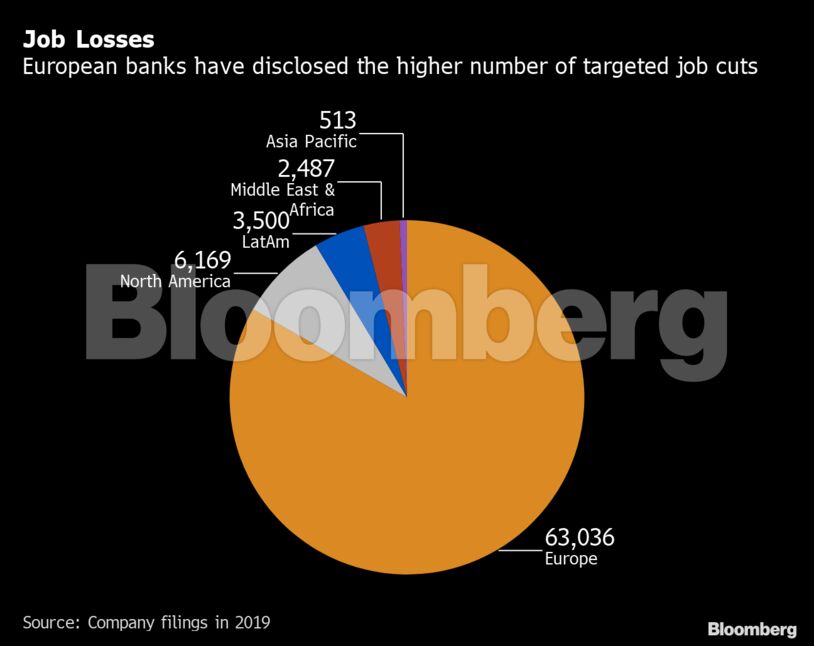

The need for steep cuts at European banks is more acute, where such measures are a major plank in their plans to restore lackluster profitability or bolster shareholder payouts. At the same time, they’re now set to receive unprecedented help from governments and regulators, making it more politically sensitive to put people out of work.

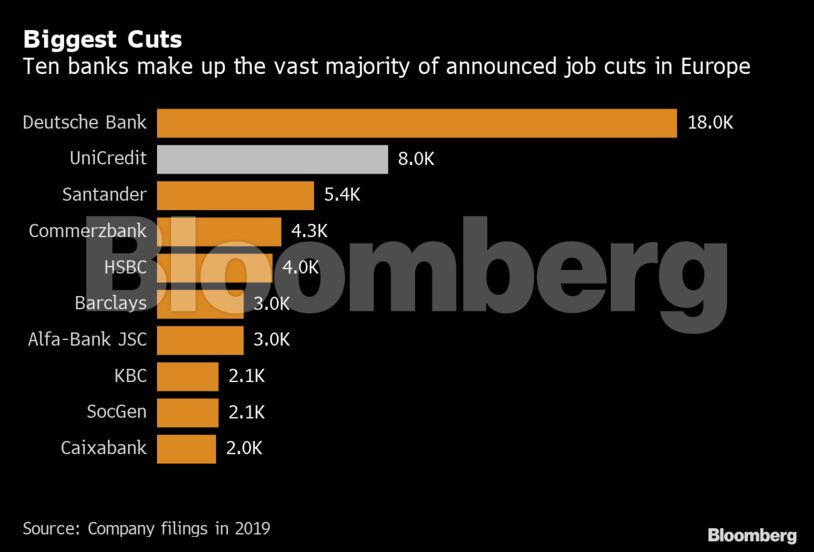

Still, the change of heart isn’t universal. UniCredit SpA is in active talks with worker representatives over its plan to cut 6,000 jobs in Italy and a deal may be in place next month, a union official said. The bank has said most reductions will come through attrition and early retirements.

Royal Bank of Scotland Group Plc Chief Executive Officer Alison Rose is sticking to her plans to slash the bank’s markets business, people with knowledge of the matter said. In February, the state-controlled lender said it will restructure NatWest Markets, without specifying how many jobs will go. The unit accounts for 4,500 of the group’s 65,400 staff, according to 2018 filings.

“Because of the extraordinary impact of the Covid-19 pandemic, we have decided to pause, for the time being, the vast majority of redundancies associated with this program where notices have not already been issued,” HSBC Chief Executive Officer Noel Quinn told staff in a memo on Thursday.

Banks are seeking to show that -- contrary to the last financial crisis more than a decade ago -- they are now in a position to help countries deal with the unprecedented impact of the virus and its economic impact through ensuring that credit keeps flowing. They are also receiving government aid on loan guarantees and waivers to tap into their capital buffers to help them weather the crisis.

“At this uncertain time, we have made the decision to stop the structural changes that were due to take place for some of our teams,” a Lloyds spokesperson said by email. “Our focus is on supporting our customers and colleagues during this unprecedented time.”

Deutsche Bank said Thursday it’s deciding whether it can join a government program that draws on taxpayers’ money to allow companies to put staff on shorter hours while maintaining most of their pay. For Germany’s biggest lender, the job cuts are central to a massive restructuring that means getting out of several businesses entirely.

The challenge of negotiating with labor unions -- an essential step in most German headcount reduction programs -- while most people are working from home could pose an operational challenge to the bank’s plans, Commerzbank Chief Financial Officer Bettina Orlopp indicated on a conference last week.

“Ms. Orlopp has indicated that job cuts may happen more slowly in the current circumstances,” Stefan Wittmann, a union representative serving on Commerzbank’s supervisory board, said by email. “In our view, that would be the right thing to do.”

The delayed job cuts put at risk the restructuring efforts under way at many banks at a time when stress in the financial system is rising. Moody’s on Thursday downgraded the credit outlook for large swathes of Europe’s banking industry as it predicted rising loan-loss provisions coupled with a strong decline in revenue that will further erode the sector’s profitability.

“I don’t think it’s in this kind of situation that we’re going to announce restructuring measures,” Societe General CEO Frederic Oudea said at a conference last week. “There is a question of decency.”